You exercised your ISOs in January, feeling smart about starting the long-term capital gains clock early. Then your CPA calls in April: "You owe $73,000 in Alternative Minimum Tax."

You: "But I didn't sell any shares. How do I owe taxes?"

Your CPA: "Welcome to AMT."

Alternative Minimum Tax is the hidden tax trap that catches thousands of tech employees every year. It's confusing, counterintuitive, and expensive, but it's also avoidable if you understand how it works.

Let's break down AMT in plain English so you can plan around it instead of getting blindsided by it.

What Is Alternative Minimum Tax (And Why Does It Exist)?

AMT is a parallel tax system created in 1969 to prevent wealthy individuals from using deductions and loopholes to pay zero federal income tax. It calculates your taxes using different rules (fewer deductions, different rates), and you pay whichever is higher: regular tax or AMT.

The problem? AMT wasn't indexed for inflation for decades, so it started hitting middle and upper-middle-class earners, especially tech employees exercising stock options.

Here's how it works:

Step 1: Calculate your regular income tax using standard deductions, exemptions, and rates.

Step 2: Calculate your AMT tax by adding back certain "preference items" (like the spread when you exercise ISOs) and using AMT rates (26% or 28%).

Step 3: Pay whichever is higher.

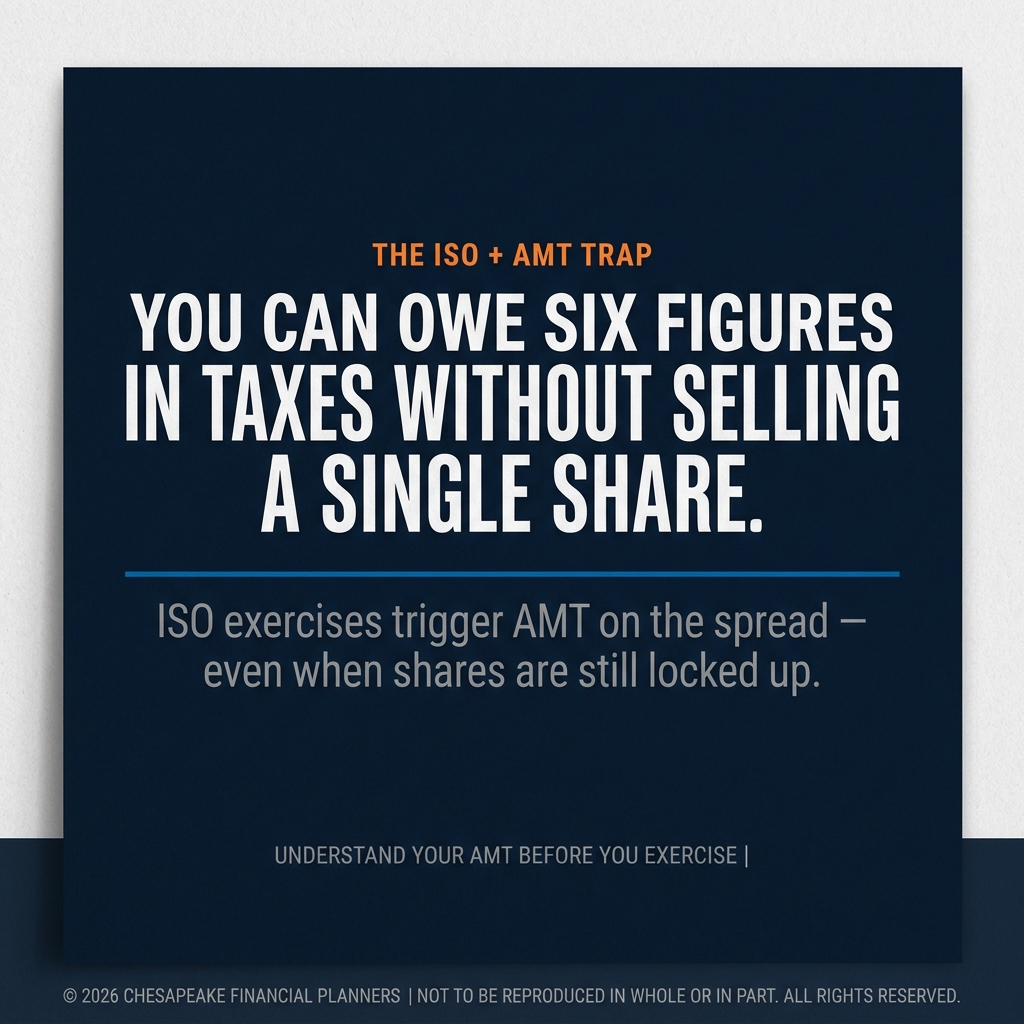

When you exercise Incentive Stock Options (ISOs), the spread between your exercise price and the fair market value becomes an AMT preference item. Even though you haven't sold shares or received cash, the IRS treats that spread as income for AMT purposes.

The ISO + AMT Trap: A Real Example

Let's say you're a senior engineer at a late-stage startup. You have 20,000 ISOs with a $5 strike price. Your company's stock is now valued at $25 per share (based on the most recent 409A valuation).

