You're thinking about leaving your job; but you're wondering: When is the best time to leave for financial reasons?

Timing matters. Leaving a week before a big bonus hits or right before your equity vests could cost you tens of thousands of dollars. But staying too long in the wrong job can cost you even more in lost opportunities and career growth.

Let's break down how to time your departure strategically, so you're not leaving money on the table.

What to Consider Before You Leave

Before you set a departure date, understand what you're walking away from:

- Unvested equity (RSUs, stock options)

- Bonuses or commissions

- 401(k) vesting schedules

- PTO payouts

- Health insurance coverage

- Timing of raises or promotions

Let's dig into each one.

1. Equity Vesting: Don't Walk Away from Money

If your company offers RSUs (Restricted Stock Units) or stock options, check your vesting schedule.

How vesting works:

Most companies vest equity over 3-4 years, often with a "cliff":

- 1-year cliff: No vesting until you hit 12 months, then 25% vests

- Monthly or quarterly vesting after that

Example:

You have $100,000 in RSUs vesting over 4 years.

- Year 1: $25,000 vests

- Years 2-4: $6,250 vests every quarter

If you leave one month before a vest date, you forfeit that $6,250.

What to do:

- Check your vesting schedule

- If you're close to a vest date (within 1-3 months), consider waiting

- If you're years away from your next vest, the opportunity cost of staying might outweigh the unvested equity

Exception: If your mental health is suffering or you have a time-sensitive opportunity, don't sacrifice your well-being for money.

2. Bonuses: Timing Is Everything

Many companies pay annual bonuses in Q1 (January-March) for the prior year's performance.

The trap:

You worked all year for a bonus, but if you leave in December, you might forfeit it.

What to do:

- Confirm your bonus payout date

- Understand your company's policy (do you need to be employed on the payout date?)

- If your bonus is $10,000-20,000+, waiting a few weeks might be worth it

Example:

Your bonus pays out February 15. You're ready to leave in January. Waiting 6 weeks nets you $15,000. That's worth the wait.

But consider:

- Is your new job offer time-sensitive?

- Can you negotiate a signing bonus with your new employer to offset the loss?

3. 401(k) Vesting: Know Your Schedule

Some employers match 401(k) contributions, but those matches may vest over time (typically 2-6 years).

Vesting schedules:

- Immediate vesting: You own the match right away (best case)

- Cliff vesting: 0% vested until you hit a certain number of years, then 100% vests

- Graded vesting: You vest a percentage each year (e.g., 20% per year over 5 years)

Example:

Your employer matches $5,000/year with a 3-year cliff. If you leave after 2 years and 11 months, you forfeit $15,000 in matches.

What to do:

- Check your 401(k) vesting schedule (it's in your plan documents)

- If you're close to full vesting, consider waiting

- If you're early in the schedule, the opportunity cost of staying might be too high

4. PTO Payouts: Use It or Lose It?

Some companies pay out unused PTO when you leave. Others don't.

What to do:

- Check your company's PTO policy

- If they don't pay out, use your PTO before leaving (take a vacation, plan your transition)

- If they do pay out, understand the tax implications (PTO payouts are taxed as ordinary income)

Example:

You have 3 weeks (15 days) of unused PTO. If your daily rate is $400, that's $6,000. Make sure you're not forfeiting it.

5. Health Insurance: Don't Let Coverage Lapse

Leaving your job means losing employer-sponsored health insurance.

What to do:

- Understand when your coverage ends (often the last day of the month you leave)

- Have a plan for new coverage:

- Don't go uninsured; one medical emergency can destroy your finances

6. Raises and Promotions: Don't Leave Too Soon

If you're up for a raise or promotion, the timing matters.

Example:

You're expecting a $10,000 raise in your annual review (happening in 6 weeks). If you leave before the review, you lose the raise and your new job's offer is based on your current (lower) salary.

What to do:

- If a raise/promotion is imminent, wait

- Use the higher salary as leverage when negotiating your new offer

But consider:

- How certain is the raise?

- Is it worth delaying your departure?

