Retirement should be about enjoying the life you've worked so hard to build—not watching a large chunk of your savings disappear to taxes.

Yet many retirees are surprised by how much they owe in taxes on their retirement withdrawals. Between federal and state income taxes, taxes on Social Security benefits, and Medicare premium surcharges, your effective tax rate can be much higher than you expect.

The good news? With strategic planning, you can significantly reduce the taxes you pay on your retirement income.

At Chesapeake Financial Planners, we help retirees create tax-efficient withdrawal strategies that keep more money in your pocket—where it belongs.

Why retirement taxes catch people off guard

During your working years, taxes are relatively straightforward: your employer withholds taxes from your paycheck, and you file once a year. But in retirement, you're in control of how much income you generate—and that control comes with complexity.

Here's what trips up many retirees:

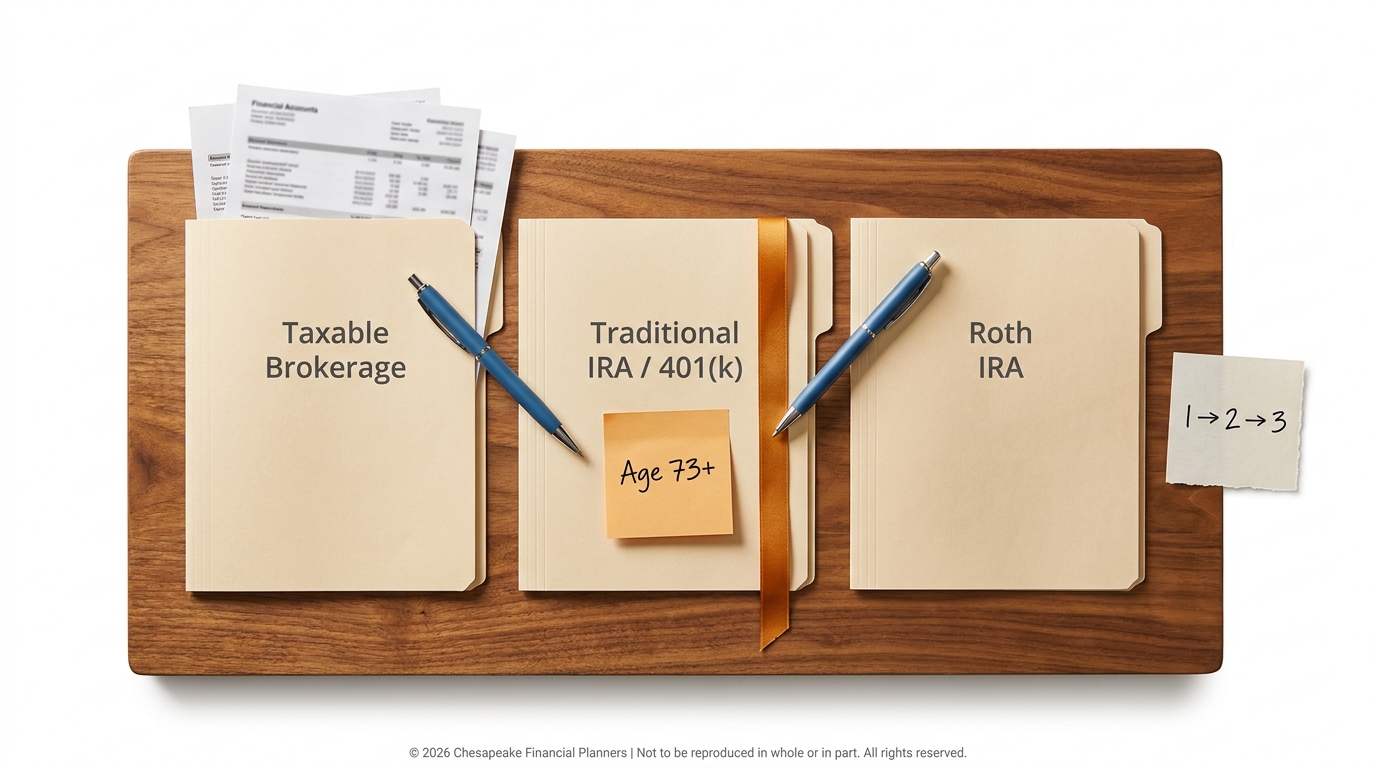

- Different accounts are taxed differently (traditional IRAs, Roth IRAs, taxable accounts, pensions, Social Security)

- Large withdrawals can push you into higher tax brackets

- Social Security benefits become taxable once your income crosses certain thresholds

- Medicare premiums increase if your income is too high (IRMAA surcharges)

- Required Minimum Distributions (RMDs) force withdrawals from traditional retirement accounts starting at age 73, whether you need the money or not

Without a plan, you could end up paying significantly more in taxes than necessary.

