You're facing one of retirement's biggest decisions: your employer is offering a pension lump sum payout. Take the single payment now, or receive monthly pension checks for life?

The stakes are high. Choose wrong, and you could outlive your money, leave your spouse financially vulnerable, or pay unnecessary taxes. Choose right, and you gain control, flexibility, and potentially more lifetime income.

But here's what makes this decision so challenging: there's no universally correct answer. The right choice depends on your health, life expectancy, other income sources, investment discipline, and dozens of other personal factors.

Even more complicated? If you do take the lump sum, how you manage that money determines whether the decision was brilliant or disastrous. Receiving a six or seven-figure check requires a comprehensive withdrawal strategy that balances income needs, tax efficiency, investment risk, and longevity planning.

Understanding What You're Deciding

A pension lump sum is your employer's offer to pay you the present value of your future pension benefits in one payment. Instead of $4,000 monthly for life, they might offer you $800,000 today.

That lump sum calculation is based on actuarial assumptions about how long you'll live and interest rates used to discount future payments to present value. When interest rates are high, lump sums are lower (because future payments are discounted more heavily). When rates are low, lump sums are higher.

This is why lump sum offers can vary significantly year to year, and why some employers encourage employees to take lump sums when rates are favorable to the company.

The Core Withdrawal Challenge

Let's say you take the lump sum. Now you have $800,000 that needs to last as long as the pension would have potentially 30+ years.

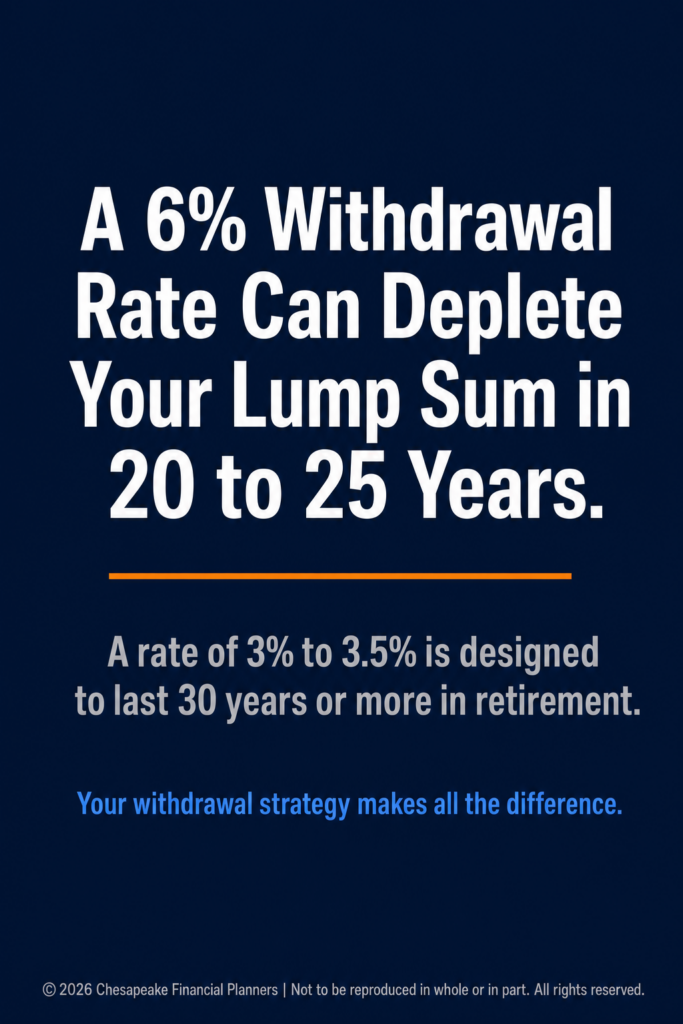

If you simply withdraw $4,000 monthly to replace the pension income, you're pulling $48,000 annually from $800,000 a 6% withdrawal rate. Research suggests this is unsustainably high for most portfolios. You're at significant risk of depleting the account within 20-25 years, especially if you encounter poor market returns early.

This is the fundamental tension: the monthly pension income often represents a higher withdrawal rate than financial planners typically recommend as safe from investment portfolios. The pension can sustain this because it's backed by the company (and potentially PBGC insurance), spreads risk across many participants, and doesn't have to survive market volatility in the same way your personal portfolio does.

