If you've been thinking about hiring a financial planner but worry you don't have enough money to qualify, you're not alone. Many people delay getting professional financial guidance because they assume advisors only work with wealthy clients who have millions to invest.

The reality is more nuanced. While some advisors do have high minimums, many work with clients at various wealth levels, including business owners who are still building wealth but need sophisticated planning around business strategy, exit planning, and tax optimization.

Here's what you actually need to know about advisor minimums and when it makes sense to work with a financial planner, regardless of your current asset level.

The Wide Range of Advisor Minimums

Financial advisors set minimums based on their business model, expertise, and target clientele. The range is enormous.

No minimum

Some fee-only planners, especially those who charge hourly or flat fees rather than asset-based fees, have no minimum. If you can pay their planning fee, they'll work with you.

$100,000–$250,000

Many advisors who charge asset-based fees (typically around 1% of assets under management) set minimums in this range. They need enough assets to generate fees that justify the time spent on comprehensive planning.

$500,000–$1 million

Advisors who specialize in complex planning, business owners, high-net-worth individuals, or those approaching retirement: often have higher minimums because their services are more specialized.

$2 million+

Some wealth management firms focus exclusively on high-net-worth clients and set minimums accordingly.

The takeaway

Advisor minimums vary dramatically. The question isn't "Do I have enough?" It's "Which advisors serve clients at my wealth level and understand my specific situation?"

When Minimums Don't Tell the Full Story

Here's what most people misunderstand: minimums are often flexible, especially for business owners with complex financial situations.

Business owners are different

An advisor might require $500,000 in investable assets for typical clients but work with business owners who have $200,000 in liquid assets plus a business worth $2 million. Why? Because business owners need sophisticated planning around exit strategy, tax optimization, and business-personal finance integration that justifies the advisor's time regardless of current liquid assets.

Planning complexity matters more than asset size

A business owner planning to sell within five years and needing exit planning, tax strategy, and post-sale wealth management represents a more valuable client relationship than someone with $1 million who just needs basic investment management.

Life stage and trajectory count

Advisors who specialize in business owners often work with clients whose wealth is largely concentrated in their business today but will become liquid upon exit. They're willing to start the relationship before the liquidity event because they understand the full wealth picture.

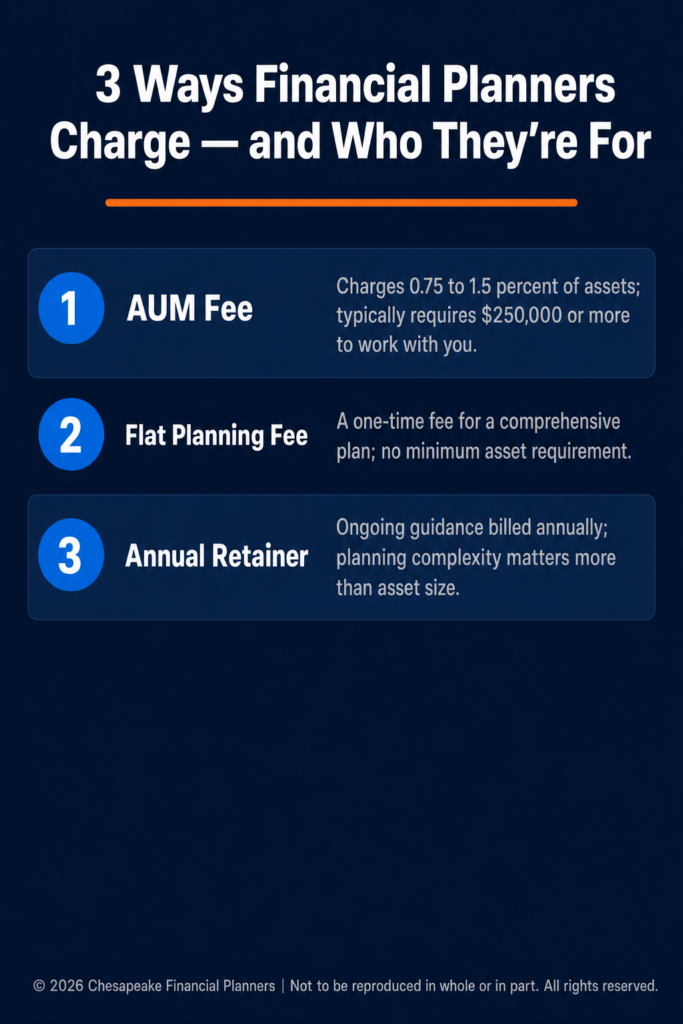

Asset-Based Fees vs. Planning Fees

The minimum you need depends heavily on how the advisor charges.

Asset-based fee model (AUM)

Advisors who charge a percentage of assets under management (typically 0.75%–1.5%) need sufficient assets to generate meaningful revenue. If you have $250,000 and the advisor charges 1%, they earn $2,500 annually. That might not cover the cost of comprehensive financial planning.

