After decades of service, you've reached a crossroads: your employer is offering you a choice between a monthly pension for life or a one-time lump sum payout. You've chosen the lump sum—or perhaps it was your only option—and now you're holding a check for $400,000, $600,000, or more.

Congratulations. You've just become your own pension manager.

The question that keeps you awake at night: How do you make this money last for a retirement that could span 30 years or more?

The Core Challenge: You're Building Your Own Pension

When you accept a pension lump sum instead of monthly payments, you're trading guaranteed lifetime income for control and flexibility. That trade-off comes with responsibility.

Your employer's pension would have provided a paycheck every month until you died, no matter how long you lived or what the market did. Now, that's your job.

The good news? With proper planning, you can often create as much or more income than the pension offered, while retaining control over your assets and the ability to leave money to heirs.

Step 1: Calculate Your Sustainable Withdrawal Rate

The traditional "4% rule" suggests you can withdraw 4% of your portfolio's initial value, adjusted for inflation each year, with a reasonable expectation of making your money last 30 years.

But the 4% rule was designed for traditional retirement (age 65). If you're retiring earlier or want more conservative planning:

- Age 55-60: Consider 3-3.5% withdrawal rate

- Age 60-65: 3.5-4% may be appropriate

- Age 65+: 4-4.5% becomes more sustainable

For a $500,000 lump sum at age 60, a 3.5% withdrawal rate provides approximately $17,500 in the first year.

Is that enough to cover your needs, combined with Social Security and other income sources? If yes, you're on track. If no, you need to either reduce expenses, work longer, or find additional income.

Step 2: Build a Three-Bucket Strategy

One of the most effective ways to manage a pension lump sum is the bucket approach:

Bucket 1: Cash Reserve (Years 1-2)

Keep 1-2 years of expenses in cash or money market funds. This is your immediate spending money.

- Purpose: Avoid selling investments during market downturns

- Amount: $50,000-$100,000 for most retirees

- Investment: High-yield savings, money market funds, short-term CDs

Bucket 2: Income Generator (Years 3-10)

This bucket focuses on stability and income generation.

- Purpose: Provide reliable income and principal protection

- Allocation: 40-50% of total portfolio

Investments:

- Investment-grade bonds or bond funds

- Dividend-paying stocks

- Balanced funds

- Short-term bond ladder

Bucket 3: Growth Engine (Years 10+)

This is your long-term growth allocation.

- Purpose: Outpace inflation and provide growth

- Allocation: 30-50% depending on risk tolerance and age

Investments:

- Diversified stock funds

- Index funds (S&P 500, total market)

- International stocks

- Real estate (REITs)

As you spend from Bucket 1, refill it from Bucket 2. As Bucket 2 depletes, refill it from Bucket 3. This creates a systematic rebalancing approach that forces you to "sell high" from your growth positions to refill your near-term buckets.

Step 3: Coordinate with Social Security

Your pension lump sum doesn't exist in isolation—it's part of a comprehensive retirement income strategy that includes Social Security.

Key Decisions:

- Claiming age: Every year you delay Social Security from 62 to 70 increases your benefit by roughly 7-8%. Your pension lump sum can bridge the gap, allowing you to delay claiming and maximize lifetime benefits.

- Spousal coordination: If you're married, optimizing both spouses' claiming strategies while using your lump sum for current income can significantly increase household lifetime income.

- Break-even analysis: Calculate when the higher benefit from delayed claiming breaks even with earlier, smaller benefits. Your lump sum provides flexibility to optimize this decision.

Step 4: Tax-Efficient Withdrawal Sequencing

Where you take money from matters as much as how much you take.

General Withdrawal Sequence:

- Taxable accounts first (brokerage accounts, non-retirement savings)

- Tax-deferred accounts next (traditional IRA, 401(k), pension rollover)

- Tax-free accounts last (Roth IRA)

This sequence typically minimizes lifetime taxes, though your specific situation may vary.

Exceptions and Nuances:

- Roth conversions: In lower-income years before Social Security and RMDs begin, consider converting some traditional IRA money to Roth. Your pension lump sum (if in a taxable account) can cover living expenses while you fill up lower tax brackets with conversions.

- Capital gains harvesting: If you're in the 10-12% tax bracket, you may pay 0% on long-term capital gains. Harvest gains strategically in these years.

- Tax diversification: Having money in taxable, tax-deferred, and tax-free accounts gives you flexibility to manage your tax bracket in retirement.

