You've received a windfall—an inheritance, business sale, legal settlement, or unexpected financial gain. You should feel excited. Instead, you're lying awake at night wondering: What if I mess this up?

That anxiety isn't unfounded. Studies show that a shocking percentage of people who receive windfalls end up in worse financial shape within a few years. Not because they were reckless, but because they didn't have a strategy to protect and deploy their sudden wealth wisely.

The difference between windfalls that transform lives and windfalls that disappear comes down to a handful of critical decisions made in the first few months. Here's how to ensure your windfall doesn't derail your financial future.

Why Windfalls Are So Vulnerable

The external problem: Sudden wealth creates pressure to make complex financial decisions quickly—about taxes, investments, estate planning, and spending—often without experience managing money at this level.

The internal problem: You're simultaneously excited and terrified. Everyone has advice. You don't know who to trust, and you're worried about making irreversible mistakes.

The philosophical problem: This money represents an opportunity to build the life you want. You ought to be able to enjoy it and protect your future—but without the right strategy, you might do neither.

Let's walk through the critical steps to protect your windfall and position yourself for lasting success.

The First 90 Days: Do Not Skip This Step

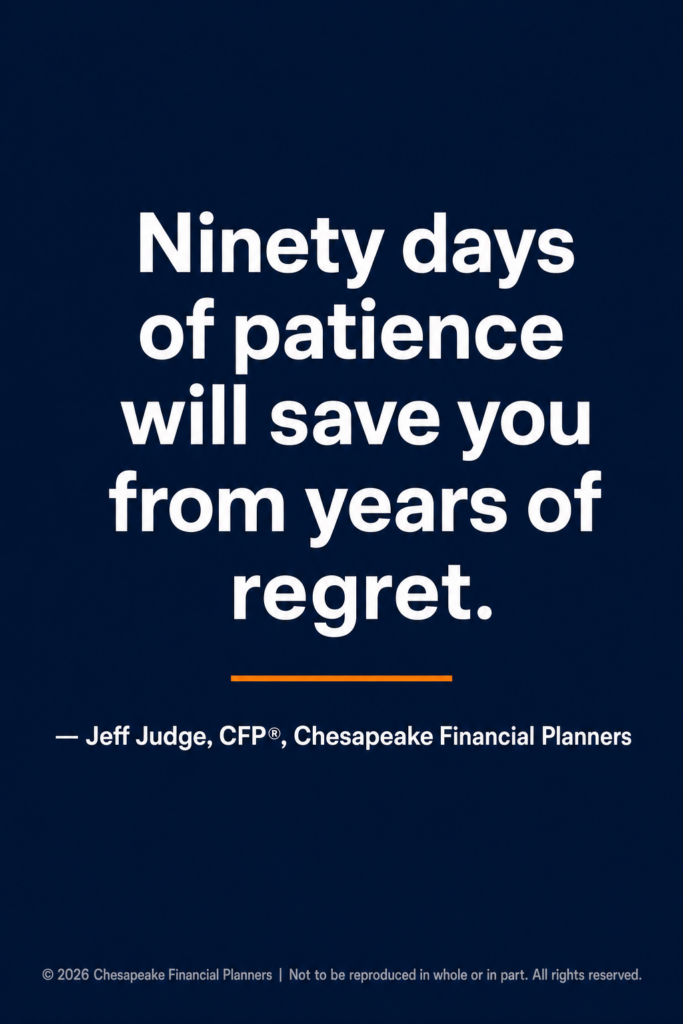

Before you invest, spend, or commit to anything, give yourself 90 days to breathe.

What to do immediately:

1. Park the Money Safely

Put your windfall into a high-yield savings account, money market fund, or short-term Treasury account. Not your checking account where you might accidentally spend it. Not stocks where market volatility adds stress. Somewhere safe and liquid.

This isn't your final strategy—it's a holding pattern while you develop one.

2. Tell No One (Yet)

Word spreads fast about windfalls. Once people know, you'll face:

- Requests for money from family and friends

- Pitches from financial salespeople

- Unsolicited advice from everyone

- Pressure to make decisions before you're ready

Keep it private until you have a plan and boundaries in place.

3. Resist All Pressure to Act

You will face pressure—internal and external—to "do something" with the money. Brokers will call. Family will have opinions. You'll feel like letting money sit is wasting the opportunity.

