You just went through a major life event marriage, divorce, a new job, an inheritance, the sale of a business, a health crisis. Your life changed. And now you're wondering: Should my investments change too?

The answer isn't automatic. Sometimes yes, sometimes no. And getting it wrong can cost you.

Here's how to think through whether (and how) to adjust your investment strategy after a major life change.

When Life Events Should Trigger Investment Changes

Not every life event requires an investment overhaul. But certain changes fundamentally alter your financial picture in ways that demand a portfolio review.

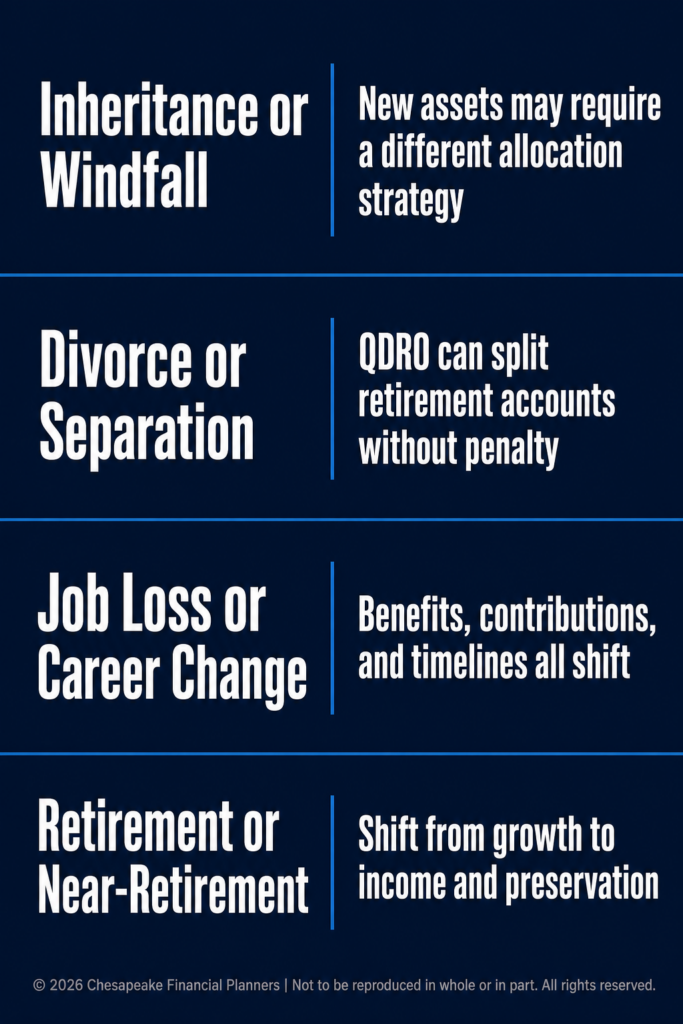

- You received a windfall (inheritance, business sale, stock options). Your asset base just increased significantly. You need to integrate the new assets, rebalance your portfolio, and potentially adjust your risk level.

- Your income changed dramatically (job loss, promotion, retirement). Your cash flow affects how much risk you can afford to take and how much liquidity you need.

- Your time horizon shifted (approaching retirement, received a terminal diagnosis, had a child). The closer you are to needing your money, the less risk you should typically take.

- Your goals changed (decided to retire early, start a business, relocate). If you're going to need a large sum of money in the next 5 years, keeping it fully invested in stocks is probably too risky.

- Your risk tolerance changed (market crash rattled you, gained confidence after weathering volatility). If your actual behavior during market downturns doesn't match your stated risk tolerance, your portfolio should reflect reality, not theory.

- Your family situation changed (marriage, divorce, birth, death). These affect your financial responsibilities, insurance needs, and estate planning all of which connect to your investment strategy.

When NOT to Change Your Investments

Just as important as knowing when to adjust is knowing when to stay the course.

- Short-term market movements. The market dropped 10%? That's not a life event. That's normal volatility. Don't let market swings drive emotional changes to your portfolio.

- Minor income adjustments. Got a 5% raise? That's great, but it probably doesn't warrant a complete portfolio overhaul.

- Temporary situations. If you're between jobs for three months, you don't need to restructure your long-term investments. Tap your emergency fund and stay the course.

- Emotional reactions without financial change. Feeling anxious about the economy or the election? Understandable. But unless your actual financial circumstances changed, your investment strategy shouldn't either.

