Ignoring family dynamics. Inheritances often create tension among family members. Set clear boundaries early. You don't owe anyone an explanation or a share of what you inherited.

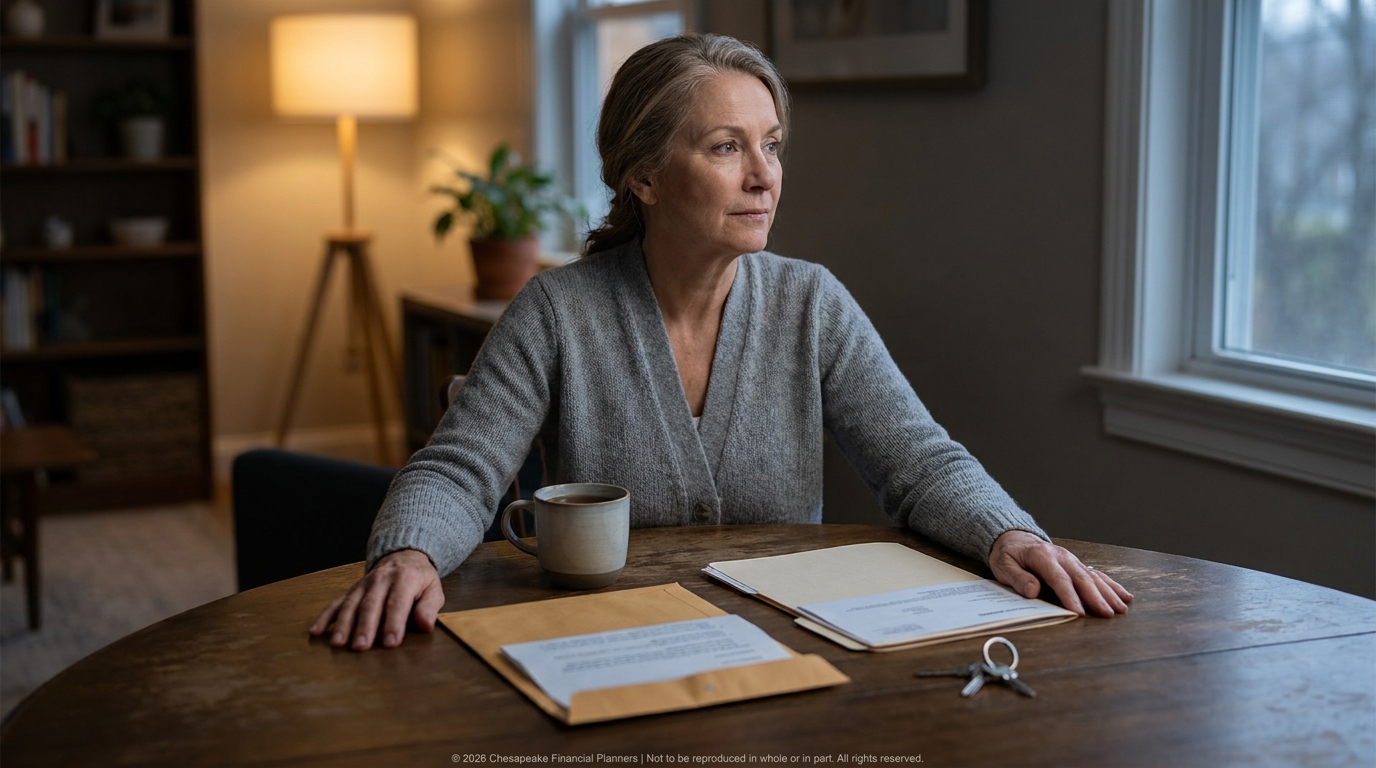

You just received an inheritance. Maybe it's money. Maybe it's property. Maybe it's both.

And now you're facing a mix of emotions, grief, gratitude, overwhelm, and a pressing question: What do I do with this?

