You've just learned you're inheriting an IRA or 401(k) from a parent or loved one. Along with the grief comes a complex financial reality: inherited retirement accounts come with tax bills and strict rules that, if mishandled, can cost you thousands or even trigger penalties.

The rules changed dramatically in 2020 with the SECURE Act, and again in 2024 when the IRS finally clarified how they'll be enforced. If your understanding of inherited IRAs is based on advice from five years ago, it's probably wrong.

The Old Rules (Pre-2020): The "Stretch IRA"

Before 2020, non-spouse beneficiaries could "stretch" inherited IRA distributions over their own life expectancy potentially decades. A 50-year-old inheriting a $500,000 IRA could take small required minimum distributions (RMDs) each year for 30+ years, allowing most of the money to continue growing tax-deferred.

Those days are gone for most beneficiaries.

The New Rules (Post-2020): The 10-Year Rule

The SECURE Act established new categories of beneficiaries with different rules:

Eligible Designated Beneficiaries (Can Still Stretch)

These special categories can still stretch distributions over their life expectancy:

- Surviving spouses (have multiple options, covered separately below)

- Minor children of the deceased (until age 21, then the 10-year rule applies)

- Disabled or chronically ill individuals (as defined by IRS rules)

- Beneficiaries less than 10 years younger than the deceased

Non-Eligible Designated Beneficiaries (10-Year Rule)

Everyone else: adult children, siblings, nieces, nephews, friends, must withdraw the entire inherited IRA within 10 years of the original owner's death.

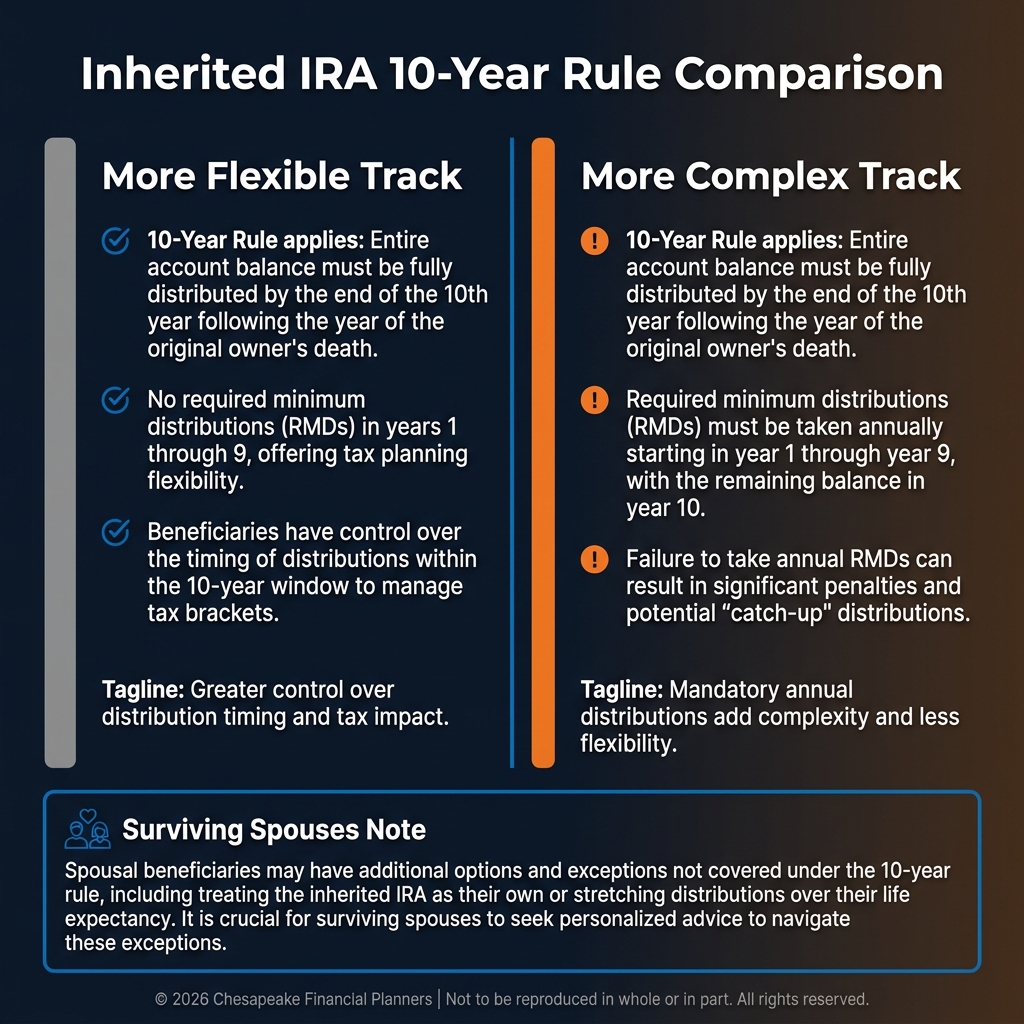

Importantly, the 2024 IRS clarification established:

If the original owner died before their Required Beginning Date (age 73): You can wait until year 10 to take everything. No annual RMDs required in years 1-9.

If the original owner died after their Required Beginning Date: You must take annual RMDs in years 1-9 based on your life expectancy, PLUS drain the account by the end of year 10.

This second scenario is much less flexible and can create larger tax bills.

The Tax Hit: Why This Matters

Inherited traditional IRAs and 401(k)s are taxed as ordinary income when you withdraw. Unlike the original owner who could spread withdrawals over decades, you're now forced to accelerate distributions.

