Your company offers an ESPP with a 15% discount and a lookback provision.

You're not participating.

Why? "I don't want more exposure to company stock. Plus, taxes are complicated."

Fair. But you're leaving 15-30% annualized returns on the table. Guaranteed. Risk-free (ish).

Let me explain why you're wrong, and what you should do instead.

The ESPP Arbitrage Most People Miss

Here's how a typical ESPP works:

- You contribute up to 15% of your salary (post-tax) via payroll deduction

- Contributions accumulate for 6 months (the "offering period")

- At the end of the period, the company buys stock for you at a 15% discount

- The discount is applied to the lower of the stock price on the first day or the last day of the period (the "lookback provision")

Let's say the stock is $100 on day 1 and $120 on day 180.

Your purchase price: $100 × 0.85 = $85

You immediately own stock worth $120 that you paid $85 for. That's a 41% gain in 6 months.

Annualized, that's an 82% return.

Even if the stock stayed flat at $100, you still made 15% in 6 months (30% annualized).

And here's the key: you can sell the stock immediately.

You're not taking long-term concentration risk. You're capturing the discount and getting out.

The Tax Treatment (It's Not That Complicated)

ESPP tax treatment depends on how long you hold the shares:

Disqualifying disposition (sell within 2 years of grant OR 1 year of purchase):

- The discount is taxed as ordinary income (W-2 wages)

- Any additional gain is short-term or long-term capital gains, depending on holding period

Qualifying disposition (hold for 2+ years from grant AND 1+ year from purchase):

- Part of the gain is ordinary income, part is long-term capital gains

- Slightly better tax treatment, but you're holding concentrated stock for 2 years

Most people should do a disqualifying disposition and sell immediately. Here's why:

- You lock in the 15-30% gain immediately

- You avoid concentration risk

- The tax treatment difference is minimal (ordinary income vs. long-term cap gains is ~10-15 percentage points)

- You can redeploy the cash into a diversified portfolio

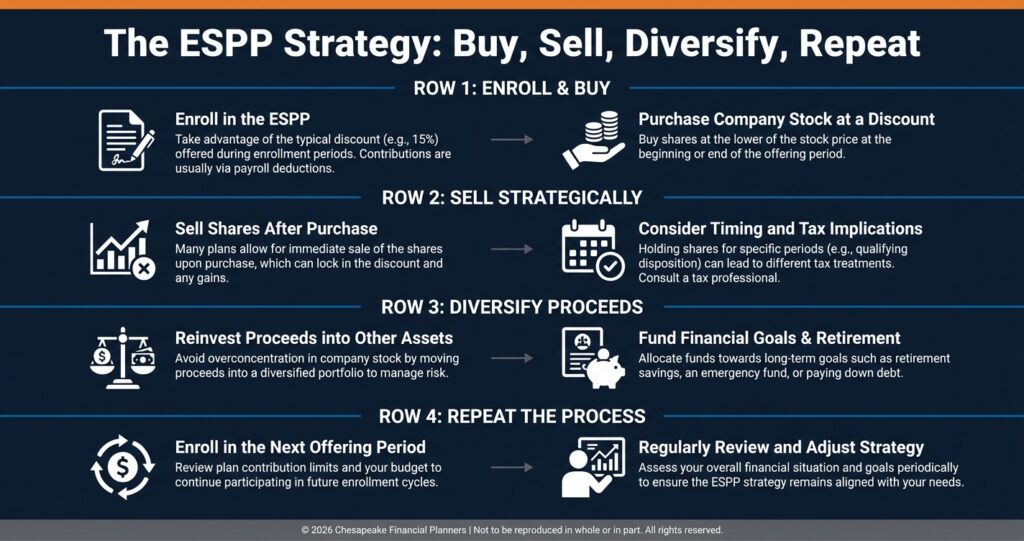

The Strategy: Buy, Sell, Diversify, Repeat

Here's what you should actually do:

1. Contribute the maximum your ESPP allows (usually 15% of salary)

Yes, this reduces your take-home pay. But you're only waiting 6 months to get it back plus a 15-30% return.

