It's one of the biggest—and most permanent—financial decisions you'll ever make: Should you take your pension as a lump sum or as monthly payments for life?

This isn't a decision you can change your mind about later. Once you elect your payout method, you're locked in. The wrong choice can cost you tens or even hundreds of thousands of dollars over your lifetime.

At Chesapeake Financial Planners, we help clients navigate this critical decision by modeling both options and evaluating them against your unique situation, goals, and risk tolerance.

Understanding your pension options

Most pension plans offer two main payout choices:

Option 1: Lump sum

You receive your entire pension benefit as a one-time payment. You can then roll it into an IRA, invest it, and manage it yourself.

Option 2: Annuity (monthly payments)

You receive a monthly payment for the rest of your life. Depending on the option you choose, payments may continue to a surviving spouse.

Some plans offer additional variations:

- Life only: Highest monthly payment, but payments stop when you die

- Joint and survivor (50%, 75%, or 100%): Lower monthly payment, but your spouse continues to receive a portion after you pass

- Period certain: Payments guaranteed for a minimum period (e.g., 10 or 20 years) even if you die early

The lump sum option: Control and flexibility

How it works

Your pension value is calculated and paid out in one large sum. You can roll it into an IRA (avoiding immediate taxes) and manage the investments yourself—or with the help of a financial advisor.

Advantages of the lump sum

1. Full control over your money

You decide how to invest it, how much to withdraw, and when. You're not locked into a fixed payment structure.

2. Flexibility to adjust withdrawals

Need extra money one year for a big expense? You can take more. Don't need income for a few years? You can leave it invested to grow.

3. Protection against inflation

If invested properly, your portfolio can grow over time, helping maintain purchasing power. Monthly pension payments often lack cost-of-living adjustments.

4. Legacy benefits

If you pass away early, your heirs inherit the remaining balance. With monthly payments (especially life-only options), the pension may stop entirely.

5. Opportunity for higher returns

If you invest wisely, you may generate more total income over your lifetime than you would have received from monthly payments.

Disadvantages of the lump sum

1. Investment and longevity risk

You're responsible for making the money last. Poor investment decisions or living longer than expected could result in running out of money.

2. Requires discipline

You must resist the temptation to overspend or make emotional investment decisions during market downturns.

3. Complexity

Managing a large portfolio and creating sustainable income requires expertise—or the cost of hiring professional help.

4. Market timing risk

If you retire just before a market crash, your portfolio could suffer significant losses that may not recover in time.

The monthly payment option: Security and simplicity

How it works

You receive a fixed monthly payment for life (or for both you and your spouse, depending on the option chosen). This income is contractual and can't be outlived.

Advantages of monthly payments

1. Guaranteed income for life

You'll never run out of money, no matter how long you live. This provides peace of mind and addresses longevity risk.

2. Simplicity

No investment decisions, no portfolio management, no worries about market performance. Your check arrives every month like clockwork.

3. Protection against poor decision-making

You can't accidentally withdraw too much or make costly investment mistakes.

4. Removes sequence of returns risk

Market crashes don't directly affect your monthly payment—it stays the same regardless of what happens in the market.

Disadvantages of monthly payments

1. No flexibility

The payment amount is fixed. If you need extra money for an emergency or opportunity, you're out of luck.

2. Inflation erosion

Most pensions don't have cost-of-living adjustments (COLAs). Over 20–30 years, inflation can cut your purchasing power in half.

3. Limited or no inheritance

Depending on the option you choose, little or nothing may be left for your heirs. A life-only option ends when you die.

4. Lower survivor benefits

Choosing a joint-and-survivor option reduces your monthly payment—sometimes by 10–20%—to provide income for your spouse after your death.

5. Loss of control

You have no say in how the pension fund is managed, and you're dependent on the financial health of the pension plan (though most are insured by the PBGC).

Key factors to consider when deciding

1. Your health and longevity

If you're in poor health or have a family history of shorter lifespans, the lump sum may make more sense—you could die before "breaking even" with monthly payments.

If you're healthy with a family history of longevity, monthly payments provide insurance against outliving your money.

2. Your spouse's situation

If you're married, consider your spouse's needs. Will they be financially secure if you pass away first? Joint-and-survivor options provide ongoing income but reduce your initial payment.

3. Other sources of guaranteed income

Do you have Social Security, another pension, or annuities? If so, you may have enough contractual income to cover essentials, making the lump sum a reasonable choice for discretionary spending.

If your pension is your only guaranteed income source, monthly payments may provide critical stability.

4. Your investment knowledge and discipline

Are you comfortable managing a large portfolio? Do you have the discipline to avoid overspending during market downturns?

If not, monthly payments remove the burden (and risk) of self-management.

5. Your need for liquidity

Do you anticipate large expenses—like long-term care, helping adult children, or major home repairs? A lump sum offers access to capital. Monthly payments do not.

6. Interest rates at the time of your decision

Lump sum calculations are based on interest rates. When rates are high, lump sums are smaller. When rates are low, lump sums are larger. This can significantly affect which option is more favorable.