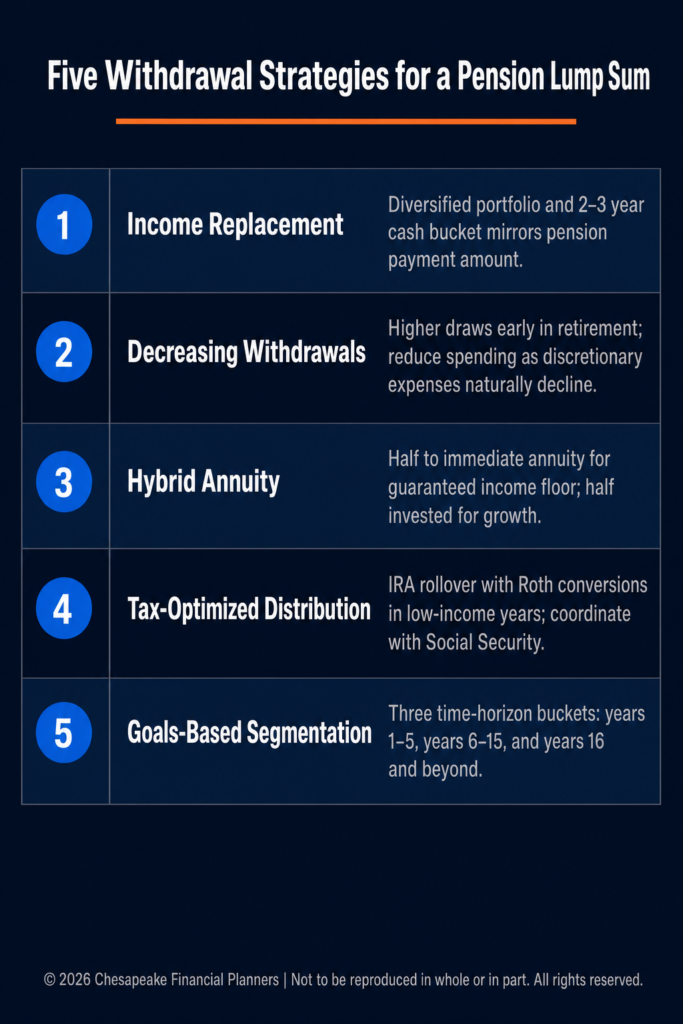

Withdrawal Strategy #1: The Income Replacement Approach

The most straightforward strategy is to invest the lump sum to generate income approximating your pension payment, while preserving principal as long as possible.

How It Works

Invest the lump sum in a diversified portfolio of income-generating investments: dividend-paying stocks, bonds, and potentially annuities. Structure withdrawals to match your pension payment amount.

Use a bucket strategy: keep 2-3 years of withdrawals in cash and short-term bonds, with the remainder invested for growth. This protects against being forced to sell during market downturns.

Pros: Provides the predictable income you would have received from the pension, with the flexibility to adjust if needed.

Cons: Requires discipline not to overspend, and investment returns must be sufficient to sustain withdrawals over your lifetime.

Withdrawal Strategy #2: The Decreasing Withdrawal Approach

This strategy acknowledges that most retirees spend less as they age (except for healthcare), and structures withdrawals accordingly.

How It Works

Start with higher initial withdrawals to fund active early retirement years. Plan to decrease withdrawals over time as travel and discretionary spending naturally decline.

For example, withdraw $60,000 annually for the first 10 years, then reduce to $45,000 for the next 10 years, and $36,000 thereafter. This front-loads spending when you're most likely to enjoy it while reducing draw pressure on the portfolio in later years.

Pros: Aligns spending with typical retirement patterns, potentially making the money last longer while providing more income when you're most active.

Cons: Requires discipline to reduce spending later, and assumes health costs don't offset the decreased discretionary spending.

Withdrawal Strategy #3: The Hybrid Annuity Approach

Use a portion of the lump sum to purchase an immediate annuity, creating a pension-like income floor, and invest the remainder for growth.

How It Works

Take $400,000 of your $800,000 lump sum and purchase an immediate annuity that provides guaranteed lifetime income. Invest the remaining $400,000 for growth and supplemental withdrawals.

The annuity creates a predictable income base covering essential expenses, while the invested portion provides flexibility, growth potential, and legacy value.

Pros: Combines the security of guaranteed income with the flexibility and upside of invested assets. Reduces longevity risk while maintaining some control.

Cons: Annuities have costs, less flexibility, and the income may not keep pace with inflation unless you purchase an inflation-adjusted annuity (which provides lower initial payments).

Withdrawal Strategy #4: The Tax-Optimized Distribution Approach

Structure withdrawals to minimize lifetime taxes by strategically pulling from different account types based on your tax situation each year.

How It Works

Roll the lump sum into an IRA. Then coordinate withdrawals with Social Security claiming decisions, Roth conversions, and other income sources to manage your tax bracket year by year.