2. Sell immediately at the end of each offering period

Don't hold. Don't wait for long-term cap gains treatment. Don't try to time the top. Sell at purchase and lock in the gain.

3. Set aside the taxes

The discount will show up as W-2 income. Set aside 35-40% for federal + state + FICA taxes. Don't spend the full proceeds.

4. Reinvest in a diversified portfolio

Take the after-tax proceeds and invest in index funds, bonds, whatever your asset allocation calls for.

You've just converted a 6-month concentrated bet into a long-term diversified position.

5. Repeat every 6 months

This is a rinse-and-repeat strategy. Every offering period, you're capturing another 15-30% gain.

The Math on Why This Is Worth It

Let's say you make $200K and contribute 10% to your ESPP.

- Annual contribution: $20,000

- Per offering period (6 months): $10,000

- Purchase price after 15% discount: $8,500 buys $10,000 worth of stock

- Immediate gain: $1,500 (before taxes)

- After-tax gain (~40% tax rate): $900

You make $900 every 6 months, or $1,800/year, just from the discount.

That's a 9% return on the $20,000 you contributed. And if the stock went up during the offering period, the return is even higher.

Annualized, this is a 15-30% guaranteed return on the capital you contribute.

Show me another investment that does that.

The Risks (There Are Some)

1. Stock drops sharply during the offering period

If the stock is $100 on day 1 and $70 on day 180, your purchase price is $70 × 0.85 = $59.50.

You own stock worth $70 that you paid $59.50 for. You still made 17.6%.

But if the stock drops to $50 right after purchase, you're underwater. This is why you sell immediately to avoid post-purchase drops.

2. Liquidity crunch during the contribution period

You're diverting 10-15% of your salary for 6 months. If you need that cash for emergencies, you can't access it until the offering period ends.

Solution: only contribute what you can afford to have locked up for 6 months. Keep your emergency fund intact.

3. Trading blackout periods

If you're subject to insider trading blackouts, you might not be able to sell immediately after purchase. This increases your risk if the stock drops post-purchase.

Check your company's trading policy before enrolling.

When You Should NOT Participate

1. You don't have an emergency fund

If you're living paycheck to paycheck, don't divert 10-15% of your income into an ESPP. Build your emergency fund first.

2. You have high-interest debt

If you're carrying credit card debt at 20% APR, pay that off before optimizing ESPP contributions.

3. Your company is in serious financial trouble

If there's a real risk of bankruptcy or delisting, the ESPP discount might not be worth the risk of holding illiquid shares.

4. Your ESPP doesn't have a discount or lookback

Some ESPPs are just "buy stock at market price with after-tax dollars." That's not an arbitrage. Don't bother.

What to Do Right Now

If you're not enrolled in your ESPP:

- Check if your company offers a discount (10-15% is standard)

- Check if there's a lookback provision (this doubles your upside)

- Enroll in the next offering period at the max contribution you can afford

- Plan to sell immediately at purchase

If you're already enrolled but holding the shares:

- Sell everything from prior offering periods

- Reinvest in a diversified portfolio

- Set up auto-sell for future purchases if your plan allows it

If you're not sure about the tax impact:

- Talk to a tax advisor before the next offering period

- Model the after-tax return

- Make sure you're withholding enough on your W-4 to cover the additional income

The Bottom Line

ESPPs with a 15% discount and lookback provision are the closest thing to free money you'll find in tech comp.

Yes, the tax treatment is annoying. Yes, it reduces your paycheck for 6 months. But the after-tax return is 15-30% annualized guaranteed.

Participate. Sell immediately. Diversify. Repeat.

This is the one piece of equity comp you should max out without hesitation.

All investing involves risk, including the potential loss of principal. This article is for educational purposes and does not constitute investment advice.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.