If you're charitably inclined and over age 70½, there's a powerful but underutilized strategy that can reduce your tax bill, satisfy required minimum distributions, and support causes you care about, all at the same time. It's called a Qualified Charitable Distribution, or QCD.

Here's why it matters: Once you reach age 73, the IRS requires you to withdraw money from your traditional IRA whether you need it or not. These required minimum distributions (RMDs) are fully taxable and can push you into higher tax brackets, trigger Medicare premium surcharges, and subject more of your Social Security to taxation.

A QCD offers an elegant solution. Donate directly from your IRA to charity, satisfy your RMD, and avoid the tax hit entirely.

What Is a Qualified Charitable Distribution?

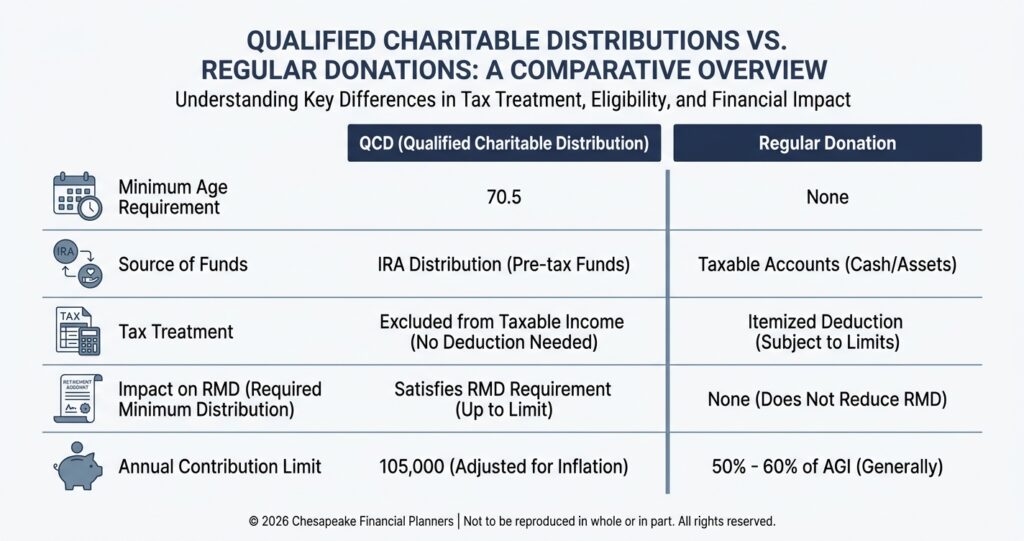

A Qualified Charitable Distribution allows individuals age 70½ or older to donate up to $108,000 per year directly from their IRA to qualified charities. The distribution counts toward your RMD but is excluded from your taxable income.

The key benefit

Unlike taking a distribution and then donating the cash (which requires itemizing deductions to get a tax benefit), a QCD reduces your adjusted gross income (AGI) from the start. This can have cascading benefits throughout your tax return.

Who Can Make a QCD?

Age requirement

You must be 70½ or older at the time of the distribution. This is different from the RMD age, which is now 73. You can start making QCDs before you're required to take RMDs.

Account eligibility

QCDs can only be made from traditional IRAs, including inherited IRAs. You cannot make QCDs from:

- 401(k) plans

- 403(b) plans

- SEP or SIMPLE IRAs (while you're still contributing)

- Roth IRAs (though you can, there's no tax benefit since Roth distributions are already tax-free)

Workaround for employer plans

If you have a 401(k) or 403(b), you can roll funds to a traditional IRA and then make a QCD from the IRA.

QCD Limits and Rules

Annual limit

Up to $108,000 per person per year. If you're married, your spouse can also donate up to $108,000 from their own IRA, for a household total of $216,000.

RMD satisfaction

QCDs count toward your annual RMD. If your RMD is $15,000 and you make a $15,000 QCD, you've satisfied your RMD requirement and owe no taxes on that distribution.

No double benefit

You cannot take a charitable deduction for a QCD. The tax benefit is the exclusion from income, not an itemized deduction.

Qualified charities

The charity must be a 501(c)(3) organization eligible to receive tax-deductible contributions. QCDs cannot go to private foundations, donor-advised funds, or supporting organizations.

Direct transfer requirement

The distribution must go directly from your IRA custodian to the charity. You cannot take the distribution yourself and then donate it. Most IRA custodians can issue checks made payable to the charity, which you can deliver, or they can send the check directly.

The Tax Benefits: Why QCDs Matter

Benefit 1: Lower Adjusted Gross Income

Because QCDs are excluded from your taxable income, they reduce your AGI. This can trigger multiple tax benefits:

Medicare premium savings

High earners pay Income-Related Monthly Adjustment Amounts (IRMAA) on Medicare Part B and Part D premiums. IRMAA thresholds are based on your AGI from two years prior. Lowering your AGI through QCDs can help you avoid or reduce these surcharges, potentially saving $1,000-$3,000+ per year per person.

Social Security taxation reduction

Up to 85% of your Social Security benefits can be taxable based on your combined income (AGI plus half of Social Security benefits). Reducing AGI through QCDs can decrease the taxable portion of your Social Security.