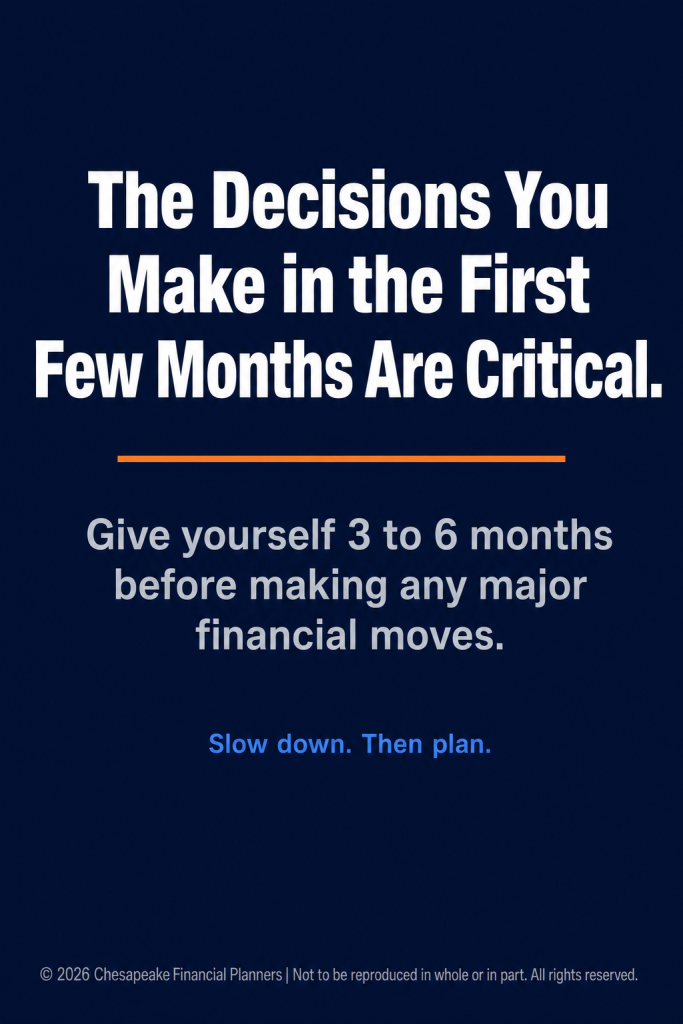

The first few months after receiving an inheritance are critical. The decisions you make now will shape whether this inheritance becomes lasting financial security or a source of regret.

Here's what to do first.

Step 1: Do Nothing (For Now)

The first rule of inheritance: slow down.

You don't need to make any major financial decisions immediately. In fact, you shouldn't.

Why waiting matters: You're likely grieving. You're processing loss. You may be dealing with family dynamics, estate settlement complexities, and emotional exhaustion. This is not the time to make irreversible financial choices.

What to do instead: If the inheritance is cash, park it in a high-yield savings account or money market fund. If it's property or investments, leave them as-is for now. Give yourself 3-6 months to let the dust settle before making significant moves.

This pause protects you from emotional decisions, pressure from family members, and your own impulse to "do something" before you're ready.

Step 2: Understand What You Actually Inherited

Before you can make a plan, you need to know exactly what you received.

- Cash and bank accounts: Simple. You have liquid funds. But understand how they'll be distributed (directly to you, through the estate, through a trust) and any tax implications.

- Retirement accounts (IRAs, 401(k)s): These require special handling. Most non-spouse beneficiaries must withdraw all funds within 10 years under the SECURE Act. Each withdrawal is taxed as ordinary income, so you'll need a strategy to minimize taxes.

- Real estate: Is it the family home? Rental property? Land? What's the current market value? What are the carrying costs (mortgage, taxes, insurance, maintenance)? Is it titled correctly to you?

- Stocks, bonds, brokerage accounts: Check the current value and composition. Understand the "step-up in basis" rule (your cost basis is the value on the date of death, not what the deceased originally paid). This can save you significant capital gains taxes.

- Business interests: If you inherited part or all of a business, you need a professional valuation and a clear understanding of your role (active owner, passive investor, or seller).

- Personal property: Jewelry, art, collectibles, vehicles. These can have emotional and financial value. Get appraisals for valuable items.

- Debts: Debts of the deceased are typically paid from the estate before distribution. But if you inherited property with debt (a mortgaged house, for example), understand your obligations.

Step 3: Handle the Immediate Logistics

Some tasks can't wait, even if major financial decisions can.

- Update titling and beneficiaries. If you inherited accounts or property, work with the executor or attorney to get them properly titled in your name.

- Set aside money for taxes. If you inherited a traditional IRA or other pre-tax account, you'll owe taxes on withdrawals. Set aside 25-30% in a separate account so you're not caught off guard when tax time comes.

- Continue essential payments. If you inherited property, keep paying the mortgage, property taxes, insurance, and utilities. Letting these lapse creates expensive problems.

