Asset protection needs: LLCs and corporations offer liability protection that sole proprietorships don't.

You chose your business structure years ago, probably based on what was easiest to set up or what your attorney recommended at the time. But here's what most business owners don't realize: the entity structure you chose is costing you thousands, maybe tens of thousands, in unnecessary taxes every year.

The Hidden Tax Burden Business Owners Face

Here's the frustrating reality: two identical businesses with identical revenue can pay vastly different tax bills based solely on their entity structure. One owner takes home significantly more money while the other unknowingly overpays the IRS year after year.

The external problem is obvious you're paying too much in taxes. But the internal struggle is worse: the nagging feeling that you're missing something, the confusion about self-employment tax, and the fear that you're leaving money on the table while your CPA gives you generic advice.

Here's the philosophical truth: You shouldn't need a law degree to understand how your business is taxed. The tax code is complex by design, but you deserve clarity about where your money is going. —

Understanding the Four Main Business Tax Structures

We work with business owners every day who are overwhelmed by entity selection and tax planning. Let's break down how each structure is taxed in language that makes sense.

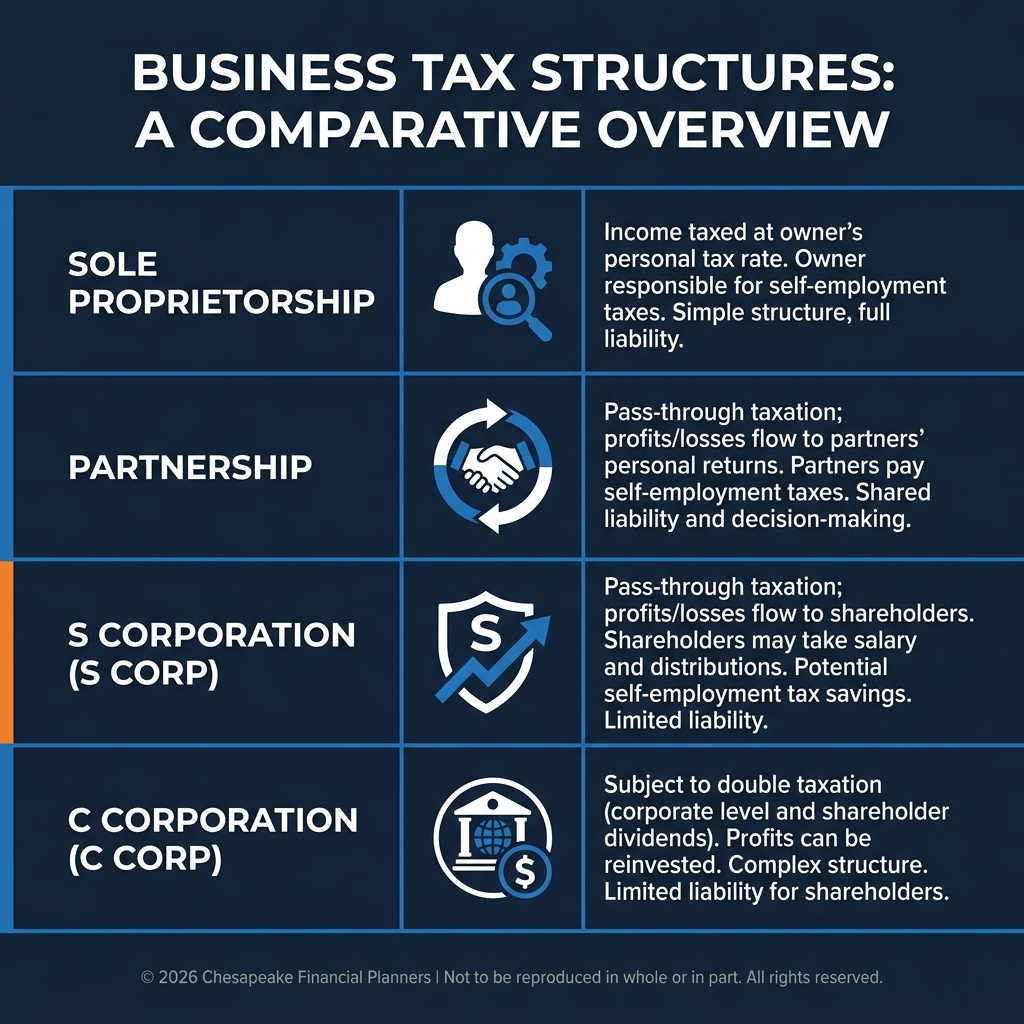

Sole Proprietorship: The Default (and Usually Most Expensive)

