You've built a profitable business and it's time to start taking money out for retirement. But how? Should you pay yourself more salary? Take distributions? What about dividends? And why does your accountant keep mentioning something about "reasonable compensation"?

Get this wrong, and you'll either overpay the IRS or trigger an audit. Get it right, and you could save tens of thousands in taxes while building the retirement you've earned.

The Tax Trap That Costs Business Owners a Fortune

Here's what most business owners discover too late: how you take money out of your business has enormous tax implications. Two owners with identical profits can pay vastly different tax bills based solely on the distribution strategy they choose.

The external problem is technical determining the optimal mix of salary, distributions, and other compensation. But the internal frustration runs deeper: the fear of triggering an IRS audit, the anxiety about leaving money on the table, and the confusion about rules that seem designed to be incomprehensible.

Here's what you deserve: a clear strategy to take money out of your business tax-efficiently, legally, and in a way that funds your retirement without attracting IRS scrutiny.

Understanding Your Options (and Their Tax Consequences)

The right answer depends entirely on your business entity structure. Let's break down each:

If You're a Sole Proprietor or Single-Member LLC

Reality: You don't have separate "salary" versus "distribution" options. All net profit flows to your personal tax return and you pay:

- Income tax on the full amount

- Self-employment tax (15.3%) on the full amount

Taking money out: You simply withdraw cash. No tax consequences beyond what you already owe on the profit.

For retirement: Every dollar of profit increases your tax bill. The solution? Use retirement plans (SEP IRA, Solo 401(k)) to reduce taxable income while building retirement savings.

Tax efficiency: Not optimal for high-profit businesses you're paying self-employment tax on everything.

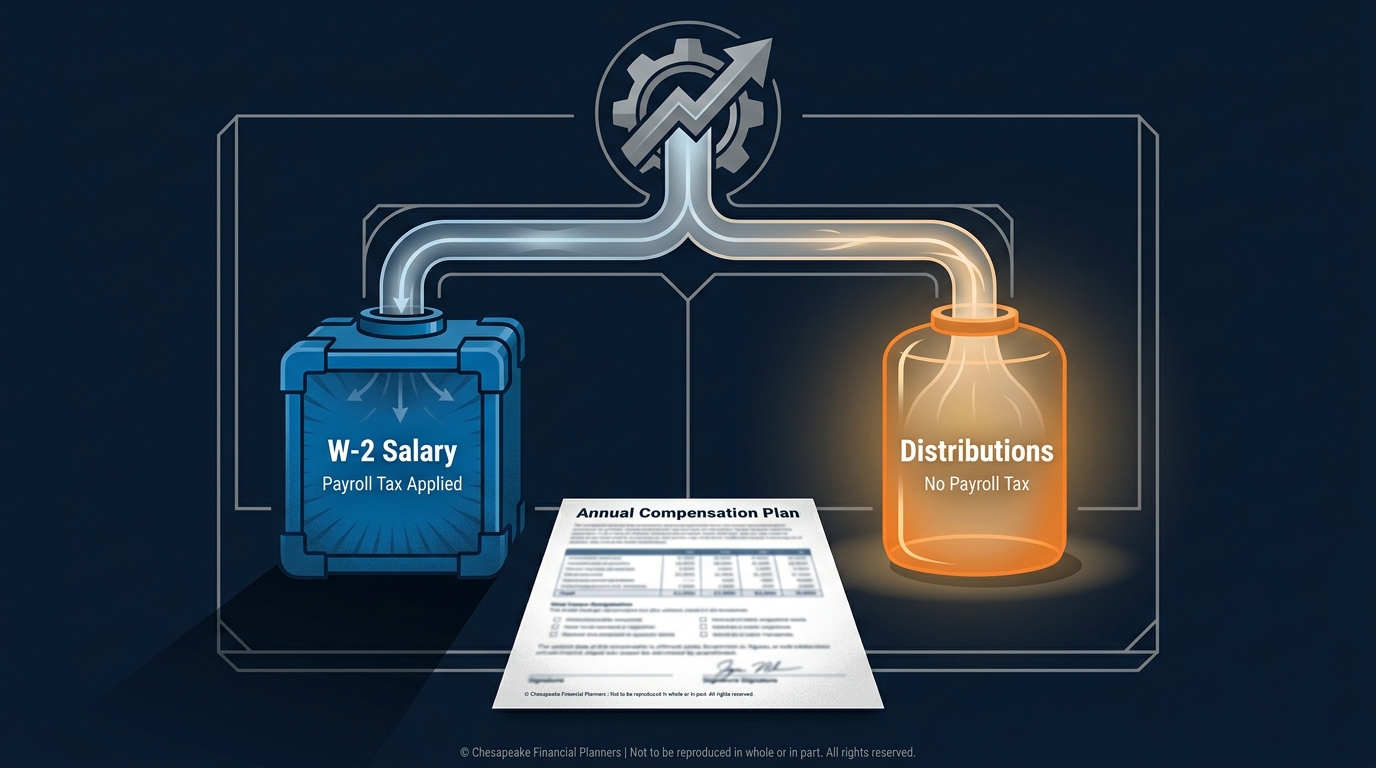

If You're an S Corporation (the Tax-Saving Sweet Spot)

The two buckets:

- W-2 Salary (Wages)

- Distributions

The strategy: Pay yourself a reasonable salary, then take remaining profits as distributions to avoid self-employment tax on the distribution portion.