- Secure valuable items. If you inherited jewelry, art, or other valuables, store them securely and update your homeowners or renters insurance to cover them.

- Don't make any binding commitments. Don't promise money to family members. Don't invest in your friend's business. Don't buy a house. Not yet.

Step 4: Assemble Your Advisory Team

An inheritance, especially a substantial one, requires professional guidance.

- Financial advisor: Someone who can help you integrate the inheritance into your overall financial plan, manage investments, and coordinate with your other advisors. Look for a fee-only fiduciary advisor.

- CPA or tax professional: Essential if you inherited retirement accounts, will be selling property, or if the inheritance significantly increases your income. They'll help you minimize taxes and avoid costly mistakes.

- Estate attorney: If the inheritance involves trusts, business interests, or complex family situations, an attorney ensures everything is handled correctly.

- Insurance agent: Review your life, disability, umbrella liability, and property insurance. An inheritance changes your risk profile and insurance needs.

You don't need to hire everyone immediately. But at minimum, consult with a financial advisor and CPA within the first few months.

Step 5: Address Debt and Build an Emergency Fund

Before you start thinking about investing or spending, handle these two priorities:

- Pay off high-interest debt. Credit cards, payday loans, or other debt with interest rates above 7-8% should be paid off immediately. This is a guaranteed return on your money.

- Build (or strengthen) your emergency fund. Set aside 3-6 months of living expenses in a liquid, safe account. This protects you from needing to tap your inheritance for unexpected costs.

These moves provide financial stability and peace of mind, creating a foundation for everything else.

Step 6: Understand Your Tax Situation

Inheritance tax rules are complex, and mistakes can be expensive.

- Federal estate tax: For most people, this doesn't apply. The estate pays federal estate tax before you inherit (if the estate exceeds $13.61 million). You don't pay federal tax on the inheritance itself.

- State estate or inheritance taxes: Some states tax inheritances. Check the rules for the state where the deceased lived.

- Inherited retirement accounts: Distributions from traditional IRAs and 401(k)s are taxed as ordinary income. Work with a CPA to create a withdrawal strategy that minimizes your lifetime tax bill.

- Capital gains on inherited property: If you sell inherited property, you'll owe capital gains tax on appreciation from the date you inherited it. But thanks to the "step-up in basis," you won't owe tax on appreciation during the deceased's lifetime.

Step 7: Decide What to Keep and What to Sell

Not everything you inherit needs to be kept.

- Sentimental vs. practical. It's okay to keep items with emotional value. But don't keep a house or investment property out of guilt if it doesn't fit your financial plan or lifestyle.

- The family home. This is often the hardest decision. If you inherited the house you grew up in, selling can feel wrong. But if you don't live there, don't want to, and can't afford the upkeep, keeping it may not make sense. Give yourself permission to make the practical choice.

- Concentrated stock positions. If you inherited a large position in a single stock, consider diversifying. The step-up in basis means you can sell immediately with minimal or no capital gains tax. Waiting could expose you to significant risk if the stock declines.

- Underperforming investments. Just because the deceased held certain investments doesn't mean you should keep them. Review everything with your advisor and make changes that align with your goals and risk tolerance.

Common Mistakes to Avoid

- Telling everyone. The more people who know about your inheritance, the more requests you'll get for money. Keep it private.

- Making large purchases immediately. Buying a car, house, or taking an expensive vacation in the first few months is usually an emotional decision, not a strategic one.

- Ignoring family dynamics. Inheritances often create tension among family members. Set clear boundaries early. You don't owe anyone an explanation or a share of what you inherited.

- Trying to recreate the deceased's investment strategy. What worked for them may not work for you. Your age, goals, risk tolerance, and timeline are different.

- Not updating your own estate plan. An inheritance changes your financial picture. Update your will, beneficiaries, and estate plan to reflect your new situation.

The Bottom Line

Receiving an inheritance is a significant financial event. It's also an emotional one. The best thing you can do in the first few weeks and months is to move slowly, seek professional guidance, and give yourself space to make thoughtful decisions.

The inheritance represents someone's life's work. Honoring that means managing it wisely not rushing into decisions you'll regret.

We help clients navigate inheritances from start to finish, providing clarity, strategy, and confidence during a complicated time.

This material is for educational purposes only and should not be considered financial, tax, or legal advice. Inheritance laws and tax treatment vary by state and individual circumstances. Consult with qualified professionals before making decisions regarding inherited assets.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.