Ignore all of it. Ninety days of patience will save you from years of regret.

Build Your Protection Strategy

Once you've created space to think, it's time to build a comprehensive strategy. Here's how.

Step 1: Assemble Your Advisory Team

Don't try to navigate this alone. Windfall management requires expertise across multiple domains.

You need:

A fiduciary financial planner: Someone legally obligated to act in your best interest, not sell you products. They coordinate your overall strategy.

A CPA or tax strategist: To minimize taxes on your windfall and structure decisions tax-efficiently. Tax mistakes can cost you 20-40% of your windfall.

An estate planning attorney: To update or create wills, trusts, and documents that protect your wealth and family.

Insurance specialist (if needed): Your insurance needs likely changed with your windfall. Assess life, disability, and umbrella liability coverage.

Interview two or three professionals in each category. Choose people you trust who have experience with windfalls similar to yours.

Step 2: Understand Your Tax Situation

Taxes are often the biggest threat to windfalls. How you handle the first year can save or cost you hundreds of thousands of dollars.

Critical tax questions:

- How is my windfall taxed? (Inheritance, capital gains, ordinary income?)

- Are there strategies to defer or reduce taxes?

- Should I spread income across multiple years?

- Can I offset gains with losses?

- What's my marginal tax rate now, and how will this change it?

- Are there state tax implications if I move?

Don't DIY this. Tax rules for windfalls are complex. A mistake here is costly and sometimes irreversible.

Step 3: Define Your Goals

Before deploying your windfall, get crystal clear on what you want it to accomplish.

Ask yourself:

- What does financial security mean to me?

- Do I want to retire early, change careers, or continue working?

- What lifestyle do I want—and what's sustainable?

- Are there immediate financial priorities (debt, emergency fund, housing)?

- How important is leaving a legacy for my children or charitable causes?

- What am I most worried about?

Write down your answers. These become the framework for every financial decision.

Step 4: Pay Off High-Interest Debt

If you're carrying credit card debt, personal loans, or other high-interest debt (10%+), pay it off immediately.

Why this matters: No investment can reliably outperform high-interest debt. Eliminating it is the highest-return move you can make.

What about mortgages and car loans? It depends. If rates are low (under 5-6%), you may be better off keeping the debt and investing. But if eliminating debt would give you peace of mind and flexibility, that's valid too.

Step 5: Build Your Safety Net

Before investing aggressively, establish a robust foundation:

Emergency fund: Six to twelve months of expenses in a liquid, safe account. This protects you from having to sell investments at the wrong time.

Insurance: Adequate life, disability, and umbrella liability coverage. Your windfall changed your insurance needs—reassess everything.

Estate plan: Updated will, beneficiaries, and estate documents that reflect your new financial situation.

Step 6: Create a Spending Framework

One of the biggest challenges with windfalls: knowing how much you can safely spend without jeopardizing your future.

The sustainable spending rule: Invest your windfall conservatively and spend 3-4% annually. A $500,000 windfall supports $15,000-$20,000 per year in additional spending, not $500,000 of spending.

Set aside "fun money": Allocate 5-10% for guilt-free purchases or meaningful experiences. This satisfies the desire to enjoy your windfall while protecting the rest.

Avoid lifestyle inflation: Upgrading everything at once (bigger house, luxury car, expensive vacations) is how windfalls disappear. Be intentional about what changes and what doesn't.

Step 7: Invest Strategically

Once you've addressed taxes, debt, emergency funds, and spending, it's time to invest the remainder for long-term growth.

Key principles:

Diversify broadly: Don't concentrate wealth in one stock, sector, or asset class. Build a diversified portfolio appropriate to your risk tolerance and timeline.

Match risk to timeline: Money you need in 1-3 years should be in safe, liquid accounts. Money you won't need for 10+ years can be invested more aggressively.

Keep fees low: Avoid high-fee products (certain annuities, actively managed funds, structured products). Choose low-cost index funds or work with a fee-only advisor.

Avoid emotional investing: Don't chase hot stocks or speculative investments. Stick to a disciplined, long-term strategy.

Consider tax-efficient strategies: Tax-loss harvesting, asset location, and strategic withdrawals can save thousands annually.