Tax-efficient withdrawal strategies

1. Understand the tax treatment of your accounts

Not all retirement accounts are created equal when it comes to taxes:

- Traditional IRAs and 401(k)s: Taxed as ordinary income when withdrawn

- Roth IRAs: Tax-free withdrawals (if you've met the 5-year rule and are over 59½)

- Taxable brokerage accounts: Taxed at capital gains rates, which are typically lower than ordinary income rates

- Social Security: Up to 85% can be taxable depending on your total income

- Pensions: Taxed as ordinary income

Understanding which accounts to tap first—and when—is the foundation of tax-efficient retirement income planning.

2. Consider the "tax bracket management" strategy

Instead of withdrawing a fixed amount every year, consider your marginal tax bracket and aim to "fill up" lower brackets without spilling into higher ones.

For example, if you're married filing jointly, the 12% tax bracket extends to about $100,800 of taxable income in 2026. If your taxable income (after deductions) is $70,000, you have roughly $30,800 of "room" left in the 12% bracket before the 22% bracket begins.

By strategically withdrawing just enough to stay in that bracket, you avoid paying higher marginal rates on every additional dollar.

3. Use Roth conversions strategically

A Roth conversion involves moving money from a traditional IRA to a Roth IRA. You'll pay taxes on the converted amount in the year of the conversion, but future growth and withdrawals are tax-free.

Why this matters in retirement:

- If you retire before age 73 (when RMDs begin), you may have lower-income years to convert at lower tax rates

- Roth IRAs aren't subject to RMDs, giving you more flexibility later

- Roth withdrawals don't count toward the income thresholds that trigger Social Security taxation or IRMAA surcharges

We help clients model Roth conversions to determine the optimal amount to convert each year—balancing current taxes with long-term tax savings.

4. Manage Social Security taxation

Many retirees don't realize that Social Security benefits can be taxable. Whether your benefits are taxed depends on your combined income, which includes:

- Your adjusted gross income (AGI)

- Nontaxable interest

- Half of your Social Security benefits

If your combined income exceeds $32,000 (married) or $25,000 (single), up to 85% of your Social Security benefits may be taxable.

Strategies to reduce Social Security taxes:

- Delay claiming Social Security until after you've done Roth conversions in low-income years

- Withdraw from Roth accounts (tax-free) instead of traditional IRAs to keep combined income lower

- Use Qualified Charitable Distributions (QCDs) to satisfy RMDs without increasing taxable income

5. Leverage Qualified Charitable Distributions (QCDs)

If you're 70½ or older, you can donate up to $108,000 per year (in 2026) directly from your IRA to a qualified charity through a Qualified Charitable Distribution (QCD).

Why QCDs are powerful:

- The distribution counts toward your RMD but doesn't increase your taxable income

- You don't need to itemize deductions to benefit

- Lower taxable income means lower taxes on Social Security and potentially lower Medicare premiums

If you're charitably inclined, QCDs can be one of the most tax-efficient strategies available.

