You've left your job, and now you're staring at your old 401(k) wondering: Should I move it to an independent financial advisor, or leave it where it is?

It's a critical decision, and the right answer depends on your situation. Let's break down your options, the pros and cons of each, and how to decide what's best for you.

Your 401(k) Rollover Options

When you leave a job, you have four main choices:

- Leave it in your old employer's plan — If your balance is over $5,000, most plans allow this.

- Roll it into your new employer's 401(k) — If your new job offers a 401(k), you can consolidate accounts.

- Roll it into an IRA managed by an independent advisor — Transfer it to an IRA where a financial planner manages it for you.

- Roll it into a self-directed IRA — Transfer it to an IRA where you manage it yourself (no advisor).

Let's focus on option 3—rolling it to an advisor—and compare it to the alternatives.

Why Move Your 401(k) to an Independent Financial Advisor?

Here are the key benefits of working with an advisor:

1. Professional Management

A financial advisor actively manages your investments based on your goals, risk tolerance, and timeline. They monitor your portfolio, rebalance regularly, and adjust as markets and your life change.

vs. a 401(k): Most 401(k) participants pick funds once and rarely revisit. An advisor provides ongoing oversight.

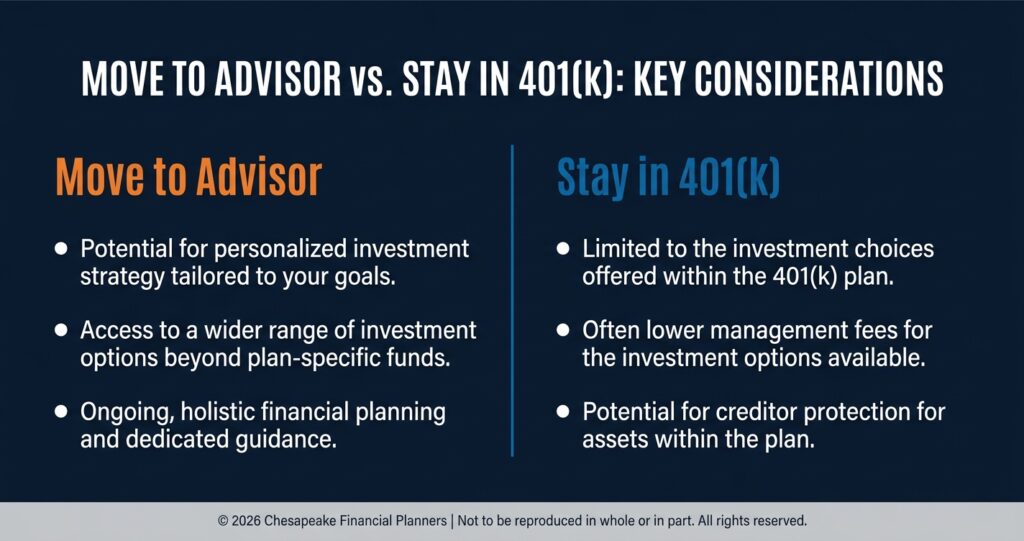

2. Personalized Investment Strategy

Advisors build portfolios tailored to your unique situation—not a one-size-fits-all target-date fund.

vs. a 401(k): 401(k) plans offer limited fund options (often 10-30 choices). An advisor has access to thousands of investment options.

3. Comprehensive Financial Planning

A good advisor doesn't just manage investments. They help with:

- Retirement planning

- Tax optimization

- Estate planning

- Insurance needs

- Social Security strategy

vs. a 401(k): A 401(k) is just an account. An advisor provides holistic guidance.

4. Consolidation and Simplicity

If you have multiple old 401(k)s scattered across former employers, rolling them into one IRA with an advisor simplifies tracking and management.

vs. a 401(k): Multiple 401(k)s = multiple logins, statements, and headaches.

5. Better Customer Service

Independent advisors work for you—not your employer. You get direct access to your planner, not a call center.

vs. a 401(k): 401(k) providers often have poor customer service and limited support.

6. More Investment Flexibility

IRAs offer access to individual equities, bonds, ETFs, mutual funds, REITs, and more. You're not limited to your employer's pre-selected menu.

vs. a 401(k): Limited to the funds your employer chose.

The Downsides of Moving to an Advisor

It's not all upside. Here are the potential drawbacks:

1. Fees

Financial advisors typically charge 0.5-1.5% of assets under management annually. On a $500,000 account, that's $2,500-7,500/year.

vs. a 401(k): Many 401(k) plans have low-cost index funds with expense ratios under 0.10%.

Key question: Does the advisor's value (planning, tax strategies, behavioral coaching) justify the fee? Often, yes—but not always.

2. Loss of 401(k) Protections

401(k)s have strong federal creditor protection under ERISA. IRAs have some protection, but it varies by state and is generally weaker.

vs. a 401(k): If you're in a high-liability profession (doctor, business owner), keeping money in a 401(k) may offer better asset protection.

