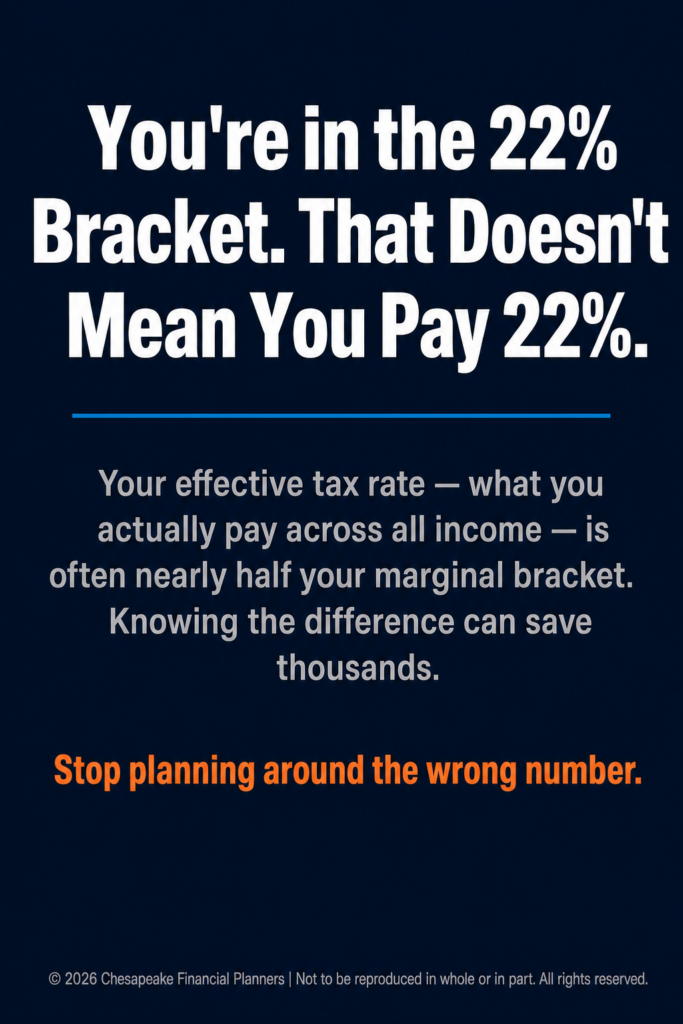

You're in the 22% tax bracket. So every dollar you withdraw from your traditional IRA costs you 22 cents in federal taxes, right?

Wrong. And this misunderstanding costs retirees thousands of dollars in unnecessary taxes and leads to suboptimal financial decisions.

The tax bracket you're "in"—your marginal tax rate—is not the same as the percentage of your total income you actually pay in taxes—your effective tax rate. For most retirees, the difference is substantial, and understanding it is crucial for making smart withdrawal, conversion, and income decisions.

Marginal vs. Effective Tax Rate: What's the Difference?

Your marginal tax rate is the percentage of tax you pay on your next dollar of income. It's the rate that applies to your highest dollars of income.

Your effective tax rate is the total tax you actually pay divided by your total income. It's your average tax rate across all your income.

Here's why they differ: the U.S. has a progressive tax system. You don't pay your marginal rate on all your income—you pay different rates on different portions of income as it fills up each bracket.