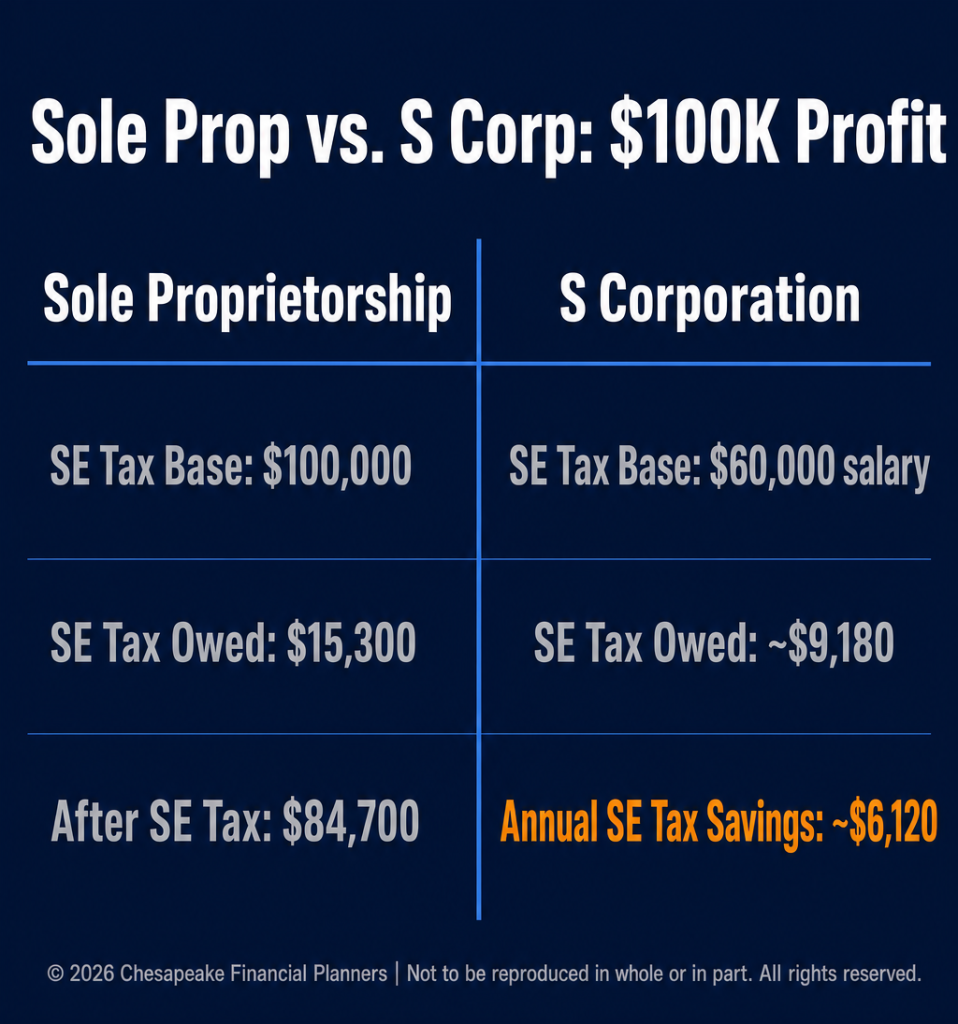

How it's taxed: All business income flows through to your personal tax return on Schedule C. You pay income tax plus self-employment tax (15.3%) on all net profit.[1]

The cost: If your business nets $100,000, you're paying $15,300 in self-employment tax alone, before income taxes.