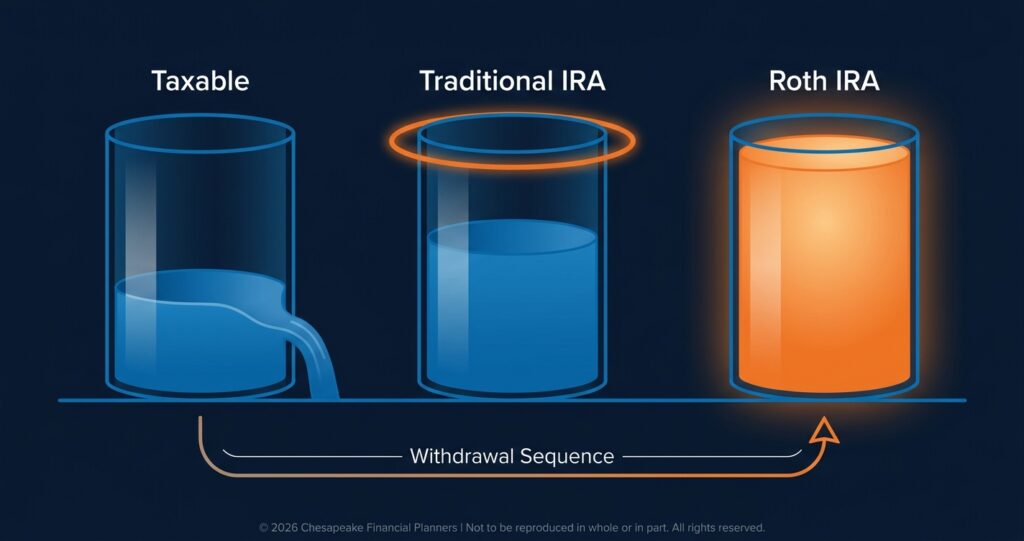

6. Optimize your withdrawal sequence

The order in which you withdraw from your accounts can have a significant impact on your lifetime tax bill. A common withdrawal sequence is:

Phase 1 (Early retirement, before RMDs):

- Withdraw from taxable accounts first (lower capital gains rates)

- Consider Roth conversions to fill up lower tax brackets

- Delay Social Security to maximize benefits

Phase 2 (Age 73+, after RMDs begin):

- Take RMDs from traditional IRAs and 401(k)s as required

- Supplement with Roth withdrawals (tax-free) to avoid pushing into higher brackets

- Use taxable accounts for additional needs

Phase 3 (Later retirement):

- Preserve Roth accounts as long as possible for tax-free growth

- Use QCDs for charitable giving if applicable

Every situation is unique, so we customize withdrawal strategies based on your income needs, account balances, and tax situation.

7. Be strategic about capital gains

Investments in taxable brokerage accounts are taxed at capital gains rates, which are more favorable than ordinary income tax rates.

Long-term capital gains tax rates (2026):

- 0% for income up to $98,900 (married) or $49,450 (single)

- 15% for income up to $613,700 (married) or $533,400 (single)

- 20% for income above those thresholds

Strategies to minimize capital gains taxes:

- Harvest losses to offset gains (tax-loss harvesting)

- Time capital gains to stay in lower brackets

- Hold investments long-term to qualify for preferential rates

- Consider donating appreciated securities to charity (avoid capital gains entirely)

8. Avoid IRMAA surcharges on Medicare premiums

If your income exceeds certain thresholds, you'll pay higher premiums for Medicare Part B and Part D through IRMAA (Income-Related Monthly Adjustment Amount).

IRMAA is based on your income from two years prior, so large withdrawals, Roth conversions, or one-time income spikes can trigger surcharges years later.

Strategies to minimize IRMAA:

- Spread large withdrawals or Roth conversions over multiple years

- Be mindful of income timing if you're near a threshold

- File an appeal (Form SSA-44) if a life-changing event (retirement, divorce, loss of income) justifies a reduction

Planning makes all the difference

Reducing taxes in retirement isn't about avoiding your tax obligations—it's about being intentional with your withdrawals so you're not paying more than necessary.

At Chesapeake Financial Planners, we help retirees:

- Analyze all income sources and account types

- Model different withdrawal scenarios to identify the most tax-efficient strategy

- Coordinate with your CPA to execute the plan

- Revisit the strategy annually to adjust for changes in tax laws, income needs, or life circumstances

Your next step

You've saved diligently for retirement. Now it's time to make sure you're keeping as much of that money as possible.

A tax-efficient withdrawal strategy can save you tens of thousands—or even hundreds of thousands—of dollars over your retirement.

Ready to reduce your retirement tax bill? Schedule a complimentary consultation with Chesapeake Financial Planners today.

This material is for educational purposes only and is not intended as tax advice. Please consult with your tax advisor regarding your specific situation. Tax laws are subject to change, and individual circumstances vary.

Roth IRA conversions are taxable in the year of conversion. Consult with a tax professional to determine if a Roth conversion is appropriate for your situation.

Qualified Charitable Distributions are subject to IRS rules and limitations. Consult with your tax advisor to ensure compliance.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.