When you own a business, figuring out how to pay yourself isn't just a personal finance question—it's a strategic decision that affects your taxes, cash flow, and long-term financial security.

Whether you've just sold your company and are transitioning to a new venture, or you're navigating a career change that includes business ownership, understanding owner compensation strategies is essential. The wrong approach can cost you thousands in unnecessary taxes or create cash flow problems that undermine your business's stability.

The Compensation Challenge Most Owners Face

You've worked hard to build something valuable. But when it comes time to pay yourself, the questions pile up: Should you take a salary? Distributions? A combination of both? How much is reasonable? What will the IRS accept?

The answer depends heavily on your business structure. Choose the wrong method, and you could face IRS scrutiny, overpay on taxes, or leave yourself financially vulnerable during lean periods.

How Your Business Structure Determines Your Pay

Sole Proprietorships and Single-Member LLCs

If you operate as a sole proprietor or single-member LLC (taxed as a sole proprietorship), you can't technically pay yourself a salary. Instead, you take owner's draws—withdrawals from your business equity account.[1]

Owner's draws offer flexibility. You can take funds as needed based on business performance and personal requirements. However, you'll pay self-employment taxes on your entire net business income, regardless of how much you actually withdraw.

Partnerships and Multi-Member LLCs

Partners typically receive guaranteed payments for services rendered, plus a share of profits through distributions. Guaranteed payments are subject to self-employment tax, while profit distributions generally are not.

This creates an opportunity: Structure your compensation to balance regular income needs against tax efficiency, while ensuring the partnership agreement clearly defines how profits are allocated.

