A buyout changes everything. Whether you're selling your share of a partnership, accepting an offer from a co-owner, or negotiating your exit from a business you built, one question looms larger than all the others: how much of this money will I actually keep?

The tax consequences of a business buyout can be staggering, or manageable. The difference comes down to structure, timing, and planning. Business owners who walk into buyouts without understanding the tax implications often discover they'll keep far less than they expected. Some face tax bills that consume 40% or more of their proceeds.

You've earned this money. Understanding the tax landscape ensures you keep as much of it as legally possible.

The Core Tax Issue: How Is Your Buyout Structured?

The tax treatment of your buyout depends fundamentally on one question: are you selling assets or ownership interests?

Asset Sale vs. Stock Sale

In an asset sale, the buyer purchases the business's assets (equipment, inventory, customer lists, goodwill). You, the seller, typically face higher taxes because different assets are taxed at different rates.

In a stock or membership interest sale, the buyer purchases your ownership stake in the entity itself. This typically results in capital gains treatment, which is usually more favorable than asset sale treatment.

The catch: Buyers typically prefer asset sales because they get better tax treatment and can pick and choose what they buy. Sellers prefer stock sales for the opposite reason. This creates negotiation tension, and the party with more leverage usually wins.

C Corporation vs. S Corporation vs. Partnership/LLC

Your business structure dramatically impacts your tax bill:

C Corporations face potential double taxation on asset sales once at the corporate level and again when proceeds are distributed to shareholders. Stock sales avoid corporate-level tax but may face higher capital gains rates on some assets.

S Corporations generally pass income through to owners, avoiding double taxation. Stock sales typically receive favorable capital gains treatment. Asset sales can still work, though depreciation recapture applies to certain assets.

Partnerships and LLCs (taxed as partnerships) offer the most flexibility. Properly structured, you can often achieve capital gains treatment while buyers get the step-up in basis they want.

The Tax Rates You'll Actually Face

Understanding the specific taxes that apply helps you estimate your after-tax proceeds:

Capital Gains Tax

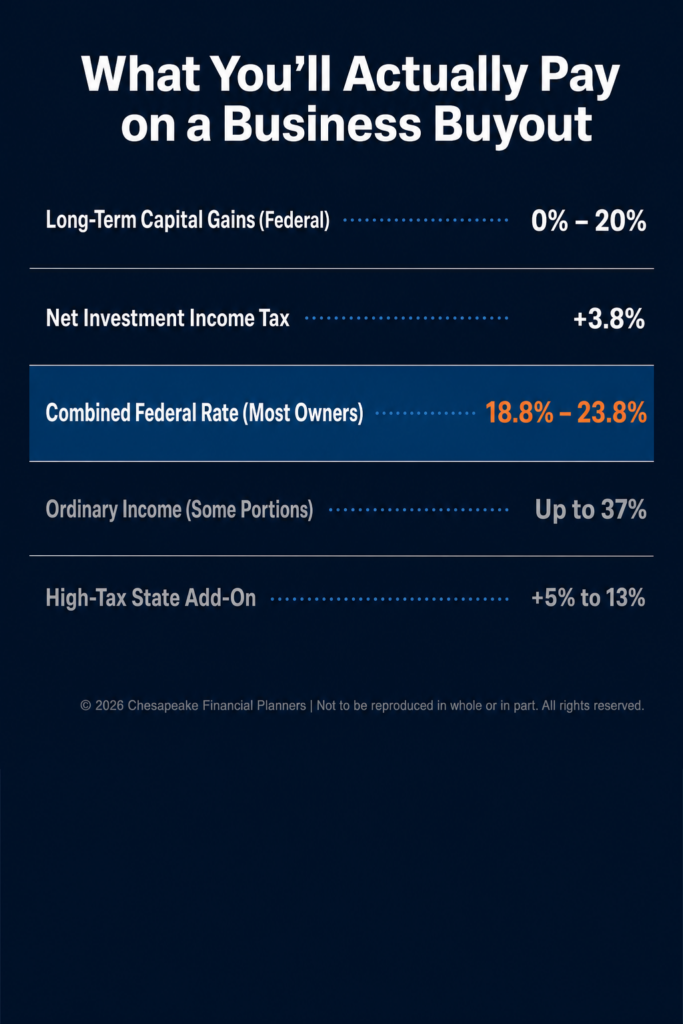

Profits from selling business interests held longer than one year face long-term capital gains rates:

- 0%, 15%, or 20% depending on your income level

- Plus 3.8% Net Investment Income Tax if your income exceeds certain thresholds ($200,000 single, $250,000 married)

Bottom line: Most business owners face combined federal capital gains rates of 18.8% to 23.8%.

Ordinary Income Tax

Some portions of your buyout may face ordinary income rates (currently 10% to 37% federal):

- Depreciation recapture on equipment and property

- Compensation agreements structured as salary or consulting

- Covenant not to compete payments

- Inventory and receivables (for asset sales)

State Taxes

Don't forget your state. Some states don't tax capital gains differently from ordinary income. Others have no income tax at all. If you're in California, New York, or New Jersey, add 5-13% to your tax bill. If you're in Texas, Florida, or Nevada, you pay zero state tax on the transaction.

Deal Structure Decisions That Impact Your Tax Bill

How your buyout is structured determines which tax rates apply to which portions. Every dollar matters.

Allocation of Purchase Price

In asset sales, the purchase price must be allocated across different asset categories. Some receive favorable capital gains treatment, others don't:

Capital assets (goodwill, customer relationships): Capital gains rates

Ordinary income assets (inventory, receivables): Ordinary income rates

Depreciable assets (equipment, buildings): Mix of capital gains and recaptured depreciation

The allocation you negotiate with the buyer directly impacts your tax bill. Buyers want allocations that maximize their deductions. Your interests often conflict.

