You're ready to sell your business. After years of building value, you're finally going to cash out. Then your accountant drops the bomb: your tax bill could be 30%, 40%, or even 50% of your sale proceeds.

Suddenly, the $3 million exit that was supposed to fund your retirement becomes $2 million or less. That's a million dollars that disappears to federal and state governments instead of securing your financial future.

Business sale taxes are real, significant, and often shocking to owners who haven't planned ahead. But they're also manageable if you understand how they work and structure your sale strategically.

The philosophical truth: You shouldn't lose half your life's work to taxes because you didn't understand the rules.

The Baseline: What Most Business Owners Actually Pay

Let's start with the realistic range so you know what you're facing.

For most small to mid-sized business sales, total tax rates (federal and state combined) fall between 20% and 45% of your net proceeds. Where you land in that range depends on several factors:

Best case scenario: 15-23.8% federal capital gains (depending on income) + 0% state (in no-tax states like Florida or Texas) = 15-24% total

Typical scenario: 15-20% federal capital gains + 3.8% Net Investment Income Tax + 5-8% state tax = 24-32% total

Worst case scenario: 37% federal ordinary income (on certain portions) + 3.8% NIIT + 10-13% state tax (California, New York, New Jersey) = 40-50% total

Most business owners end up somewhere in the middle paying 25-35% in combined taxes. But the difference between 25% and 45% on a $2 million sale is $400,000. That's worth planning around. —

Capital Gains vs. Ordinary Income: The Core Distinction

The single most important factor determining your tax bill is whether your sale proceeds receive capital gains treatment or ordinary income treatment.

Capital Gains Tax Rates (The Better Option)

Long-term capital gains, profits from selling assets held over one year, face preferential rates:

- Federal rates: 0%, 15%, or 20% depending on your taxable income

- Net Investment Income Tax: Additional 3.8% if income exceeds $200,000 (single) or $250,000 (married)

- State taxes: Varies by state, from 0% to 13%+

- Combined typical rate: 18.8% to 23.8% federal, plus state

Ordinary Income Tax Rates (The Expensive Option)

Ordinary income faces your regular income tax bracket:

- Federal rates: 10% to 37% based on total income

- State taxes: Same as capital gains rates

- Self-employment tax: Usually doesn't apply to business sale proceeds

- Combined typical rate: 30% to 50%+ depending on bracket and state

The goal: Structure your sale to maximize capital gains treatment and minimize ordinary income treatment. —

What Determines Which Rate You Pay?

Whether you pay capital gains or ordinary income rates depends on your business structure and how the sale is structured.

Asset Sale vs. Stock Sale

Stock/Membership Interest Sale: Generally receives full capital gains treatment on the entire sale price. The buyer purchases your ownership stake.

Asset Sale: Different assets are taxed differently:

- Goodwill and intangibles: Capital gains rates

- Inventory and receivables: Ordinary income rates

- Equipment: Mix of capital gains and depreciation recapture (at 25% federal)

- Real estate: Capital gains rates with depreciation recapture

Buyers often prefer asset sales for tax reasons. Sellers prefer stock sales for the same reason your interests conflict.

Business Structure Impacts

- C Corporations: Can face double taxation on asset sales (once at corporate level, once when distributed). Stock sales avoid corporate-level tax.

- S Corporations: Pass-through taxation avoids double tax. Stock sales typically receive favorable capital gains treatment.

- Partnerships/LLCs: Flexible structures allow capital gains treatment in most cases, even with asset sales, if structured properly.

- Sole Proprietorships: Assets are sold individually, creating a mix of capital gains and ordinary income. —