Step 8: Establish Boundaries with Others

Windfalls change relationships. You'll likely face:

- Requests for money from family and friends

- Pressure to invest in business opportunities

- Unsolicited advice from everyone

How to protect yourself:

Decide in advance what you're willing to do: Set dollar limits on gifts or loans before anyone asks.

Don't lend money you can't afford to lose: Loans to family rarely get repaid.

Use your advisor as a buffer: "I need to check with my financial planner first" is a complete sentence.

Practice saying no: You're allowed to prioritize your own financial security.

Step 9: Monitor and Adjust

Windfall planning isn't a one-time event. Your plan needs to evolve as your life and goals change.

Schedule regular reviews:

- Quarterly check-ins on spending and investments

- Annual comprehensive reviews with your advisory team

- Updates when major life events occur

Adjust as needed:

- Markets change

- Tax laws change

- Your goals change

- Your plan should change too

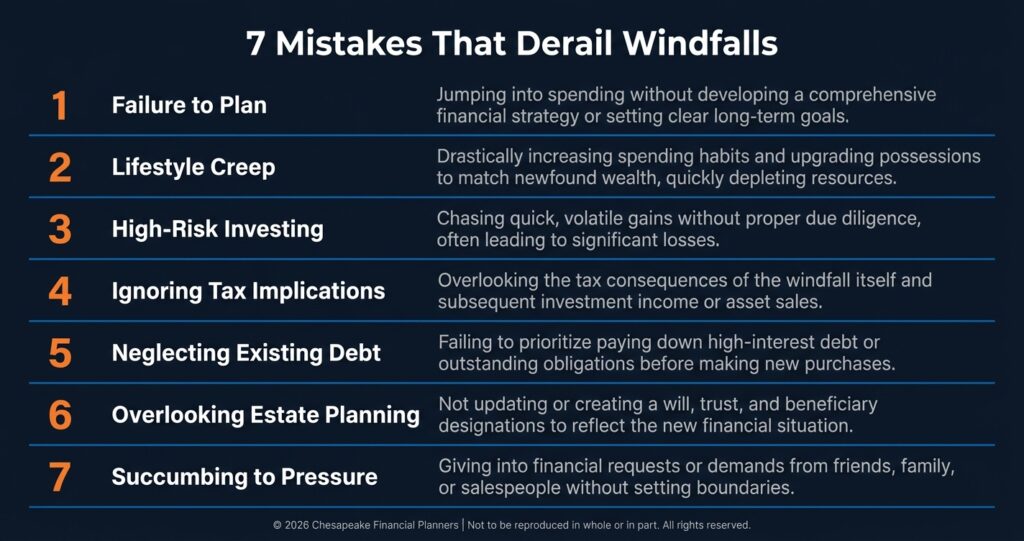

The Mistakes That Derail Windfalls

Avoid these critical errors:

Acting too quickly: Pause, plan, then proceed. Rushing leads to costly mistakes.

Trusting the wrong people: Work only with fiduciary advisors. Verify credentials and check disciplinary history.

Ignoring taxes: Tax mistakes can cost 20-40% of your windfall. Consult a CPA before major decisions.

Failing to diversify: Concentration in one stock or asset is dangerous, no matter how strong it seems.

Lifestyle inflation: Upgrading everything at once is how windfalls disappear within a few years.

Skipping estate planning: Update your will, beneficiaries, and documents to reflect your new wealth.

Trying to do it alone: Professional guidance during windfalls pays for itself many times over.

Your Next Step

If you've received a windfall:

- Park it safely for 90 days while you develop a strategy

- Assemble your advisory team (financial planner, CPA, attorney)

- Define your goals clearly before making major decisions

- Address taxes, debt, and safety nets before aggressive investing

- Create a spending framework that balances enjoyment with protection

- Invest strategically for long-term growth

A windfall is both an opportunity and a responsibility. With the right strategy, you can build lasting financial security and the life you've always wanted.

Received a windfall and need expert guidance? Schedule a complimentary consultation. We'll help you develop a comprehensive strategy that protects your wealth, minimizes taxes, and positions you for long-term success.

This material is for informational purposes only and should not be construed as tax or legal advice. Please consult with a qualified professional regarding your individual situation.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.