When to Leave Despite Financial Considerations

Sometimes, the best financial decision is to leave immediately, even if you're forfeiting money.

Leave now if:

- Your mental/physical health is suffering: No amount of money is worth burnout, anxiety, or depression.

- You have a time-sensitive opportunity: If your new job won't wait, don't risk losing it.

- Your current job is toxic or unstable: If layoffs are coming or the environment is unbearable, get out.

- The opportunity cost of staying is too high: If staying means missing out on massive career growth, leave.

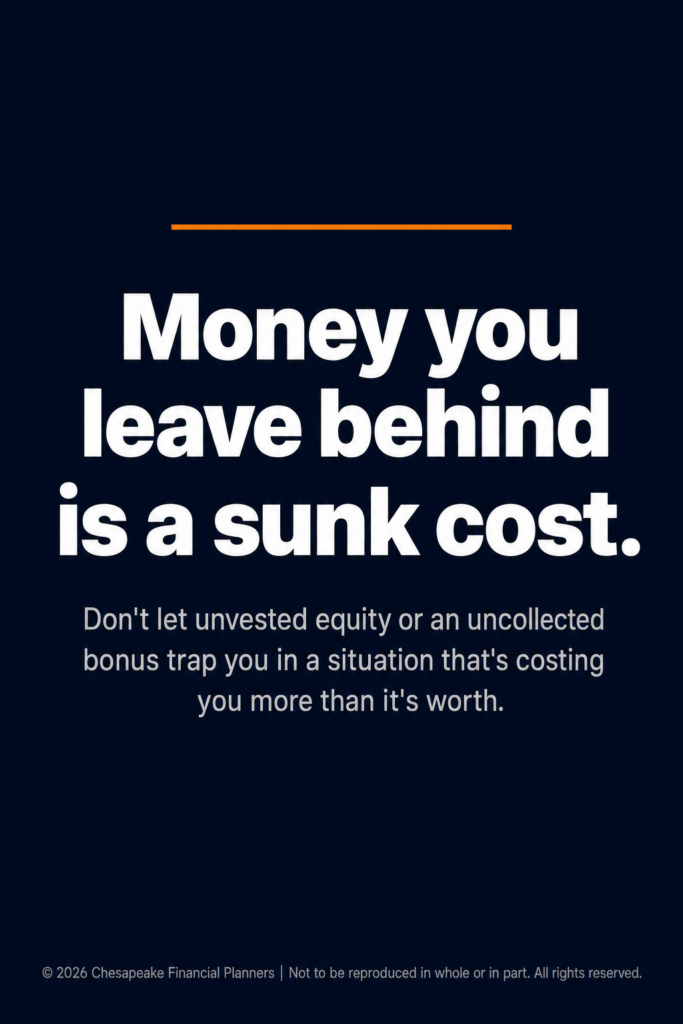

Money you leave behind is a sunk cost. Don't let it trap you in a bad situation.

How to Negotiate Your Departure Timing

Sometimes, you can have your cake and eat it too.

Option 1: Negotiate a later start date with your new employer

"I'm excited to join, but I have equity vesting on [date]. Could we push my start date to [date]?"

Most employers accommodate reasonable requests.

Option 2: Negotiate a signing bonus to offset what you're forfeiting

"I'm walking away from $X in unvested equity and a bonus. Can we discuss a signing bonus to help offset that loss?"

Many employers are willing to do this, especially for strong candidates.

Option 3: Work part-time or consult during the transition

Some companies allow you to stay on part-time or as a contractor to bridge the gap until equity vests or bonuses pay out.