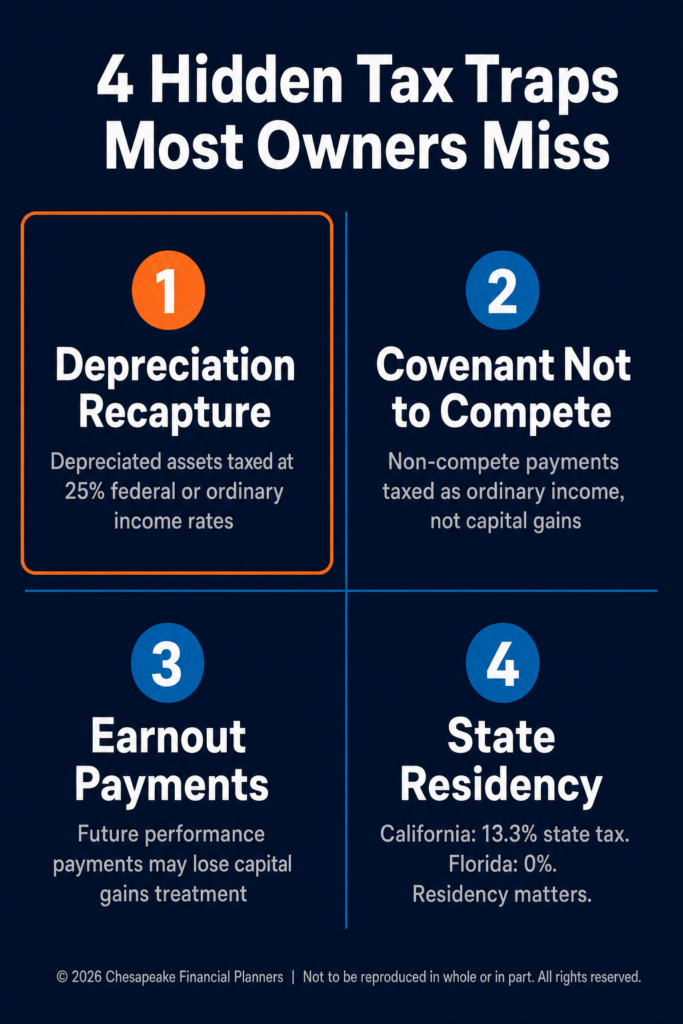

The Hidden Tax Traps Most Owners Miss

Beyond the basic structure, several lesser-known tax issues can dramatically increase your bill:

Depreciation Recapture

If you've depreciated equipment, vehicles, or buildings over the years, the IRS wants some of that back when you sell. Depreciation recapture is taxed at 25% federal (for real estate) or as ordinary income (for equipment)—higher than capital gains rates.

Impact: Businesses with significant depreciated assets can face surprise tax bills of tens or hundreds of thousands.

Covenant Not to Compete

If your sale agreement includes payments for agreeing not to compete, the IRS typically treats these as ordinary income—not capital gains. Buyers may push for allocating significant amounts here because it's deductible for them.

Watch out: Negotiate these allocations carefully with tax implications in mind.

Earnouts and Contingent Payments

Earnouts—additional payments based on future performance—can be taxed as ordinary income rather than capital gains, depending on how they're structured.

State Tax Residency

Where you live when you sell matters enormously. Selling while a California resident costs 13.3% state tax. Moving to Florida or Texas first? Zero state tax. That's a $266,000 difference on a $2 million sale.

Important: State residency changes must be legitimate and completed well before the sale. States aggressively challenge tax-motivated moves. —

Tax Strategies That Can Significantly Reduce Your Bill

Smart planning before closing can preserve hundreds of thousands of dollars:

Installment Sales

Spreading payments over multiple years spreads your tax bill across those years, potentially keeping you in lower brackets and deferring tax liability.

- Pros: Tax deferral, interest income on deferred payments

- Cons: Buyer default risk, locked into long-term arrangement

Qualified Small Business Stock (QSBS) Exclusion

C Corporation shareholders may exclude up to $10 million in gains (or 10x basis) from federal tax under Section 1202 if requirements are met.

- Requirements: Stock held 5+ years, active business, gross assets under $50 million at issuance

Impact: This is an enormous benefit—potentially eliminating all federal tax on millions in gains.

Charitable Remainder Trusts

Donating appreciated business interests to a charitable remainder trust (CRT) eliminates immediate capital gains tax while providing lifetime income and ultimate charitable benefit.

Opportunity Zone Reinvestment

Investing sale proceeds into Qualified Opportunity Zone funds defers capital gains and can reduce the ultimate tax bill through basis step-ups.

Timing and Income Management

Strategic timing around other low-income years, spreading the transaction across tax years, or coordinating with other deductions can reduce effective rates. —

What You Need to Do Now

Whether you're selling next year or in ten years, tax planning should start today:

3-5 Years Before Sale

- Optimize your entity structure. Converting from C Corp to S Corp (or vice versa) takes time to implement tax-efficiently. Some strategies require 5+ year holding periods.

- Review depreciation strategies. Understanding your recapture exposure helps you model your after-tax proceeds.

- Consider QSBS eligibility. If you're forming a new C Corp, structuring it properly for Section 1202 from day one creates enormous future benefit.

1-2 Years Before Sale

- Engage a tax advisor experienced in business sales. General accountants often lack expertise in complex business sale tax planning.

- Model multiple sale structures. Run scenarios showing after-tax proceeds under different deal structures.

- Consider residency moves if strategic. Legitimate moves to no-tax states must be completed well in advance.

During Negotiations

- Negotiate structure, not just price. A $2.5 million sale taxed at 23.8% nets more after-tax than a $3 million sale taxed at 40%.

- Fight for favorable purchase price allocations. Every dollar shifted from ordinary income to capital gains treatment is worth 10-20 cents in taxes.

- Involve your tax advisor in deal structuring. Post-closing tax planning is too late—the structure is set. —

Your Next Steps

The tax consequences of selling your business represent one of the largest financial planning challenges you'll face. The difference between proactive planning and reactive filing can easily exceed $500,000 on a typical small business sale.

Start here:

- Understand your current structure and its tax implications for a future sale

- Get preliminary tax modeling based on your expected sale price and timing

- Identify optimization opportunities that require advance planning

- Build a team including a business sale tax specialist, financial advisor, and attorney

- Create a timeline that ensures tax strategies are implemented before they're needed

You built value in your business over decades. Strategic tax planning ensures you keep more of what you've earned when it's time to exit.

Planning to sell your business? Schedule a consultation to discuss tax-efficient exit strategies.

The information provided is for educational purposes only and should not be construed as tax or legal advice. Tax laws are complex and subject to change. Business sale tax consequences depend on numerous factors including business structure, deal terms, and individual circumstances. Consult with qualified tax and legal professionals before making any business sale decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.