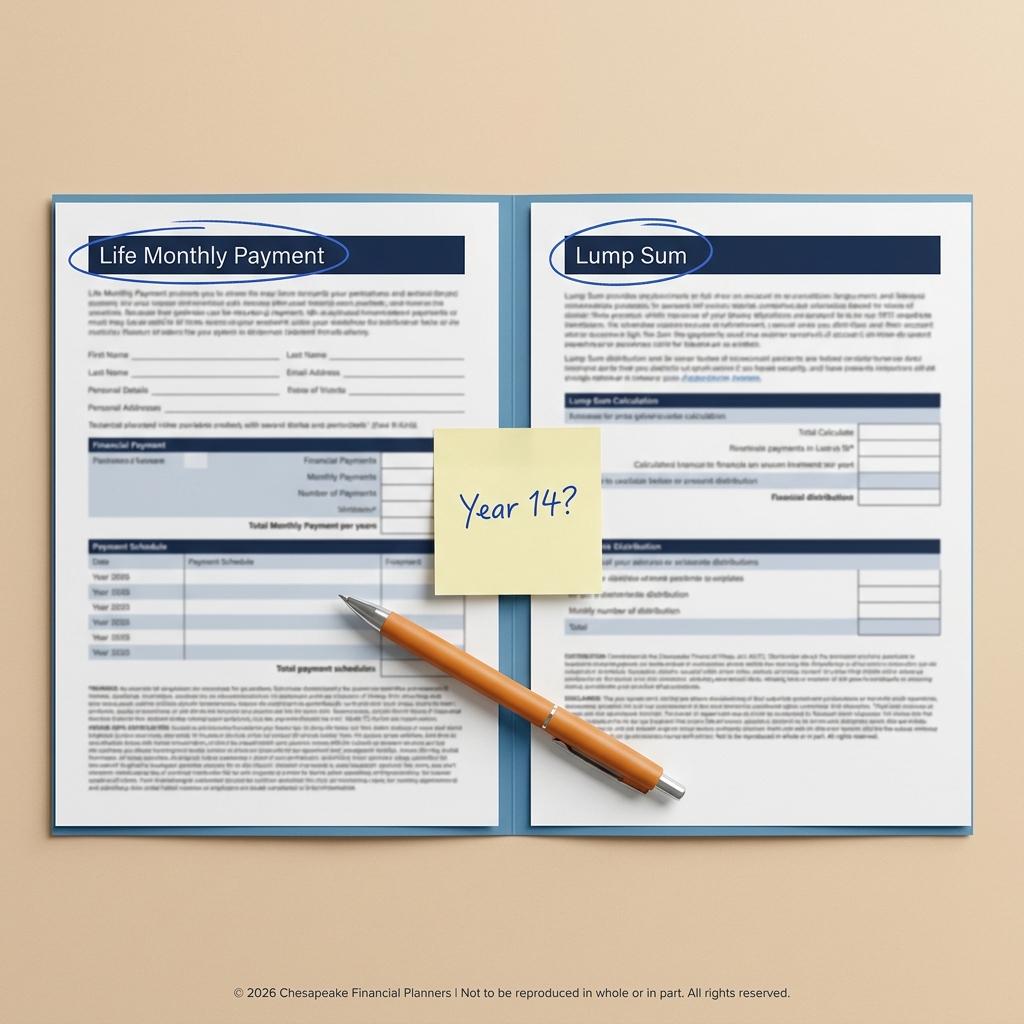

Running the numbers: The breakeven analysis

One way to compare options is to calculate the breakeven point—how long you'd need to live for the monthly payments to exceed the lump sum value.

Example

- Lump sum offer: $500,000

- Monthly payment: $3,000 per month ($36,000 per year)

Simple breakeven calculation

$500,000 ÷ $36,000 = ~13.9 years

If you live longer than 14 years, the monthly payments would pay out more than the lump sum.

But this analysis is incomplete. It doesn't account for:

- Investment growth on the lump sum

- Inflation eroding the monthly payment's value

- Taxes on withdrawals vs. pension income

- Survivor benefits

That's why professional modeling is critical—we run detailed scenarios that factor in all these variables to show you which option makes sense for your situation.

What we recommend at Chesapeake Financial Planners

There's no one-size-fits-all answer, but here are some guidelines:

Lean toward the lump sum if:

- You're in below-average health

- You have strong financial discipline and investment knowledge

- You have other sources of guaranteed income (Social Security, annuities)

- You want to leave a legacy for heirs

- Interest rates favor a higher lump sum payout

Lean toward monthly payments if:

- You're in good health with a long life expectancy

- You prefer simplicity and guaranteed income

- You're concerned about outliving your money

- This is your primary source of retirement income beyond Social Security

- You lack investment experience or discipline

Consider a hybrid approach:

Some retirees take the lump sum and use a portion to purchase an immediate annuity, creating their own "personal pension" while maintaining access to the remaining funds for flexibility.

Your next step

This decision deserves careful analysis, not a gut feeling. The right choice depends on your health, financial situation, other income sources, and personal preferences.

At Chesapeake Financial Planners, we model both options using detailed projections that account for taxes, inflation, investment returns, and longevity. We help you see the long-term impact of each choice—so you can decide with confidence.

Facing a pension decision? Schedule a complimentary consultation with our team today.

This material is for educational purposes only and is not intended as investment or tax advice. Pension elections are irrevocable and should be carefully evaluated with the help of a qualified financial advisor and tax professional.

All investing involves risk, including the potential loss of principal. No investment strategy can guarantee success or protect against loss.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.