Example:

You inherit a $600,000 traditional IRA. You're 55, earning $120,000 per year, and in the 24% federal tax bracket.

If you wait until year 10 and withdraw everything at once: $600,000 additional income pushes you into the 37% bracket on most of it. Federal tax bill: ~$200,000.

If you spread withdrawals evenly over 10 years: $60,000 per year keeps you mostly in the 24% bracket. Federal tax bill: ~$145,000.

Smart planning saves $55,000 in this example.

Tax Planning Strategies

Strategy 1: Smooth Annual Withdrawals

Instead of waiting until year 10, take roughly equal distributions each year. This keeps you from bracket creep and the 37% top rate.

Even better: Take larger distributions in lower-income years (early retirement, sabbatical, between jobs) and smaller distributions in high-income years.

Strategy 2: Roth Conversions Before Death (For Original Owners)

If you're the IRA owner planning your estate, consider converting traditional IRA money to Roth before death. Your heirs inherit Roth IRAs tax-free (they still face the 10-year rule, but withdrawals are tax-free).

This shifts the tax burden to you at potentially lower rates than your heirs will face.

Strategy 3: Coordinate with Other Income

If you're approaching retirement and expect income to drop, delay inherited IRA distributions until after you retire and are in lower tax brackets.

Conversely, if you're early in your career with lower current income, take larger distributions now before your income increases.

Strategy 4: Charitable Contributions

If you're charitably inclined and over age 70½, you can satisfy your RMD from an inherited IRA through a Qualified Charitable Distribution (QCD). This sends money directly to charity without increasing your taxable income (up to $108,000 in 2026).

Strategy 5: State Tax Planning

If you're considering relocating to a no-income-tax state (Florida, Texas, Nevada, etc.), time your inherited IRA distributions for after the move. On a $500,000 inherited IRA, this could save $25,000-$50,000 depending on your current state's tax rate.

Special Rules for Spousal Beneficiaries

Surviving spouses have unique options not available to other beneficiaries:

Option 1: Treat as Your Own

Roll the inherited IRA into your own IRA. This allows you to delay RMDs until your own RMD age (73-75, depending on birth year) and take distributions based on your life expectancy.

Best for younger spouses who don't need immediate income.

Option 2: Remain a Beneficiary

Keep the inherited IRA as an inherited account. You can take distributions based on your life expectancy starting immediately (or when your spouse would have reached RMD age).

Best for younger spouses (under 59½) who need income now and want to avoid the 10% early withdrawal penalty.

Option 3: 10-Year Rule

Spouses can elect to use the 10-year rule like non-spouse beneficiaries if that's somehow advantageous (rarely is).

Inherited Roth IRAs

Inherited Roth IRAs also face the 10-year rule, but with a crucial difference: withdrawals are tax-free (assuming the original Roth was open for at least 5 years).

This makes inherited Roths much simpler: You can leave the money growing tax-free for 10 years, then withdraw it all in year 10 with no tax consequences.

Penalties to Avoid

The IRS doesn't care about your ignorance of the rules. Mistakes can be expensive:

- Missing RMDs: 25% penalty on the amount you should have withdrawn (reduced from 50% under new rules, but still painful)

- Missing the 10-year deadline: All remaining funds become immediately taxable, potentially pushing you into the highest bracket

- Early withdrawal penalty: Generally doesn't apply to inherited IRAs, but does apply if a spouse rolls an inherited IRA to their own and withdraws before 59½

Estate Planning for IRA Owners

If you own IRAs and want to leave them to heirs:

- Name beneficiaries directly: Don't let IRAs pass through your will or estate. Direct beneficiary designations avoid probate and provide clarity.

- Consider Roth conversions: Pay the tax now at your rate rather than forcing heirs to pay at theirs.

- Update beneficiaries after life changes: Divorce, remarriage, birth of children all require beneficiary updates.

- Don't name your estate as beneficiary: This eliminates the stretch option and forces the 5-year rule (even worse than the 10-year rule).

- Consider trusts for spendthrift heirs: A properly designed trust can protect inherited retirement accounts from beneficiaries' creditors or poor money management.

Document Everything

When you inherit an IRA:

- Request a copy of the original owner's death certificate

- Obtain documentation of the account value on the date of death

- Retitle the account properly: "[Deceased Name] IRA, [Your Name], Beneficiary"

- Work with the custodian to ensure proper inherited IRA setup

- Keep records of all distributions and tax reporting

Improper titling can disqualify the entire inherited IRA, triggering immediate taxation.

The Bottom Line

Inheriting an IRA is a mixed blessing: you receive assets, but with complexity and tax consequences attached. The new 10-year rule accelerates taxation compared to the old stretch IRA, making strategic planning even more critical.

Key takeaways:

- Understand which category of beneficiary you are

- Know whether annual RMDs are required or optional

- Plan withdrawals to minimize tax brackets

- Don't wait until year 10 unless you've modeled the tax impact

- Spouses have special options worth exploring

- Inherited Roth IRAs are simpler and tax-free

The tax implications of inherited retirement accounts are complex enough that professional guidance is usually worthwhile. A few hours with a financial advisor or CPA can save tens of thousands in taxes and penalties.

This information is for educational purposes only and should not be considered tax or legal advice. Inherited IRA rules are complex and subject to ongoing IRS guidance. Consult with qualified tax and legal professionals before making distribution decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.