The Right Way to Review Your Investments

If you've determined that a review is warranted, here's how to approach it:

Step 1: Reassess Your Goals and Timeline

What are you investing for? Retirement? A house? Education? Something else? Has that changed?

When do you need the money? If your timeline shortened (you're retiring in 5 years instead of 20), your portfolio should become more conservative. If it lengthened (you're 40 and just inherited money you won't need until retirement), you can potentially take more risk.

How much do you need? If your windfall means you've already achieved your financial goals, you may not need to take as much risk anymore.

Step 2: Evaluate Your Current Asset Allocation

Are you still in balance? Major life events often throw your asset allocation off. If you inherited a large stock position, you might be over-weighted in equities. If you sold a business and have $2 million in cash, you're under-invested.

Does your current mix match your goals and timeline? A 30-year-old with a stable job saving for retirement should have a very different portfolio than a 65-year-old planning to retire next year even if they have the same net worth.

Step 3: Consider Your Risk Capacity vs. Risk Tolerance

Risk capacity: How much risk can you afford to take based on your financial situation? If you're 60 and need your portfolio to fund retirement starting next year, your risk capacity is low, even if you're emotionally comfortable with volatility.

Risk tolerance: How much risk can you handle emotionally? If market drops cause you to lose sleep and sell at the bottom, your risk tolerance is lower than you think.

The two must align. The right portfolio balances both. A major life event may have changed one or both.

Step 4: Integrate New Assets Thoughtfully

If your life event brought new assets (inheritance, business sale proceeds, stock options), don't just leave them sitting in cash or in their current form.

Inherited investments: Review them. Do they fit your overall strategy? The step-up in basis means you can sell with minimal tax impact. Don't keep something just because you inherited it.

Concentrated stock positions: If you received a windfall in a single stock (company stock, inheritance), diversify to reduce risk. Concentration creates volatility and unnecessary exposure.

Cash from a business sale: Don't let it sit idle. But also don't rush to invest it all at once. Dollar-cost average over 6-12 months if that helps you sleep better.

Step 5: Adjust Risk Appropriately

Reducing risk: If your timeline shortened, your income dropped, or your risk tolerance decreased, move toward a more conservative allocation. This typically means more bonds, cash, or stable value funds, and less in stocks.

Increasing risk: If you're young, have a long timeline, and just received a windfall that provides a safety net, you might actually be able to take more risk than before. But only if it aligns with your goals and temperament.

Don't overreact. Small adjustments (shifting from 80% stocks to 70% stocks) are usually sufficient. Complete overhauls are rarely necessary.

Step 6: Tax Implications

Every investment decision has tax consequences. Don't make changes in a vacuum.

Selling taxable investments triggers capital gains. If you're rebalancing, sell strategically. Harvest losses to offset gains. Consider which accounts to sell from (taxable vs. tax-deferred).

Inherited accounts have special rules. Traditional IRAs inherited by non-spouses must be withdrawn over 10 years. Roth IRAs can grow tax-free for 10 years. Factor this into your strategy.

Location matters. Place tax-inefficient investments (bonds, REITs, actively managed funds) in tax-deferred accounts. Place tax-efficient investments (index funds, growth stocks) in taxable accounts.

Common Mistakes to Avoid

- Abandoning your plan during volatility. If the market drops after your life event, don't panic and sell everything. Volatility is normal. Stick to your updated strategy.

- Chasing performance. Don't pile into last year's hot sector or fund. Diversification works better than trying to time the market.

- Over-concentrating in one investment. Whether it's your company stock, a single rental property, or cryptocurrency, too much in one place is risky.

- Ignoring fees. High-fee investments (actively managed funds, variable annuities, hedge funds) can erode returns over time. Favor low-cost index funds unless there's a compelling reason not to.

- Trying to DIY a complex situation. If your life event involved substantial wealth, work with a financial advisor. The cost of mistakes far exceeds the cost of professional guidance.

The Bottom Line

Major life events don't automatically require investment changes, but they do require a review. Some events fundamentally alter your goals, timeline, or risk profile in ways that demand portfolio adjustments. Others don't.

The key is knowing the difference and making changes based on strategy, not emotion.

We help clients navigate exactly these situations, reviewing their portfolios after major life events and making adjustments that align with their new reality while keeping them on track for long-term independence.

This material is for educational purposes only and should not be considered investment advice. All investments involve risk, including loss of principal. Asset allocation and diversification do not guarantee profit or protect against loss. Consult with a qualified financial advisor before making investment decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.