The Financially Optimal Timing

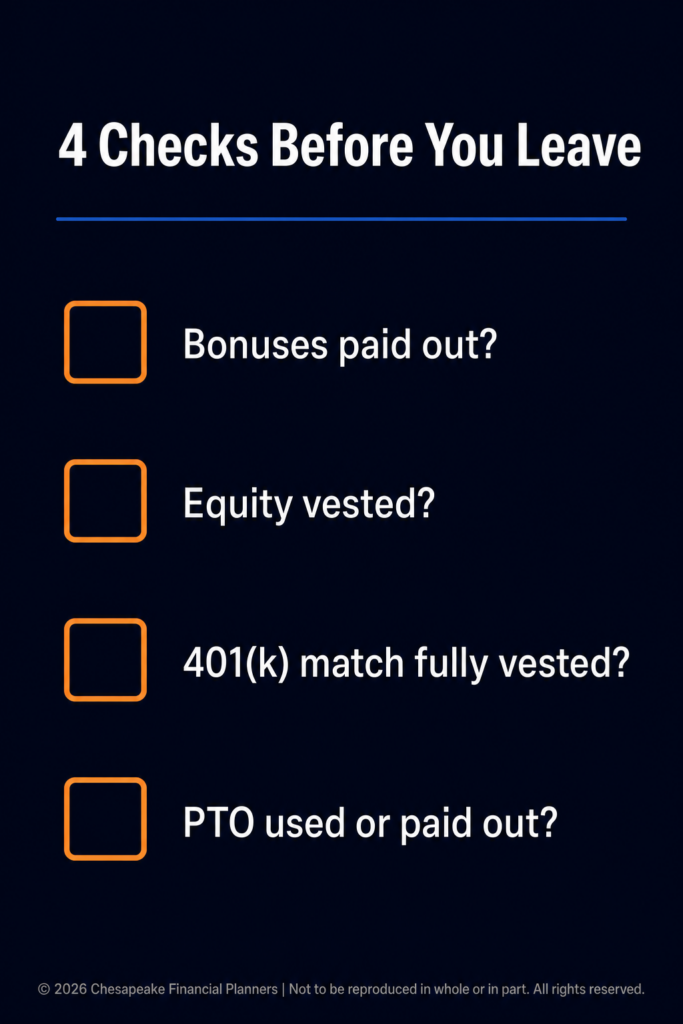

Here's the ideal scenario:

Step 1: Wait until after major payouts

- Bonuses paid out?

- Equity vested?

- 401(k) match fully vested?

- PTO used or paid out?

Step 2: Leave at the end of a month

This ensures health insurance coverage through the full month.

Step 3: Start your new job at the beginning of a month

This minimizes gaps in health insurance and income.

Step 4: Time it around slow periods

Leaving during a slow period (post-project, end of quarter) can make transitions smoother.

Real-Life Example

Scenario:

You're considering leaving your job. Here's what's on the table:

- $20,000 in RSUs vesting in 6 weeks

- $15,000 annual bonus paying out in 8 weeks

- 401(k) match fully vested

- 2 weeks unused PTO (worth $4,000)

- Health insurance through the end of the month

Best move:

Wait 8 weeks. Collect the RSUs ($20K) and bonus ($15K). Use your 2 weeks PTO during your notice period. Leave at the end of the month.

Total saved by waiting: $39,000

If you can't wait 8 weeks:

Negotiate a $35,000 signing bonus with your new employer to offset the loss.

When the Math Doesn't Work

Sometimes, staying isn't worth it, even for big money.

Example:

You have $50,000 in equity vesting in 18 months. Your current job is toxic, your career is stagnating, and you have a great offer now.

The opportunity cost of staying 18 months might be:

- Missed career growth (worth $100K+ over your lifetime)

- Mental health damage

- Losing the current opportunity

- 18 months of unhappiness

In this case, leave. The $50K isn't worth it.

The Bottom Line

When is the best time to leave a job for financial reasons?

Ideal timing:

- After bonuses and equity vest

- After 401(k) matches fully vest

- At the end of a month (for health insurance)

- When you have a new job lined up

But leave immediately if:

- Your health is suffering

- You have a time-sensitive opportunity

- The opportunity cost of staying outweighs what you're forfeiting

Money is important; but it's not everything. Don't let unvested equity trap you in a job that's destroying you.

At Chesapeake Financial Planners, we help clients evaluate job transitions strategically—weighing financial timing, career growth, and personal well-being.

Thinking about leaving your job? Let's build a plan.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.