You decide to exercise all 20,000 options.

The math:

- Exercise cost: 20,000 × $5 = $100,000 (you pay this to your company)

- Fair market value: 20,000 × $25 = $500,000 (what the shares are "worth")

- Spread (FMV – strike price): $500,000 – $100,000 = $400,000

That $400,000 spread is added to your AMT income. If you're already earning $200,000 in salary, your AMT income is now $600,000.

AMT calculation (simplified):

- AMT income: $600,000

- AMT exemption: ~$85,000 (phases out at higher incomes)

- Taxable AMT income: ~$515,000

- AMT tax (28% rate): ~$144,000

Your regular tax (without ISO exercise):

- Taxable income: $200,000

- Regular federal tax: ~$42,000 (using current rates)

What you owe: You pay the higher amount around $144,000 in AMT. That's $102,000 more than you would've paid without exercising ISOs.

And remember: You haven't sold a single share yet. You're out-of-pocket $100,000 for the exercise cost plus $102,000 in extra taxes = $202,000 in cash.

When AMT Becomes a Nightmare

The worst-case scenario happens when your company's stock craters after you've exercised and paid AMT.

The nightmare:

You exercise ISOs, trigger $100,000 in AMT, and pay the tax. Your company's stock was valued at $25 when you exercised. A year later, the market turns, your company's valuation drops, and the stock is now worth $8.

You've paid taxes on $400,000 in "gains" that no longer exist. Yes, you might eventually recoup some of that through AMT credits in future years, but those credits only help if you have regular tax liability exceeding your AMT liability in future years. And they don't give you back the cash you've tied up.

This exact scenario devastated thousands of employees during the dot-com crash in 2000-2001 and has happened repeatedly in market downturns since.

How to Avoid the AMT Trap

You can't eliminate AMT entirely if you're exercising ISOs at a startup with significant appreciation, but you can manage it strategically.

Strategy 1: Calculate Your AMT Exemption "Safe Zone"

The AMT exemption for 2026 is $90,100 for singles ($140,200 for married filing jointly). If your ISO spread plus other income stays below AMT thresholds, you might avoid AMT entirely.

The safe zone: For many tech employees, you can exercise ISOs with a spread of around $75,000-$100,000 without triggering AMT (depending on your other income and deductions).

Action step: Work with a CPA to calculate your personal AMT safe zone. Then exercise only that amount each year, spreading exercises over multiple years to stay below the threshold.

Strategy 2: Exercise Early When the Spread Is Small

If you join a startup early and exercise ISOs when your strike price equals (or is close to) the fair market value, the spread is tiny or zero. This means little or no AMT.

Example: Your ISOs have a $1 strike price, and current FMV is $1.10. If you exercise 50,000 shares, the spread is only $5,000 ($0.10 × 50,000). That's unlikely to trigger meaningful AMT.

Years later, when your company's stock is worth $30, you'll be glad you exercised early. The entire $29 gain per share will be taxed at long-term capital gains rates (if you've met holding periods), and you avoided AMT entirely.

Critical: If you exercise before shares fully vest (early exercise), you must file an 83(b) election within 30 days. Miss that deadline, and you've created a tax disaster.

Strategy 3: Exercise Enough to Trigger AMT, But Not Much More

If you're going to hit AMT anyway, there's a sweet spot where you maximize the value of being in AMT without going way over.

AMT rates are 26% or 28%, often lower than your marginal ordinary income tax rate (32%, 35%, or 37%). If you're definitely in AMT, you can exercise more ISOs at the relatively lower AMT rate.

Why this works: Once you're paying AMT, the incremental cost of exercising additional ISOs is often lower than your regular marginal rate.

This is complex and requires running scenarios with a CPA. Don't DIY this strategy.

Strategy 4: Disqualifying Dispositions (Intentionally Breaking ISO Rules)

If AMT is going to devastate you, you can intentionally "break" ISO tax treatment by selling shares before meeting the holding period requirements (one year from exercise, two years from grant). This is called a disqualifying disposition.

What happens: The sale becomes taxable as ordinary income (like an NSO), but you avoid AMT. The ordinary income offsets the AMT preference item.

When this makes sense: Rarely. You're giving up long-term capital gains treatment to avoid AMT. Usually only makes sense if your company's stock has already declined significantly after exercise, or if AMT would create an unmanageable cash flow crisis.

Strategy 5: Don't Exercise At All (Sometimes the Right Answer)

If exercising ISOs would trigger massive AMT and you can't afford the cash outlay, the right answer might be: don't exercise.

ISOs are valuable only if you can afford to exercise them and if your company ultimately succeeds. If you can't afford the exercise cost + AMT bill, or if your company's liquidity path is uncertain, walking away from options might be the financially sound decision.

Brutal truth: Lots of startup employees forfeit options because they can't afford to exercise. This is why early exercise (when spreads are small) is so powerful. It turns ISOs from "can't afford it" into "already done."

AMT Credits: The Small Consolation Prize

When you pay AMT, you generate AMT credits that you can use in future years when your regular tax exceeds your AMT. These credits don't expire, but they're only useful if you eventually have years where you're paying regular tax (not AMT).