Installment Sales

Taking payment over time through an installment sale can spread your tax liability across multiple years, potentially keeping you in lower tax brackets.

Benefits: Tax deferral, potentially lower overall rates, collects interest on unpaid balance

Risks: Buyer default, tax law changes, locked into long-term arrangement

Earnouts and Contingent Payments

Earnouts: additional payments based on future business performance, create tax uncertainty. The IRS may treat these as ordinary income rather than capital gains, depending on structure.

Tax Strategies to Potentially Reduce Your Bill

Smart planning before and during buyout negotiations can preserve significantly more of your proceeds:

Qualified Small Business Stock (QSBS) Exclusion

If your business is a C Corporation and qualifies under Section 1202, you may be able to exclude up to $10 million in gains or 10x your basis from federal tax. This is an enormously valuable provision that many business owners miss.

Requirements: Must be C Corp stock held over 5 years, active business, gross assets under $50 million at issuance.

Opportunity Zone Deferral

Investing capital gains into Qualified Opportunity Zone funds allows you to defer the tax bill and potentially reduce it through basis step-ups.

Charitable Giving Strategies

Donating appreciated business interests to charity or using charitable trusts can eliminate capital gains while creating income tax deductions and achieving philanthropic goals.

Timing and Income Management

Spreading the transaction across multiple tax years or timing it with lower-income years can reduce your effective rate. This requires careful planning and may impact deal terms.

The Mistakes That Cost Business Owners the Most

Avoid these common errors that turn manageable tax bills into painful ones:

- Mistake 1: Negotiating deal terms without understanding tax implications. Structure matters as much as price.

- Mistake 2: Failing to involve a tax professional early. Post-transaction planning is too late; the structure is already set.

- Mistake 3: Not considering state tax implications. Moving to a no-tax state before a sale can save hundreds of thousands.

- Mistake 4: Ignoring depreciation recapture. Businesses with significant equipment or property face surprise tax bills on recaptured depreciation.

- Mistake 5: Accepting unfavorable purchase price allocations. Fight for allocations that minimize ordinary income treatment.

Your Next Steps

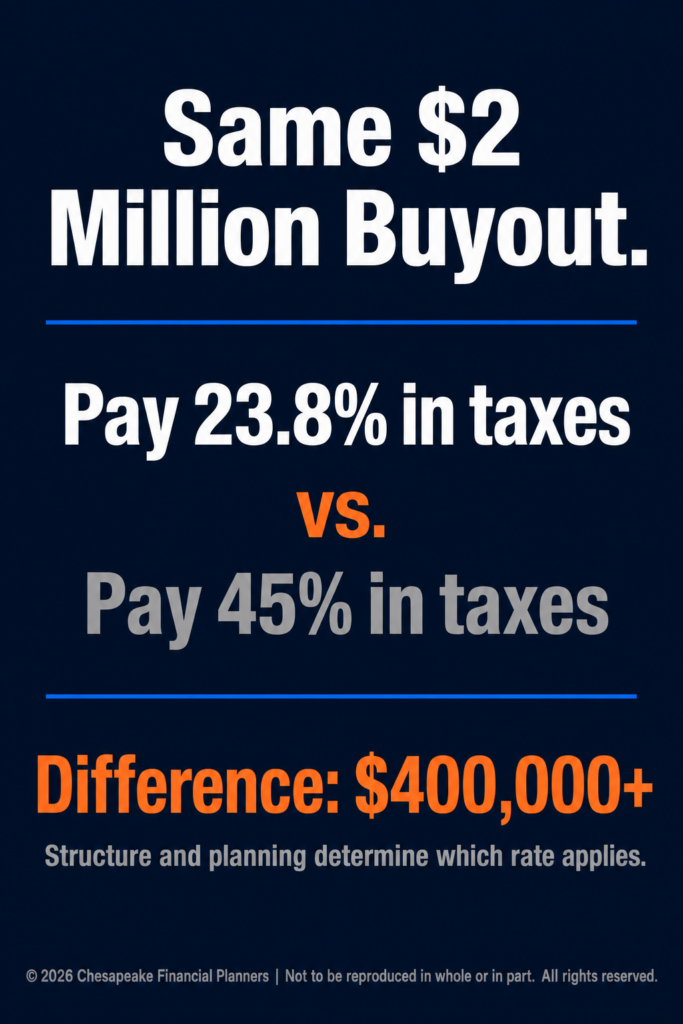

A business buyout represents a potentially life-changing financial event. The difference between paying 23.8% and 45% in taxes on a $2 million buyout is over $400,000 money that either funds your next chapter or disappears to the IRS.

Here's what you should do:

- Engage a tax advisor experienced in business sales before you begin serious negotiations

- Model different deal structures to understand tax implications of each approach

- Consider your complete financial picture how does this transaction fit into retirement planning, estate planning, and investment strategy?

- Negotiate structure, not just price sometimes a lower purchase price with better tax treatment nets more after-tax dollars

You worked hard to build value in your business. Strategic tax planning ensures you keep more of what you've earned.

Facing a business buyout? Schedule a consultation to discuss tax-efficient exit strategies for business owners.

The information provided is for educational purposes only and should not be construed as legal or tax advice. Tax laws are complex and subject to change. Buyout tax consequences depend on individual circumstances, business structure, and specific deal terms. Consult with qualified tax and legal professionals before proceeding with any business transaction.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.