You're self-employed or a small business owner ready to get serious about retirement savings. You've heard about Solo 401(k)s and SEP IRAs both let you contribute tens of thousands annually with tax deductions. But which one is actually better for your situation?

The answer isn't the same for everyone. Choose wrong and you might leave $10,000-$20,000+ on the table in lost contributions or pay unnecessary administrative costs.

The Retirement Plan Confusion That Costs Business Owners

Here's the frustrating reality: Most business owners either don't save for retirement at all or pick a plan based on what their friend uses rather than what's optimal for their specific situation.

The external problem is comparing two similar but different plans. But the internal weight runs deeper: anxiety about falling behind on retirement savings, confusion about complex plan rules, and fear of making an expensive mistake.

Here's what you deserve: clarity about which plan maximizes YOUR retirement savings based on your income, age, employee situation, and goals—with simple implementation.

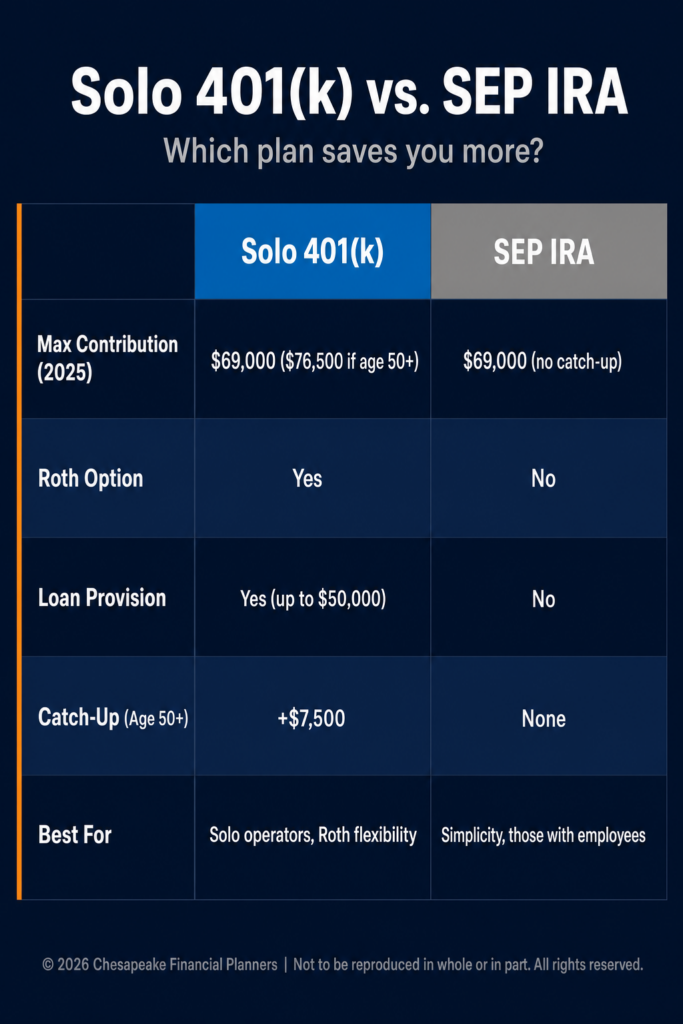

Solo 401(k) vs. SEP IRA: The Complete Comparison

We work with business owners building retirement wealth strategically. Here's how these plans compare:

Contribution Limits: Where More Might Be Possible

Solo 401(k) (2026):

- Employee deferrals: $24,500 ($32,500 if age 50+)

- Employer contributions: Up to 25% of compensation (20% of net self-employment income)

- Total limit: $72,000 ($80,000 if age 50+)

SEP IRA (2026):

- Employer contributions only: Up to 25% of compensation (20% of net self-employment income)

- Total limit: $72,000 (no catch-up provision)

Winner for contribution potential: Solo 401(k)

Why? The employee deferral component means you can often contribute more with a Solo 401(k), especially at lower income levels or if you're over 50.

Example 1: Age 52, net self-employment income $120,000

- Solo 401(k): $32,500 (employee) + $24,000 (employer 20%) = $56,500 total

- SEP IRA: $24,000 (employer 20%) = $24,000 total

- Advantage: Solo 401(k) by $32,500

Example 2: Age 42, net self-employment income $300,000

- Solo 401(k): $24,500 (employee) + $60,000 (employer 20%) = $72,000 total (hits limit)

- SEP IRA: $60,000 (employer 20%) = $60,000 total

- Advantage: Solo 401(k) by $12,000

Setup and Administration: The Simplicity Factor

SEP IRA:

- Setup time: 15 minutes

- Cost: Free to minimal

- Annual filing: None (unless assets exceed $250K)

- Record keeping: Minimal

- Plan document: Simple 1-page form

Solo 401(k):

- Setup time: 1-3 hours

- Cost: $0-$500 for setup, potentially $20-$100 annual custodian fees

- Annual filing: Form 5500-EZ required once assets exceed $250,000

- Record keeping: More detailed

- Plan document: Required (but provided by custodian)

Winner for simplicity: SEP IRA

If you value simplicity over every dollar of potential contribution, SEP IRA wins. It's the "set it and forget it" option.