How AMT credits work:

You paid $100,000 in AMT in 2026 because you exercised ISOs. In 2027, you don't exercise any ISOs, and your regular tax is $80,000 while your AMT is $50,000.

You pay $80,000 in regular tax but can use $30,000 of your AMT credit to reduce your bill to $50,000.

Over time, you might recoup the AMT you paid, but it's not guaranteed, and it's not immediate. Don't count on AMT credits to save you.

Your ISO/AMT Action Plan

Before exercising ISOs:

1. Run AMT projections. Don't guess. Work with a CPA to model different exercise scenarios and see which triggers AMT and by how much.

2. Calculate the all-in cost. Exercise cost + AMT + state taxes + cash reserves for potential disasters. Can you afford it?

3. Assess liquidity timeline. When can you realistically sell shares? If liquidity is 5+ years away, can you afford to have cash tied up that long?

4. Diversify the decision. You don't have to exercise all or nothing. Maybe you exercise your AMT safe zone this year and more next year.

After exercising ISOs:

1. File 83(b) if early exercising. You have 30 days. Set three calendar reminders.

2. Track your AMT credit. Keep records of AMT paid. You'll use these credits in future years.

3. Plan your sale carefully. To get long-term capital gains treatment, hold shares 1 year from exercise and 2 years from grant. Selling before that creates a disqualifying disposition.

4. Monitor company progress. If the stock is declining and you're sitting on AMT-triggered losses, consult your CPA about your options.

AMT State Tax Considerations

Most states don't have their own AMT, but they might not conform to federal rules.

California: No state AMT, but California doesn't allow ISO preference exclusions that the federal system does. This can create additional state tax complexity.

Other states: Check your state's treatment of ISO exercises and AMT. Some states have their own parallel systems.

Work with a CPA familiar with your state's rules.

The AMT Calculation (Simplified)

Here's the actual AMT calculation in simplified form:

Step 1: Start with your regular taxable income

Step 2: Add back AMT preference items:

- ISO spread at exercise

- State and local tax deductions

- Certain other deductions

Step 3: Subtract AMT exemption

- $90,100 (single) or $140,200 (married) for 2026

- Exemption phases out at higher incomes

Step 4: Multiply by AMT rate

- 26% on first ~$220,000 of AMT income

- 28% on amounts above

Step 5: Compare to regular tax

You pay whichever is higher.

When to Consult a Professional

You should work with a CPA experienced in equity compensation and AMT if:

- You're planning to exercise ISOs

- The spread on exercise exceeds $50,000

- Your annual income (including equity comp) exceeds $200,000

- You've exercised ISOs in prior years and have AMT credits

- You're considering early exercise

The cost of professional advice ($1,500-$3,000) is trivial compared to the potential AMT savings ($20,000-$100,000+).

Real-World AMT Scenarios

Scenario 1: Young employee, small spread

You join a Series A startup. ISOs have $0.50 strike price, current FMV is $0.75. You exercise 40,000 shares.

- Spread: $0.25 × 40,000 = $10,000

- AMT impact: Minimal. Unlikely to trigger AMT.

- Action: Exercise immediately, file 83(b), start the long-term capital gains clock.

Scenario 2: Late-stage employee, large spread

You join a Series D startup. ISOs have $8 strike price, current FMV is $20. You have 15,000 vested options.

- Spread: $12 × 15,000 = $180,000

- AMT impact: Will definitely trigger AMT, likely $40,000-$50,000 tax bill

- Action: Exercise in tranches over 2-3 years to spread AMT impact. Run projections with CPA first.

Scenario 3: Leaving the company

You're leaving your job. You have 90 days to exercise 10,000 ISOs or they expire. Spread is $25 per share = $250,000.

- AMT impact: ~$65,000 tax bill

- Exercise cost: $100,000 (assuming $10 strike)

- Total cash needed: ~$165,000

- Action: Decide if the company's future justifies $165,000 at risk. If yes, exercise. If no, walk away.

The AMT Recovery Strategy

If you've already paid AMT on ISO exercises, here's how to recover those credits:

Year after large AMT: Don't exercise more ISOs. Let your regular tax exceed AMT so you can use credits.

Future years: As AMT credits reduce your tax bill, you're gradually recovering the AMT you paid.

Worst case: If you never have regular tax exceeding AMT (because you keep exercising ISOs), you might never fully recover credits until you retire or have a low-income year.

Don't Let AMT Paralyze You

AMT is complex and expensive, but it shouldn't prevent you from exercising valuable options.

The key is planning:

- Calculate AMT before exercising

- Understand the all-in cost

- Exercise strategically (early when possible, in tranches when necessary)

- Work with professionals who understand equity comp

Your stock options are part of your compensation. Don't forfeit them because AMT feels too complicated. Understand it, plan for it, and make informed decisions.

This information is not intended to be a substitute for specific individualized tax or investment advice. We suggest that you discuss your specific situation with a qualified tax or financial advisor.

Please consult your tax professional regarding your specific tax situation.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.