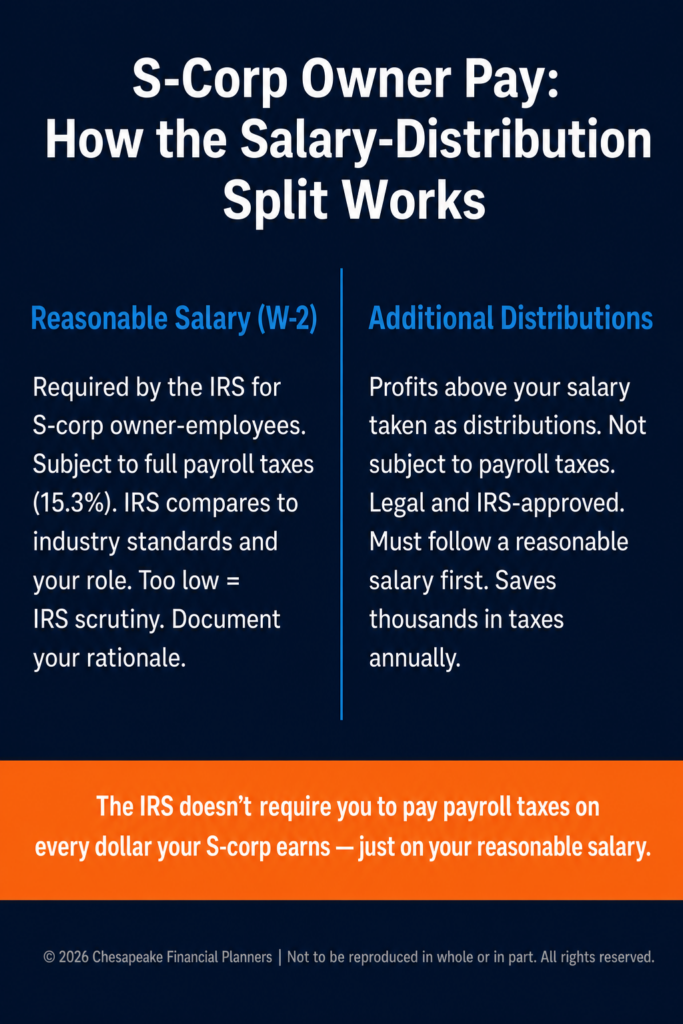

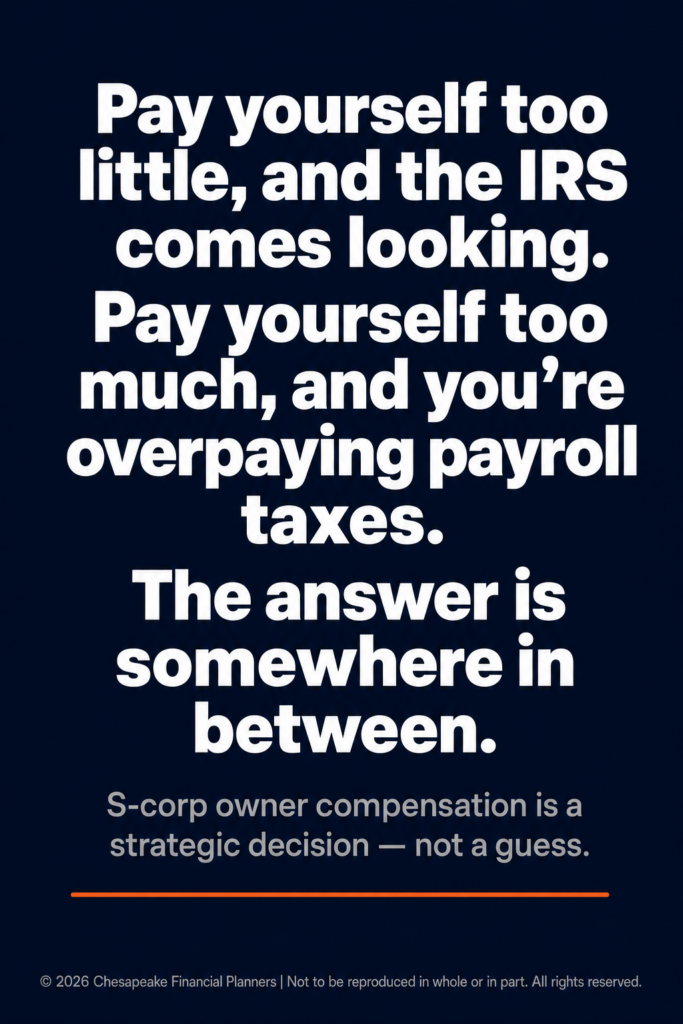

S Corporations: The Balancing Act

S corporation owners face the most complex—and potentially most tax-advantageous—compensation structure. The IRS requires S corp owner-employees to take a "reasonable salary" subject to payroll taxes, while additional profits can be taken as distributions that avoid the 15.3% self-employment tax.[2]

The challenge? "Reasonable compensation" isn't precisely defined. The IRS looks at factors including:

- Industry standards for similar roles

- Your qualifications and responsibilities

- Time devoted to the business

- Company profitability and cash flow

- Compensation paid to non-shareholder employees in comparable positions

Taking too low a salary to minimize payroll taxes invites IRS scrutiny. Taking too high a salary means paying unnecessary payroll taxes on amounts that could have been distributed.

C Corporations: Straightforward But Tax-Heavy

C corporation owners typically take a salary as W-2 employees. Distributions come as dividends, which face double taxation—once at the corporate level and again on your personal return.

This structure makes sense primarily for businesses planning to reinvest most profits or those positioning for acquisition.

Strategic Approaches to Owner Compensation

The Income-First Method

Determine your personal financial needs first, then structure business compensation to meet them. This approach prioritizes financial stability and ensures you can maintain your lifestyle during business transitions.

Start by calculating your minimum monthly expenses, desired savings rate, and discretionary spending. Add a buffer for irregular expenses. This becomes your target compensation floor.

The Industry Benchmark Approach

Research typical salaries for your role and industry using resources like the Bureau of Labor Statistics, industry associations, or executive compensation studies. Position your salary within the reasonable range for your experience level and responsibilities.

This method provides IRS-defensible compensation levels while ensuring you're not overpaying or underpaying yourself relative to market standards.

The Profit-Sharing Formula

Some owners establish a predetermined formula: pay yourself a base salary that meets IRS reasonable compensation standards, then distribute a percentage of quarterly or annual profits.

For example, you might take a $120,000 salary plus 50% of net profits exceeding $200,000. This balances tax efficiency with business cash flow needs and provides upside when the company performs well.

The Lifecycle-Adjusted Strategy

Your compensation strategy should evolve as your business matures:

- Startup phase: Take minimal salary, reinvest heavily in growth. Consider owner's loans you can repay later.

- Growth phase: Increase salary toward market rates as cash flow stabilizes. Begin taking modest distributions.

- Mature phase: Optimize the salary-distribution split for tax efficiency while ensuring adequate retained earnings for opportunities and cushion.

- Exit preparation: Normalize compensation to market rates 2-3 years before sale to present clean financials to potential buyers.

Common Compensation Mistakes to Avoid

- Inconsistent payments: Irregular compensation makes personal financial planning difficult and can raise red flags for lenders or the IRS. Establish regular payment schedules.

- Ignoring cash flow: Ambitious compensation plans that strain business cash flow create stress and may force you to reduce payments when you need them most. Build buffer reserves first.

- Neglecting retirement contributions: Business owners often overlook retirement planning. Establish a SEP-IRA, Solo 401(k), or defined benefit plan to build long-term security while gaining current tax deductions.

- Failing to document: Maintain clear records of compensation decisions, especially for S corps. Document board meetings, salary surveys reviewed, and rationale for your compensation structure.

- Mixing personal and business expenses: Keep finances separate. Pay yourself properly and use those funds for personal expenses rather than running personal costs through the business.

Special Considerations for Wealth Events

If you're navigating a business transition—whether you've recently sold a company, received a buyout, or are starting a new venture after a career change—your compensation strategy requires extra attention.

- After a business sale: Resist the urge to overpay yourself from a new venture while you're still living on sale proceeds. Structure reasonable compensation that's sustainable regardless of your investment income.

- Buyout situations: If you received a buyout and are starting fresh, consider taking a modest salary initially while you build your new venture, supplementing with investment income as needed.

- Career transitions: Moving from W-2 employment to business ownership often means accepting lower initial compensation. Plan for this transition by building reserves beforehand.

Getting Expert Guidance

Owner compensation involves tax law, business strategy, and personal financial planning. Work with a CPA experienced in your business structure and a financial advisor who understands business owner needs.

They can help you model different compensation scenarios, ensure IRS compliance, optimize your tax situation, and integrate business compensation into your broader financial plan.

Your business should support your life, not complicate it. The right compensation strategy ensures you're paid fairly, protects your company's financial health, and positions you for long-term success—whatever transitions lie ahead.

This article is for educational purposes only and does not constitute tax, legal, or financial advice. Consult with qualified professionals regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.