Roth Options: Tax-Free Growth Potential

Solo 401(k):

- ✅ Can make Roth employee deferrals

- ✅ Can do in-plan Roth conversions

- Backdoor Roth IRAs remain available

SEP IRA:

- ❌ No Roth option—all contributions are pre-tax

- Backdoor Roth IRA complications (SEP IRA counts as traditional IRA for pro-rata rule)

Winner for Roth flexibility: Solo 401(k)

If you want tax-free growth in retirement or expect higher future tax rates, Solo 401(k)'s Roth options are valuable.

Loan Provisions: Access to Your Money

Solo 401(k):

- ✅ Can borrow up to $50,000 or 50% of vested balance

- Must repay with interest

- Can be useful for emergencies or business needs

SEP IRA:

- ❌ No loan provision

- Early withdrawal = 10% penalty + ordinary income tax

Winner for liquidity: Solo 401(k)

While we never recommend using retirement funds for non-retirement purposes, the loan option provides a safety valve if needed.

Employee Considerations: When You Grow

SEP IRA:

- ❌ Must contribute same percentage for all eligible employees

- Eligible: Employees 21+, worked 3 of last 5 years, earned $750+ in 2026

- If you contribute 20% for yourself, you must contribute 20% for qualifying employees

- Gets expensive fast with multiple employees

Solo 401(k):

- ✅ Only available if you have NO employees (except spouse)

- If you hire your first non-spouse employee, you must switch plans or exclude them (which has limitations)

- Stays cheap as long as it's just you (or you + spouse)

Winner for solo operators: Solo 401(k)

Winner if you have employees: Neither—you need a different plan

Contribution Flexibility: Variable Income

Both plans allow flexible contributions:

- You can contribute different amounts each year

- You can skip years if cash flow is tight

- No mandatory contributions

Tie on flexibility

This makes both ideal for businesses with variable income—unlike defined benefit plans which require fixed annual contributions.

Deadline for Contributions

Both plans:

- Contributions due by tax filing deadline (including extensions)

- For sole proprietors: Typically April 15 (or October 15 with extension)

Tie on deadline

You have the same window to make contributions for each plan type.

The Decision Framework: Which Plan for Your Situation

Choose Solo 401(k) if:

- You're over 50 (catch-up contributions add $8,000)

- You want Roth options for tax-free growth

- You're just you (or you + spouse) with no employees

- You want to maximize contributions at any income level

- You value the loan provision as an emergency backup

- You're willing to handle slightly more paperwork

Choose SEP IRA if:

- You value extreme simplicity

- You have a few employees and want to contribute for them

- Administrative burden is a major concern

- You're confident you won't need Roth options

- You're earning $300,000+ where both plans hit contribution limits anyway

Can You Have Both?

Short answer: No, not in the same year for the same business.

You can have either a Solo 401(k) OR a SEP IRA, but not both simultaneously. The contribution limits are combined across all employer plans.

However, if you have a W-2 job elsewhere with a 401(k), you CAN still have a Solo 401(k) or SEP for your side business—but the employee deferral limit ($24,500) is shared across all 401(k)s.

Implementation: Getting Started

For SEP IRA:

- Open SEP IRA account with any brokerage (Vanguard, Fidelity, Schwab, etc.)

- Complete Form 5305-SEP

- Make contributions before tax deadline

- Done

For Solo 401(k):

- Choose provider (Vanguard, Fidelity, Schwab, E*TRADE, or specialized providers)

- Complete plan adoption documents

- Obtain EIN for the plan (if required by provider)

- Open plan account

- Make contributions before tax deadline

- File Form 5500-EZ annually once assets exceed $250K

The Switching Question

Can you switch from SEP IRA to Solo 401(k) or vice versa?

Yes, but not mid-year. You can:

- Stop contributing to SEP IRA after current year

- Set up Solo 401(k) for next year

- Keep SEP IRA funds invested (or roll to Solo 401(k))

- Or do the reverse

Many business owners start with SEP IRA for simplicity, then switch to Solo 401(k) once they understand the contribution advantage and are willing to handle slightly more administration.

What Maximum Savings Looks Like

Imagine contributing $50,000-$70,000 annually to retirement with full tax deductions. Over 15 years at 7% growth, that's $1.7-2.4 million in retirement wealth—built systematically while reducing your current tax bill by $15,000-$25,000 annually.

That's the power of choosing the right retirement plan and maximizing contributions.

Your Clear Path to Maximum Retirement Savings

Here's how we help business owners optimize retirement contributions:

- Schedule a complimentary consultation to review your income, age, and business structure

- We'll calculate maximum contributions for Solo 401(k) vs. SEP IRA specific to your situation

- Together we'll implement the optimal plan and create a systematic contribution strategy

You've built a successful business. Let's make sure you're building retirement wealth to match.

Ready to maximize your retirement contributions? Schedule your consultation today.

This article is for educational purposes only and does not constitute tax or investment advice. Contribution limits are subject to change and may be affected by compensation levels and other factors. Plan selection has tax and administrative implications. Consult with qualified tax and financial professionals regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.