Example of the tax savings:

- Net profit: $200,000

- Reasonable salary: $120,000 (payroll tax: ~$18,360)

- Distribution: $80,000 (no additional payroll tax)

- Tax saved vs. sole prop: ~$12,240 annually

The IRS Landmine: "Reasonable Compensation"

The IRS requires S corp owners who actively work in the business to pay themselves a reasonable salary BEFORE taking distributions. Pay yourself $40K salary and $160K distributions when comparable jobs pay $120K? Expect IRS attention.

How to determine "reasonable":

- What would you pay someone else to do your job?

- Industry compensation surveys for your role and location

- Your qualifications, responsibilities, and hours worked

- Company profitability and industry norms

Safe harbor approach: Many advisors suggest 40-60% of profits as salary, though no official IRS safe harbor exists. Document your rationale.

If You're a C Corporation

The three options:

- Salary

- Dividends

- Redemption of Stock

For retirement income: C corps are tax-inefficient for regular distributions due to double taxation. Better for:

- Businesses retaining earnings for growth

- Companies planning to go public

- Situations where qualified dividend treatment provides overall lower rates than S corp distributions

The strategy: Maximize deductible salary/benefits while in accumulation years. Consider redemption or liquidation strategies when exiting.

If You're a Partnership or Multi-Member LLC

How it works: Partners receive:

- Guaranteed Payments

- Distributive Share of Profits

For retirement: Partners face similar tax treatment as sole proprietors—self-employment tax on everything. Solutions involve retirement plans and potentially restructuring as an S corp.

Building Your Retirement Income Strategy

Taking money out for retirement is more than just tax optimization. It's about creating sustainable income that:

Meets your retirement lifestyle needs: Calculate actual retirement expenses, not just a percentage of current income.

Provides tax diversification: Don't put all your eggs in one tax basket. Having money in traditional retirement accounts, Roth accounts, taxable accounts, and business equity gives you flexibility.

Preserves business value: Taking out too much too fast can starve the business of capital needed for growth or leave it weak when you try to sell.

Maintains flexibility: Your income needs will change—healthcare costs, travel, helping family. Build in flexibility to adjust distributions.

The Optimal Strategy by Business Stage

Growth phase (building the business):

- Minimize current distributions

- Maximize retirement plan contributions for tax-deferred growth

- Reinvest profits for business value appreciation

Mature phase (business throwing off cash):

- Take reasonable compensation + distributions for lifestyle

- Max out retirement contributions

- Build taxable investment accounts for liquidity

Pre-exit phase (2-5 years from sale):

- Continue retirement plan contributions

- Consider deferred compensation arrangements

- Position business for optimal sale structure

- Build personal liquidity separate from business

Exit phase (winding down or sold):

- Optimize the sale structure for tax efficiency

- Convert business proceeds to diversified retirement portfolio

- Implement systematic withdrawal strategy

Common Mistakes That Cost Business Owners

Paying zero salary in an S corp: Taking all profits as distributions is an IRS red flag and will likely be recharacterized with penalties.

Not documenting reasonable compensation: When the IRS questions your salary, you'll need evidence—industry surveys, job descriptions, board minutes discussing compensation.

Ignoring state payroll taxes: Some states have different rules. California, New York, and others may not follow federal S corp treatment.

Taking irregular distributions: Maintain consistency to show it's not disguised wages. Distributions should generally align with ownership percentages.

Forgetting about basis: S corp distributions exceeding your stock basis create capital gains. Track your basis carefully.

Mixing personal and business finances: Clean separation is essential—both for tax purposes and if you ever face IRS scrutiny.

What Financial Clarity Looks Like

Imagine taking $150,000 annually from your business for retirement, knowing you're structured optimally for taxes, your documentation would withstand an audit, and you're building wealth both inside and outside the business.

You sleep well knowing you're not overpaying taxes or taking unnecessary risks. You have confidence in your retirement timeline because you've built systematic income streams.

That's the power of strategic distribution planning.

Your Three-Step Path to Tax-Efficient Retirement Income

Here's how we help business owners structure income for retirement:

- Schedule a complimentary consultation to review your current business structure and compensation strategy

- We'll model different scenarios showing tax implications of salary vs. distributions, retirement plan contributions, and withdrawal strategies

- Together we'll implement an optimized plan and coordinate with your CPA to ensure proper execution and documentation

You've built the business. Now let's make sure you're taking money out in the most tax-efficient way possible.

Ready to optimize your business distributions for retirement? Schedule your consultation today.

This article is for educational purposes only and does not constitute tax, legal, or investment advice. Reasonable compensation requirements vary by situation and are subject to IRS review. Entity structure and distribution strategies have complex tax implications. State tax treatment may differ from federal. Consult with qualified tax and legal professionals regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.