Tax bracket management

Keeping your AGI lower can help you stay in lower tax brackets or avoid phase-outs of other tax benefits.

Benefit 2: Satisfy RMDs Without Increasing Taxable Income

Once RMDs begin at age 73, you must withdraw funds whether you need them or not. For retirees living comfortably on Social Security and pensions, these forced distributions can feel like unwanted taxable income.

The QCD solution

If you were planning to donate to charity anyway, using a QCD means that donation satisfies your RMD without adding to your tax bill. You've essentially converted a taxable distribution into a tax-free charitable gift.

Benefit 3: Tax Benefit Even If You Don't Itemize

With the standard deduction at $32,200 for married couples filing jointly in 2026 ($16,100 for single filers), most retirees no longer itemize deductions. This means traditional charitable donations provide no tax benefit. You're donating with after-tax dollars but getting no deduction.

The QCD advantage

QCDs reduce your income regardless of whether you itemize or take the standard deduction. You get a tax benefit from your charitable giving even without itemizing.

When QCDs Make the Most Sense

Scenario 1: You're charitably inclined and taking RMDs

If you donate to charity regularly and are subject to RMDs, QCDs are almost always advantageous. You're redirecting money you'd have to withdraw anyway to causes you support, while avoiding the tax hit.

Scenario 2: Your income is near Medicare IRMAA thresholds

If you're close to an IRMAA threshold, a QCD can help you stay below it and avoid premium surcharges worth thousands of dollars per year.

Scenario 3: You don't need your RMD for living expenses

If Social Security, pensions, and other income cover your expenses, using QCDs means your RMD directly supports charities rather than becoming unwanted taxable income.

Scenario 4: You're in a high tax bracket

The higher your marginal tax rate, the more valuable the income exclusion. A $10,000 QCD saves $2,200 in taxes if you're in the 22% bracket, or $3,700 if you're in the 37% bracket (when considering federal and state taxes).

How to Execute a QCD

Step 1: Contact your IRA custodian

Let them know you want to make a QCD. Most custodians have specific procedures and forms for QCDs.

Step 2: Provide charity information

You'll need the charity's legal name, address, and Tax ID number. The custodian will need this to issue the check correctly.

Step 3: Delivery options

- Custodian sends directly: The custodian mails the check directly to the charity (safest for documentation purposes)

- Check made payable to charity, mailed to you: You deliver the check to the charity (allows you to present the gift personally)

Step 4: Get a receipt

Obtain a written acknowledgment from the charity. While the tax code doesn't require it for QCDs the same way it does for regular charitable donations, it's prudent documentation.

Step 5: Report on your tax return

Your Form 1099-R from your IRA custodian will show the distribution but won't indicate it was a QCD. You (or your tax preparer) must report it correctly on your tax return as a QCD to exclude it from income.

Timing Considerations

Calendar year planning

QCDs must be completed by December 31 to count for that tax year. Don't wait until late December. Allow time for processing and delivery.

Age 70½ specificity

You become eligible for QCDs the day you turn 70½, not January 1 of that year. If your 70th birthday is June 15, you turn 70½ on December 15 of that year.

Coordinate with RMDs

If you're taking RMDs, make your QCD first or early in the year to ensure it counts toward your RMD for that year.

Common Mistakes to Avoid

Taking the distribution first, then donating

If you receive the distribution personally and then donate, it doesn't qualify as a QCD. The transfer must be direct from the IRA to the charity.

Donating to non-qualified organizations

Donor-advised funds, private foundations, and certain supporting organizations don't qualify. Verify the charity is an eligible 501(c)(3).

Not informing your tax preparer

Your 1099-R won't distinguish a QCD from a regular distribution. Make sure your tax preparer knows to exclude it from income.

Combining with itemized deductions

You can't take a charitable deduction for a QCD. If you claim it as both a QCD and an itemized deduction, the IRS will disallow one or the other.

Maximizing the Strategy

Bunch multiple years

If you typically donate $5,000 per year to a charity, consider making a $10,000 or $15,000 QCD in one year to cover multiple years of giving. This provides a larger tax benefit in one year if you're near IRMAA thresholds or trying to manage income for other tax planning purposes.

Coordinate with Roth conversions

In years when you're doing Roth conversions, use QCDs to satisfy RMDs. This keeps your conversion amounts from being inflated by RMDs you didn't need.

Support multiple charities

You can split your QCD among multiple charities, as long as the total doesn't exceed $108,000.

The Bottom Line

For charitably inclined retirees age 70½ or older, QCDs offer one of the most tax-efficient ways to support causes you care about. The strategy becomes even more valuable once RMDs begin, allowing you to satisfy distribution requirements without increasing your taxable income.

If you regularly donate to charity and are approaching or past age 70½, implementing QCDs can save thousands in taxes while supporting organizations aligned with your values. The key is understanding the rules, coordinating with your IRA custodian, and ensuring your tax return properly reflects the QCD.

This content is for educational purposes only and should not be construed as specific tax or legal advice. Qualified Charitable Distribution rules are complex and subject to IRS regulations. Tax planning decisions should be made in consultation with qualified tax professionals who understand your complete financial situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.