This model creates a natural minimum threshold. Most AUM-based advisors won't work with clients below $250,000–$500,000 because the economics don't work.

Flat fee or hourly model

Advisors who charge planning fees ($3,000–$10,000 for a comprehensive plan) or hourly rates ($200–$500/hour) don't need asset minimums. You pay directly for their time and expertise, regardless of your asset level.

Retainer model

Some advisors charge ongoing annual retainer fees ($5,000–$15,000+) for comprehensive planning and ongoing advice. Asset size matters less than whether you value and can afford the retainer.

For business owners specifically

Look for advisors who offer planning fees or retainers in addition to or instead of AUM fees. This allows you to access sophisticated planning before you have substantial liquid assets.

When It Makes Sense to Hire a Planner (Regardless of Assets)

Don't focus solely on whether you meet a minimum. Focus on whether you need the services a financial planner provides.

You should consider hiring a financial planner if:

- You own a business and plan to exit within 10 years. Exit planning, business valuation, tax strategy, and wealth preservation after sale are complex enough to justify professional guidance even if your current liquid assets are modest.

- Your financial situation is complex. Multiple income streams, concentrated business ownership, irregular cash flow, stock options, or significant tax considerations all create complexity that benefits from professional guidance.

- You're making high-stakes decisions. Should you sell your business now or wait? How should you structure the sale? What should you do with sale proceeds? These decisions have million-dollar implications. Professional guidance pays for itself.

- You're not on track for your goals. If you're uncertain whether you're saving enough, investing appropriately, or positioned to retire when you want, a financial planner can provide clarity and a roadmap.

- You want to optimize taxes. Business owners often overpay taxes because they don't have coordinated strategies around entity structure, owner compensation, and retirement plan design. A planner who specializes in business owners can identify opportunities worth tens of thousands annually.

What to Look for in an Advisor (Beyond Minimums)

Once you've identified advisors who work with clients at your asset level, evaluate them based on expertise, not just whether you qualify.

- Business owner expertise: Do they regularly work with business owners? Can they discuss exit planning, business valuation, and coordinated tax strategies? Or do they primarily serve corporate executives and retirees?

- Planning approach: Do they provide comprehensive financial planning, or just investment management? Business owners need the former.

- Fee transparency: Are their fees clear and reasonable given the services provided? Can they explain exactly what you'll pay and what you'll receive?

- Fiduciary status: Do they operate as a fiduciary 100% of the time, legally required to put your interests first?

- Coordination with other professionals: Will they work with your CPA and attorney to create coordinated strategies, or do they operate in isolation?

Alternatives If You Don't Meet Minimums

If you don't meet minimums for comprehensive wealth management but need financial guidance, consider these alternatives:

- Hourly or project-based planning: Find a fee-only planner who will create a comprehensive financial plan for a flat fee ($3,000–$7,000). You implement the plan yourself, avoiding ongoing asset-based fees and minimums.

- Robo-advisors with planning add-ons: Services like Vanguard Personal Advisor or Schwab Intelligent Portfolios offer lower minimums ($25,000–$50,000) with some access to human advisors, though planning is less comprehensive than full-service advisors.

- Financial coaches or planners targeting your stage: Some advisors specialize in working with younger business owners or those still building wealth. They often have lower minimums because they're building their practices and targeting your demographic.

- DIY with CPA coordination: If your primary need is tax optimization and you have a good CPA, work closely with them on business tax strategy while managing investments yourself through low-cost index funds.

The Cost of Waiting

Here's what business owners often don't consider: the cost of waiting until you have "enough" to work with an advisor.

- Missed tax opportunities compound. If restructuring your entity or optimizing owner compensation could save you $20,000 annually in taxes, waiting three years costs $60,000. That's far more than advisor fees.

- Exit planning takes time. Businesses positioned for sale 5–10 years in advance typically sell for 20–40% more than businesses sold quickly out of necessity. If your business is worth $2 million and proper exit planning could increase that by 25%, that's $500,000 dwarfing any advisor fees.

- Suboptimal investment strategies cost returns. If your investments are poorly allocated, too conservative, or too aggressive for your situation, you're giving up returns or taking unnecessary risks every year you wait.

The Real Question

The question isn't "How much money do I need to work with a financial planner?" The real question is "Am I in a situation where professional financial guidance would create enough value to justify the cost?"

For business owners, the answer is often yes, even if your liquid assets are modest, because the planning opportunities around business strategy, tax optimization, and exit preparation create enormous value that far exceeds advisor fees.

Don't let arbitrary asset minimums keep you from getting guidance you need. Seek out advisors who work with business owners at your stage, understand your complexity, and can demonstrate how their planning will create value specific to your situation.

If an advisor tells you that you don't qualify based solely on liquid assets without considering your business ownership, full financial picture, and planning needs, you're probably talking to the wrong advisor. Keep looking.

This article is for educational purposes only and should not be construed as specific financial advice. Consider consulting with a qualified financial professional regarding your individual circumstances.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.