3. Loss of Early Withdrawal Flexibility (If You're 55+)

If you leave your job at age 55 or later, you can take penalty-free withdrawals from your 401(k) under the "Rule of 55." This doesn't apply to IRAs—you'd have to wait until 59½.

vs. a 401(k): If you're planning early retirement and need access before 59½, keeping it in the 401(k) may be smarter.

4. Potential for Poor Advisor Selection

Not all advisors are created equal. A bad advisor can cost you more in poor performance, high fees, or bad advice than you'd lose in a mediocre 401(k).

Key question: Is the advisor a fiduciary? Do they have relevant credentials (CFP®)? Do they have a track record?

When You Should Move Your 401(k) to an Advisor

Consider rolling to an advisor if:

- You want personalized investment management — If you're not comfortable managing your own investments and want professional oversight, an advisor adds value.

- You're overwhelmed by financial planning — If you need help with retirement planning, taxes, estate planning, or insurance, an advisor provides comprehensive guidance.

- Your old 401(k) has high fees or poor options — If your 401(k) charges high fees or offers only expensive actively managed funds, an advisor with low-cost options may be better.

- You have multiple old 401(k)s — Consolidating into one IRA simplifies your financial life.

- You're nearing retirement and want a strategy — An advisor can help you build a withdrawal strategy, optimize Social Security, and coordinate all your assets.

- You value behavioral coaching — Studies show advisors' biggest value is keeping clients from making emotional, costly mistakes (panic-selling, chasing performance, etc.).

When You Should Not Move Your 401(k) to an Advisor

Keep your 401(k) where it is (or move to a self-directed IRA) if:

- Your 401(k) has excellent low-cost options — If your plan offers institutional-class funds with expense ratios under 0.10%, it's hard for an advisor to beat that after fees.

- You're between 55 and 59½ and may need money — The Rule of 55 allows penalty-free 401(k) withdrawals. Don't give that up unnecessarily.

- You're comfortable managing investments yourself — If you're knowledgeable and disciplined, a self-directed IRA at Vanguard, Fidelity, or Schwab may be cheaper than an advisor.

- You're planning to do backdoor Roth conversions — If you have no other Traditional IRA balances, keeping your 401(k) at your old employer (or rolling to a new one) preserves your ability to do clean backdoor Roth contributions.

- You value strong asset protection — If creditor protection is a priority, 401(k)s offer better federal protection than IRAs.

Self-Directed IRA vs. Advisor-Managed IRA

If you decide to roll your 401(k) out of your employer plan, you have two options:

Self-directed IRA (DIY):

- You manage your own investments

- Minimal fees (just fund expense ratios)

- Requires time, knowledge, and discipline

Advisor-managed IRA:

- Advisor manages investments and provides planning

- Higher fees (0.5-1.5% annually)

- Hands-off, professional guidance

Which is better? It depends on your confidence, time, and complexity. If your financial life is straightforward and you're investment-savvy, DIY works. If you want guidance, accountability, and comprehensive planning, an advisor is worth it.

Questions to Ask Before Moving Your 401(k)

If you're considering rolling to an advisor, ask:

- Is the advisor a fiduciary? — Fiduciaries are legally required to act in your best interest. Not all advisors are.

- What are the total fees? — Advisor fee + fund expense ratios = total cost. Make sure you understand what you're paying.

- What services are included? — Investment management only? Or comprehensive financial planning (retirement, tax, estate, insurance)?

- What's the investment philosophy? — Do they use low-cost index funds or expensive active funds? What's their approach to risk?

- What are my 401(k) options? — Compare your current 401(k)'s fees and investment options to what the advisor offers.

- What's the advisor's track record? — How long have they been in business? What credentials do they have? Can they provide references?

The Bottom Line

Should you move your 401(k) to an independent financial advisor?

Yes, if:

- You want comprehensive financial planning and professional investment management

- Your old 401(k) has high fees or poor options

- You value behavioral coaching and accountability

- You have multiple accounts to consolidate

No, if:

- Your 401(k) has excellent low-cost options

- You're comfortable managing investments yourself

- You're between 55-59½ and may need penalty-free withdrawals

- You value strong creditor protection

The key: Don't move your 401(k) on autopilot. Evaluate your options, compare costs, and choose what aligns with your goals and situation.

At Chesapeake Financial Planners, we help clients evaluate their 401(k) rollover options and build comprehensive financial strategies—so you're making informed decisions, not guesses.

Wondering what to do with your old 401(k)? Let's review your options together.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual.

Before rolling over, consider all of your options including leaving assets in your former employer's plan, rolling into a new employer's plan, or taking a cash distribution (taxes and possible withdrawal penalties may apply). Considerations may include, but are not limited to, investment options, fees and expenses, services, withdrawal penalties, protection from creditors and legal judgments, required minimum distributions, and employer stock holdings.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.