In low-income years (before Social Security or RMDs begin), take larger IRA withdrawals and do Roth conversions. In high-income years, minimize withdrawals and draw from Roth or taxable accounts instead.

Pros: Potentially saves tens of thousands in lifetime taxes compared to simply taking the same amount each year.

Cons: Requires sophisticated planning and annual recalibration. Works best with professional guidance.

Withdrawal Strategy #5: The Goals-Based Segmentation Approach

Divide the lump sum into separate pools for different time horizons and purposes.

How It Works

Segment the lump sum into three accounts:

- Short-term (Years 1-5): $200,000 in conservative investments (bonds, CDs) to fund immediate needs without market risk.

- Medium-term (Years 6-15): $300,000 in balanced investments providing moderate growth and income.

- Long-term (Years 16+): $300,000 in growth-oriented investments, primarily stocks.

Each segment has its own withdrawal strategy matched to its time horizon and risk profile.

Pros: Reduces sequence of returns risk by matching asset allocation to time horizons. Provides clarity about which money is for which purpose.

Cons: Requires regular rebalancing and movement of funds between segments. May sacrifice some returns in short-term buckets.

Critical Factors in Your Withdrawal Strategy

Longevity Risk

If you're in excellent health with family history of longevity, you might live 30-40 years in retirement. Your withdrawal strategy must account for this extended timeline. Conservative withdrawal rates (3-3.5%) and strategies that preserve principal become more important.

Inflation Protection

Pensions often don't include cost-of-living adjustments, but inflation still erodes purchasing power. Your withdrawal strategy must either provide inflation protection through investment growth or plan for increasing withdrawals over time.

Some strategies deliberately start with lower withdrawals, leaving more invested to grow and outpace inflation in later years when you need higher nominal amounts to maintain purchasing power.

Spouse Protection

If you're married, how does your withdrawal strategy protect your spouse if you die first? Pension survivor benefits typically provide 50-100% of your pension to your surviving spouse. Your lump sum strategy must ensure your spouse has adequate income even after your death.

This might mean purchasing a joint-life annuity, maintaining sufficient assets to generate income for your spouse, or ensuring adequate life insurance is in place.

Market Risk Management

Unlike a pension that provides the same payment regardless of market conditions, your lump sum is subject to investment risk. Your withdrawal strategy must account for market downturns.

The sequence of returns risk is particularly important early in retirement. Poor market returns in your first 5-10 years can devastate your portfolio if you're simultaneously taking withdrawals. This is why many strategies emphasize cash reserves and conservative positioning early in retirement.

Tax Considerations for Lump Sum Withdrawals

If you roll your lump sum into an IRA, withdrawals are taxed as ordinary income. This creates both challenges and opportunities:

- Challenge: Large withdrawals can push you into high tax brackets.

- Opportunity: You can strategically time withdrawals to manage your tax bracket, unlike a pension that provides the same taxable income regardless of your tax situation that year.

Consider taking larger withdrawals in years when you're in lower brackets (before Social Security begins, or years when you have lower income from other sources). Use Roth conversions during these low-income years to reduce future RMDs.

When the Numbers Favor the Pension

Sometimes the math clearly favors keeping the pension:

- If you're in poor health or have shorter life expectancy

- If the pension includes generous survivor benefits your spouse needs

- If the monthly payment represents more than a 6% withdrawal rate on the lump sum

- If you lack investment discipline or financial planning experience

- If the company offering the pension is financially strong and the pension is well-funded

A guaranteed income stream that continues for life, adjusted for inflation, and provides survivor benefits is difficult to replicate with a lump sum unless the lump sum is particularly generous relative to the monthly benefit.

The Bottom Line

Taking a pension lump sum gives you control and flexibility, but it also transfers risk from your employer to you. Your withdrawal strategy determines whether you successfully manage that risk or succumb to it.

The most successful lump sum strategies combine several elements: diversified investments, disciplined withdrawals that adjust for circumstances, tax optimization, longevity planning, and often some form of guaranteed income to reduce risk.

This isn't a decision to make quickly or alone. Model different scenarios with software or an advisor. Calculate how long your lump sum would last under different withdrawal rates and market conditions. Compare those scenarios to the security of lifetime pension payments.

The right withdrawal strategy for a lump sum is as personalized as the decision to take the lump sum itself. But with careful planning and disciplined execution, a lump sum can provide the income you need while offering flexibility and control you wouldn't have with a traditional pension.

This material is for informational purposes only and should not be construed as investment or retirement advice. Pension lump sum decisions are complex and irreversible. You should consult with a qualified financial advisor regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.