A Simple Example

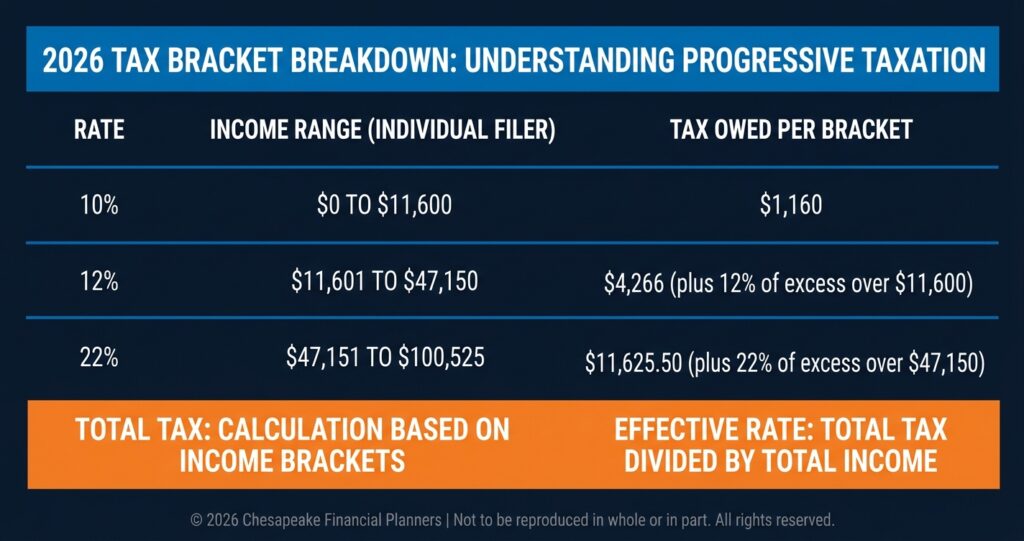

Consider a married couple with $103,000 of taxable income in 2026. They're in the 22% marginal tax bracket (which starts at $100,800 for married filing jointly).

But here's what they actually pay:

- 10% on the first $24,800 = $2,480

- 12% on income from $24,800 to $100,800 = $9,120

- 22% on income from $100,800 to $103,000 = $484

Total federal tax: $12,084

Effective tax rate: $12,084 ÷ $103,000 = 11.7%

They're "in" the 22% bracket, but they're only paying an effective rate of 11.7%. That's nearly half their marginal rate.

Why This Matters in Retirement

Understanding the distinction between marginal and effective rates changes how you think about retirement withdrawals and tax planning strategies.

Withdrawal Decisions

Many retirees obsess about staying in a lower tax bracket, avoiding taking an extra dollar that would push them into the next bracket. But this misses the point.

If you're at the top of the 12% bracket and considering a withdrawal that would push you $10,000 into the 22% bracket, you're not paying 22% on the entire withdrawal. You're paying 12% on most of it and 22% only on the dollars above the bracket threshold.

The tax cost is much lower than many people assume. Sometimes it makes sense to "fill up" your current bracket with strategic withdrawals or Roth conversions, even if it bumps you partially into the next bracket.

Roth Conversion Strategy

Understanding effective vs. marginal rates is crucial for Roth conversion decisions.

When you convert traditional IRA money to Roth, you pay tax at your marginal rate on the converted amount. But you need to weigh this against the taxes you'll pay on future required minimum distributions.

If your current effective rate is 12%, but RMDs will eventually push your effective rate to 18-20%, paying the marginal rate now (even if it's 22% on the last dollars converted) can save taxes overall.

The question isn't just "what bracket am I in now" but "what will my effective rate be over my retirement" versus "what effective rate will I pay if I convert strategically now."

How Standard Deduction Affects Your Effective Rate

The standard deduction creates a powerful tax benefit that significantly reduces your effective tax rate, especially for retirees.

For 2026, the standard deduction is $32,200 for married couples filing jointly ($16,100 for single filers). This means the first $32,200 of income is completely tax-free.

If a married couple has $80,000 of gross income, only $47,800 is taxable after the standard deduction. Their effective rate is calculated on the full $80,000, but they only pay tax on $47,800.

Using our earlier calculation methods:

- 10% on first $24,800 = $2,480

- 12% on remaining $23,000 = $2,760

- Total tax: $5,240

- Effective rate on $80,000 gross income: 6.6%

This couple's effective federal tax rate is less than 7%, even though their marginal rate is 12%. This is why retirees with moderate incomes often pay far less in taxes than they fear.

