One of the most common questions people ask (and one of the most anxiety-inducing) is whether they're saving enough. You're putting money away each month, but is it enough to retire comfortably? To fund your children's education? To achieve financial independence? Or are you falling behind without realizing it?

The answer depends on your goals, your timeline, and your current financial situation. While there are general guidelines, the real question isn't whether you're saving "enough" in some abstract sense. It's whether you're saving enough to reach your specific goals. Here's how to figure out where you stand.

General Savings Benchmarks

Financial planners often use rules of thumb to provide rough guidance:

The 50/30/20 Rule

Allocate 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. While simple, this rule doesn't account for high earners who can save more or those with specific goals requiring higher savings rates.

Age-Based Retirement Savings Targets

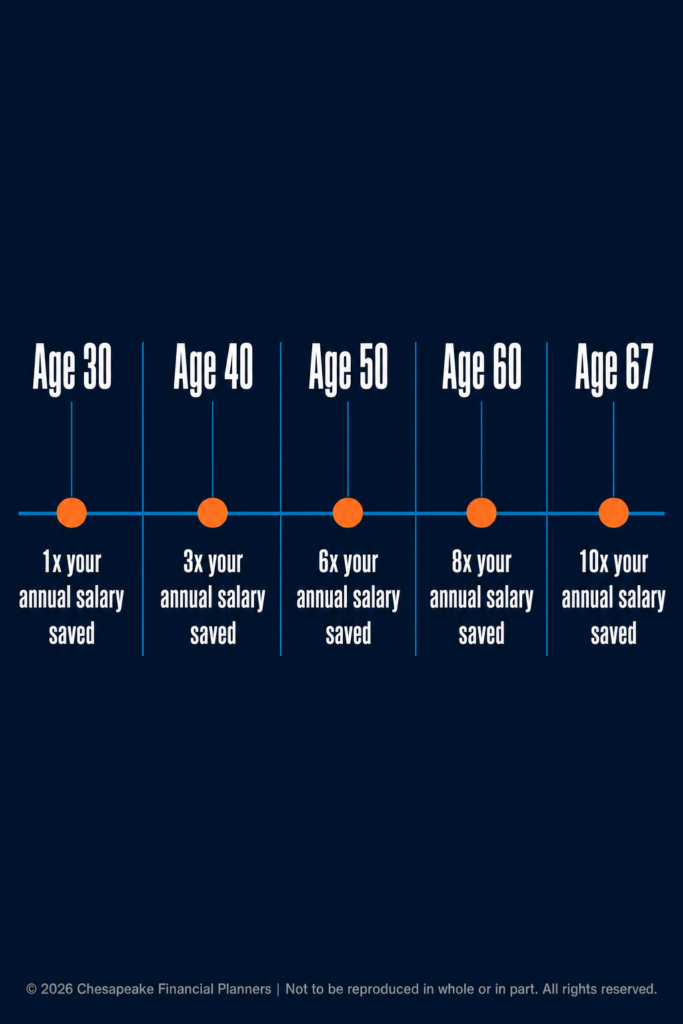

Fidelity suggests the following multiples of annual salary saved by specific ages:

- Age 30: 1x annual salary

- Age 40: 3x annual salary

- Age 50: 6x annual salary

- Age 60: 8x annual salary

- Age 67: 10x annual salary

For example, if you're 40 and earning $150,000, you should have approximately $450,000 saved for retirement. These targets assume you'll replace about 45% of pre-retirement income from savings, with Social Security covering the rest.

10-15% Savings Rate

Many advisors recommend saving 10 to 15% of gross income for retirement, starting in your 20s or 30s. If you start later, you'll need to save more to catch up.

Emergency Fund

Before focusing on long-term goals, build an emergency fund of 3 to 6 months' expenses. This prevents you from having to tap retirement accounts or take on debt during unexpected events.

Factors That Change the Calculation

General rules are helpful, but your specific situation matters more:

When You Started Saving

If you started saving in your 20s, 10 to 15% may be sufficient. If you didn't start until your 40s, you may need to save 20 to 30% or more to catch up. Time is the most powerful variable in wealth accumulation.

Desired Retirement Lifestyle

Planning a modest retirement in a low-cost area requires less savings than planning for extensive travel, multiple homes, or supporting adult children. Your savings target should reflect your goals, not generic benchmarks.

Other Income Sources

Do you have a pension? Rental income? A business you plan to sell? Expected inheritance? These sources reduce how much you need to save from earned income.

Employer Match

If your employer matches 401(k) contributions, that's "free money" that accelerates savings. A 6% contribution with a 6% match is effectively a 12% savings rate.