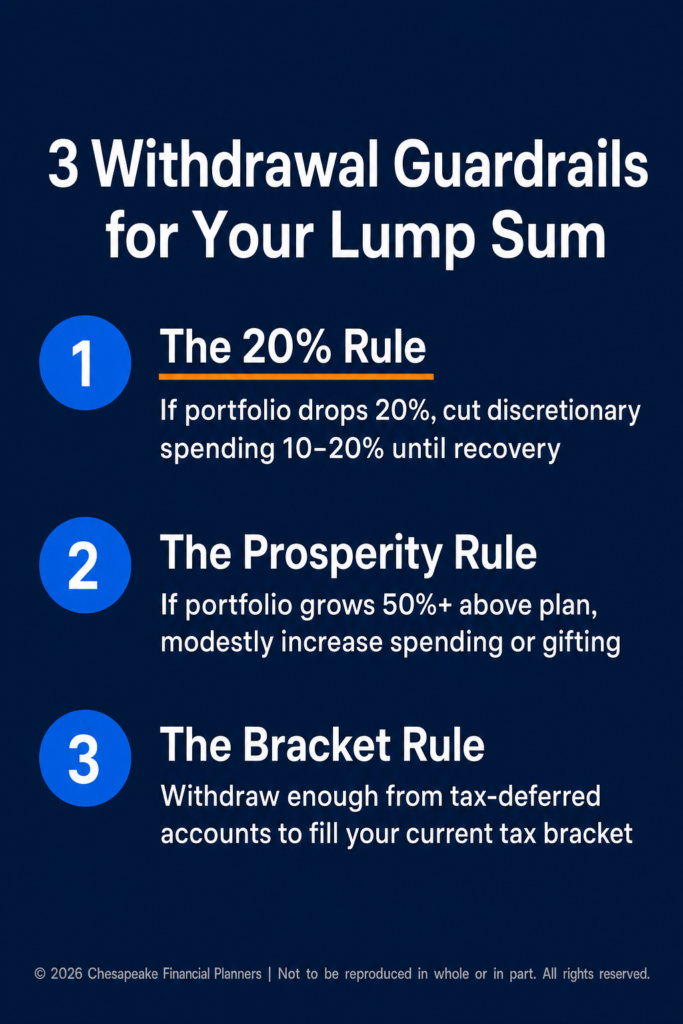

Step 5: Create Guardrails

Rigid withdrawal rates don't adapt to reality. Create flexible guidelines:

The 20% Rule

If your portfolio declines 20% or more from its peak, reduce discretionary spending by 10-20% until recovery.

The Prosperity Rule

If your portfolio grows significantly beyond your initial planning assumptions (e.g., 50% above your starting value), you can modestly increase spending or accelerate goals like gifting to heirs.

The Bracket Rule

Withdraw enough from tax-deferred accounts to "fill up" your current tax bracket, even if you don't need the money. This can reduce future RMDs and avoid bracket creep later.

Step 6: Don't Forget Healthcare

Before age 65, you'll need healthcare coverage. Budget $1,000-$1,500 per person per month for marketplace insurance—more if you have health issues.

After 65, Medicare Part B, Part D, and supplemental coverage (Medigap or Medicare Advantage) will cost $300-$600+ per month per person.

Healthcare costs often represent one of the largest retirement expenses after housing. Don't underestimate them.

Step 7: Annual Review and Rebalancing

At least once per year:

- Review your spending vs. your withdrawal plan

- Rebalance your portfolio to target allocation

- Refill your cash bucket from income and gains

- Assess whether guardrails suggest spending adjustments

- Update projections based on portfolio performance and life changes

Common Mistakes to Avoid

- Being too conservative: An all-bond portfolio won't keep up with inflation over 30 years. You need growth.

- Being too aggressive: Losing 40% in a market crash and panic-selling locks in losses. You need stability.

- Ignoring inflation: $50,000 today needs to be $100,000 in purchasing power in 24 years at 3% inflation.

- Spending windfalls: That unexpected $30,000 tax refund or inheritance isn't "extra"—it's part of your long-term security.

- Failing to adjust: Markets change, life changes, expenses change. Your plan must adapt.

When to Get Professional Help

Consider working with a financial advisor if:

- Your lump sum exceeds $300,000

- You're retiring before age 65

- You have complex tax situations

- You're unsure about asset allocation

- You want accountability and behavioral coaching

The cost of good advice is often far less than the cost of mistakes.

The Bottom Line

Making a pension lump sum last requires converting a one-time windfall into decades of reliable income. It's part math, part discipline, and part flexibility.

With a sustainable withdrawal rate, diversified three-bucket strategy, tax-efficient sequencing, and flexible guardrails, you can create your own pension—one that provides income for life while giving you control over your financial future.

Your employer handed you responsibility along with that lump sum check. With the right strategy, you can carry that responsibility confidently through a long, secure retirement.

This information is for educational purposes only and should not be considered investment or tax advice. Withdrawal strategies and rates should be tailored to individual circumstances, risk tolerance, and time horizon. Past performance does not guarantee future results.

Asset allocation and diversification do not ensure a profit or protect against loss.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.