Social Security Taxation and Effective Rates

Social Security benefits add another layer of complexity to effective tax rates in retirement.

Up to 85% of your Social Security can be taxable, depending on your "combined income." But here's where it gets interesting: the taxation of Social Security benefits is itself progressive.

For many retirees, taking an additional dollar of income doesn't just trigger your marginal tax rate—it also causes more Social Security to become taxable. This creates an effective marginal rate higher than your stated tax bracket.

In some income ranges, an additional $1,000 of income can trigger:

- Tax on the $1,000 at your marginal rate (say, 12%)

- Plus tax on an additional $850 of Social Security that becomes taxable (another 10.2%)

- For a combined effective marginal rate of 22.2% on that $1,000

This is why understanding your true effective rate—including these hidden factors—is so important for retirement planning.

State Taxes Impact Your True Effective Rate

Federal taxes are only part of the picture. State income taxes can add significantly to your effective rate.

State tax rates and structures vary widely:

- High-tax states like California, New York, and New Jersey can add 5-10% to your effective rate

- Moderate-tax states might add 3-5%

- No-income-tax states like Florida, Texas, and Washington eliminate this additional burden entirely

When calculating your true effective tax rate for retirement planning, include state taxes. A 12% federal effective rate might actually be 17-19% once state taxes are factored in, significantly impacting your after-tax retirement income.

Using Effective Tax Rate for Planning

Baseline Your Current Situation

Calculate your effective tax rate for the current year. Take your total tax liability (federal and state) and divide by your gross income. This is your baseline.

Now project this forward: will your effective rate increase or decrease in retirement? If you're currently working and will have lower income in retirement, your effective rate will likely drop substantially. If retirement income is similar to current income (common for high earners), your rate may not change much.

Model Different Scenarios

Use tax software or work with an advisor to model different withdrawal and income scenarios:

- What happens to your effective rate if you withdraw an extra $20,000?

- What if you do a $50,000 Roth conversion?

- How does delaying Social Security affect your effective rate in different years?

These projections reveal opportunities to minimize lifetime taxes that aren't obvious when you only think about marginal rates.

Fill Up Lower Brackets Strategically

If you're early in retirement with low income (maybe you've retired but haven't claimed Social Security yet), your effective rate might be extremely low—perhaps 5-8%.

These are golden years for strategic withdrawals and Roth conversions. Even if you "fill up" the 12% bracket, your effective rate might only reach 8-10%, creating a massive arbitrage opportunity compared to future years when RMDs and Social Security push your rate higher.

Common Misconceptions

"I'm in the 22% bracket, so I shouldn't take more income"

Wrong. You might be able to take substantial additional income at 22% marginal while keeping your effective rate much lower. Focus on effective rates for overall planning, not just avoiding the next bracket.

"My tax bracket is all that matters for Roth conversions"

Wrong. You need to compare your current marginal rate on conversions to your future effective rate on distributions. Sometimes paying a slightly higher marginal rate now saves significant effective rate taxes later.

"Lower income always means lower taxes"

Not necessarily. If that lower income comes from strategies that bunch income or trigger benefit taxation, your effective rate might not drop as much as expected. Structure matters.

The Bottom Line

Your marginal tax bracket gets all the attention, but your effective tax rate is what determines how much of your retirement income you actually keep.

Understanding the difference empowers better decisions about withdrawals, Roth conversions, income timing, and overall retirement tax strategy. Don't let bracket fear prevent you from taking income when your effective rate is low. And don't assume your tax burden based solely on your marginal bracket—calculate your true effective rate to see your real tax picture.

The goal isn't to minimize your marginal rate—it's to minimize your lifetime effective tax rate across your entire retirement. That's a much more nuanced strategy that requires looking beyond simple bracket thresholds to your complete tax situation.

This material is for informational purposes only and should not be construed as tax advice. Tax laws are complex and subject to change. You should consult with a qualified tax advisor regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.