Debt and Expenses

High-interest debt or inflated lifestyle expenses reduce your ability to save. Paying down debt and controlling spending are often as important as increasing savings.

Longevity and Health

If longevity runs in your family or you expect to live into your 90s, you need more savings than someone planning for a shorter retirement. Health conditions may require additional reserves for medical costs.

Social Security and Medicare

Your expected Social Security benefit significantly affects how much you need to save. Higher earners receive larger benefits, but benefits replace a smaller percentage of pre-retirement income.

How to Know If You're On Track

Run a Retirement Projection

The most accurate way to assess whether you're saving enough is to run a detailed retirement projection. This involves:

- Estimating your desired retirement age and lifestyle expenses

- Projecting your Social Security benefits

- Modeling investment growth based on your asset allocation

- Calculating whether your savings will last through retirement

Many financial advisors offer this as part of comprehensive planning. Online tools like Fidelity's Retirement Score or Vanguard's Retirement Nest Egg Calculator provide rough estimates.

Calculate Your Savings Rate

Divide your annual savings (retirement accounts, taxable investments, emergency fund contributions) by your gross income. If the result is below 10%, you're likely undersaving unless you started very early or have other income sources.

Compare to Age-Based Benchmarks

While not perfect, comparing your savings to age-based targets provides a quick sense of whether you're in the ballpark. If you're significantly behind, it's time to reassess.

Stress Test for Different Scenarios

What happens if you retire earlier than planned? If markets underperform? If you face major health expenses? Running scenarios reveals whether your savings can handle variability.

What to Do If You're Behind

Increase Your Savings Rate

The most direct solution is to save more. Even a 2 to 3% increase in savings rate compounds significantly over time. Direct raises and bonuses straight to savings before you adjust your lifestyle.

Maximize Tax-Advantaged Accounts

Prioritize contributions to 401(k)s, IRAs, HSAs, and other tax-advantaged accounts. The tax savings effectively reduce the "cost" of saving.

Delay Retirement

Working even 2 to 3 additional years has a triple benefit: more years to save, more years of investment growth, and fewer years drawing from savings. It's one of the most powerful levers available.

Reduce Expenses

Cutting spending frees up cash for savings and reduces how much you need in retirement. Housing, transportation, and lifestyle inflation are common areas where expenses can be trimmed.

Optimize Investment Strategy

Ensure your portfolio is appropriately allocated for growth, uses low-cost investments, and includes tax-efficient strategies. Small improvements compound over time.

Consider Part-Time Work in Retirement

Even modest part-time income in early retirement can dramatically extend portfolio longevity by reducing withdrawal rates during critical early years.

What to Do If You're Ahead

Increase Lifestyle

If you're confident you're saving more than needed, consider allocating some savings to current quality of life. Money is a tool, not the goal itself.

Pursue Earlier Retirement

Excess savings may allow you to retire years earlier than planned. Run projections to see if early retirement is feasible.

Fund Other Goals

Redirect savings toward other priorities: education funding, charitable giving, travel, business investments, or legacy planning.

Build Margin for Uncertainty

Having more than "enough" provides buffer against market downturns, health events, longevity risk, or changes in Social Security policy.

Business Owners Face Unique Challenges

If you're a business owner, assessing whether you're saving enough is more complex:

- Your business equity may represent the majority of your wealth, creating concentration risk

- Variable income makes consistent savings difficult

- You may not have access to employer 401(k) matches

- Exit planning and business sale proceeds are often key retirement funding sources

Business owners should work with advisors who understand these dynamics and can model scenarios that account for business value, exit timing, and diversification strategies.

The Role of Professional Guidance

Determining whether you're saving enough requires projecting decades into the future, accounting for variables like investment returns, inflation, taxes, and life expectancy. A financial advisor can:

- Run comprehensive retirement projections with various scenarios

- Identify gaps between current trajectory and goals

- Model trade-offs (retire earlier vs. spend more vs. leave legacy)

- Update projections as life changes

- Provide accountability and course correction

Your Next Step

If you're unsure whether you're saving enough, the worst thing you can do is ignore the question. Uncertainty compounds over time, and waiting to address shortfalls makes them harder to fix.

Chesapeake Financial Planners helps business owners and professionals assess whether they're on track to achieve their financial goals. We provide detailed projections, scenario analysis, and clear guidance on what adjustments (if any) are needed.

Contact us to schedule a consultation:

Chesapeake Financial Planners

2402 Scotlon Ct

Forest Hill, MD 21050

(410) 652-7868

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.