When it makes sense: You're just starting out with minimal revenue, or you're a true solopreneur with low profit margins.

The trap: Many business owners stay sole proprietors long after it stops making financial sense, simply because they don't know there's a better option. —

Partnership: Similar to Sole Proprietorship

How it's taxed: Income, deductions, and credits pass through to partners' personal returns. Each partner pays self-employment tax on their share of profits.[2]

The cost: Same self-employment tax burden as sole proprietorships, just split among partners.

When it makes sense: You have multiple owners and want operational simplicity without corporate formalities.

The trap: Partners often disagree about tax strategy and distributions, leading to conflict. —

S Corporation: The Tax-Saving Sweet Spot

How it's taxed: Income passes through to your personal return, but here's the key difference you only pay self-employment tax on your W-2 salary, not on distributions.[3]

The savings: If your business nets $100,000, you might pay yourself a reasonable salary of $60,000 (paying SE tax on that) and take $40,000 as a distribution (no SE tax). That saves you approximately $6,100 in self-employment taxes.

When it makes sense: Your business is netting $60,000+ annually and you're tired of writing checks to the IRS for self-employment tax.

The requirements: You must pay yourself a "reasonable" salary, file a separate tax return for the S corp, and follow corporate formalities. You're also limited to 100 shareholders who must be US citizens or residents.

The trap: The IRS scrutinizes S corps where owners pay themselves unreasonably low salaries to avoid payroll taxes. You need documentation for your salary determination. —

C Corporation: For High-Growth Businesses

How it's taxed: The corporation pays tax on its profits at the corporate rate (currently 21%). When you take money out as dividends, you pay tax again on your personal return the infamous "double taxation."[2]

When it makes sense: You're seeking significant outside investment, planning to go public, or need to retain substantial earnings in the business for growth.

The benefit: The 21% corporate rate can be lower than your personal rate if you're a high earner, and you have more flexibility with fringe benefits.

The trap: Double taxation makes C corps expensive for most small business owners who want to take money out regularly. —

How to Choose the Right Structure for Your Business

The optimal structure depends on your specific situation:

- Revenue and profit levels: Higher profits generally favor S corp taxation to save on self-employment taxes.

- Growth plans: Planning to raise capital from investors? C corp may be necessary.

- Number of owners: Multiple owners add complexity, especially for S corps with their strict shareholder requirements.

- Asset protection needs: LLCs and corporations offer liability protection that sole proprietorships don't.

- State taxes: Some states don't recognize S corps or tax them differently. Your state matters.

The Conversion Process

Many business owners can convert from one structure to another, but timing and execution matter:

- Sole prop to LLC: Usually simple and inexpensive

- LLC to S corp: Elect S corp status with the IRS (no need to change your LLC at the state level)

- S corp to C corp: Possible but involves revoking your S election

- C corp to S corp: Allowed but with waiting periods and potential tax consequences

Each conversion has tax implications that must be carefully evaluated. —

What Financial Freedom Looks Like

Imagine keeping an extra $6,000, $10,000, or even $20,000 per year simply by structuring your business correctly. That's real money for retirement savings, business reinvestment, or finally taking that vacation you've been postponing.

You'll have the confidence that comes from knowing your business is structured optimally, not just for taxes, but for asset protection, succession planning, and long-term wealth building. —

Your Three-Step Path Forward

Getting your business structure right doesn't have to be complicated:

- Schedule a complimentary consultation where we'll review your current structure and financial situation

- We'll analyze the tax impact of your current setup versus potential alternatives

- Together we'll create an implementation plan that minimizes taxes while protecting your interests

You've worked too hard to overpay on taxes. Let's make sure your business structure is working for you, not against you.

Ready to stop overpaying the IRS? Schedule your business structure review today.

This article is for educational purposes only and does not constitute tax, legal, or accounting advice. Entity selection has legal, tax, and operational implications. Consult with qualified tax and legal professionals regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.