You've decided to start investing. You've opened an account, set up automatic contributions, and now you're staring at a list of fund options. Some say "index fund," others say "actively managed." The expense ratios vary wildly, and you're not sure what any of it means.

Here's what matters. The difference between index funds and actively managed funds will likely determine whether you retire five years early or five years late.

One approach costs less, performs better on average, and requires zero effort. The other costs more, underperforms most of the time, and demands constant monitoring. Yet billions of dollars still flow into actively managed funds every year, often from investors who don't realize they're paying for underperformance.

Here's how to make the choice that actually builds wealth.

What Are Index Funds?

An index fund is designed to mirror the performance of a specific market index like the S&P 500, the total U.S. stock market, or international developed markets.

How it works:

- The fund buys all (or a representative sample) of the stocks in the index

- It holds them in the same proportions as the index

- When the index changes, the fund adjusts automatically

- No fund manager is making bets on which stocks will outperform

The goal isn't to beat the market. It's to match the market at the lowest possible cost.

Examples:

- Vanguard Total Stock Market Index Fund (VTSAX)

- Fidelity 500 Index Fund (FXAIX)

- Schwab Total Stock Market Index Fund (SWTSX)

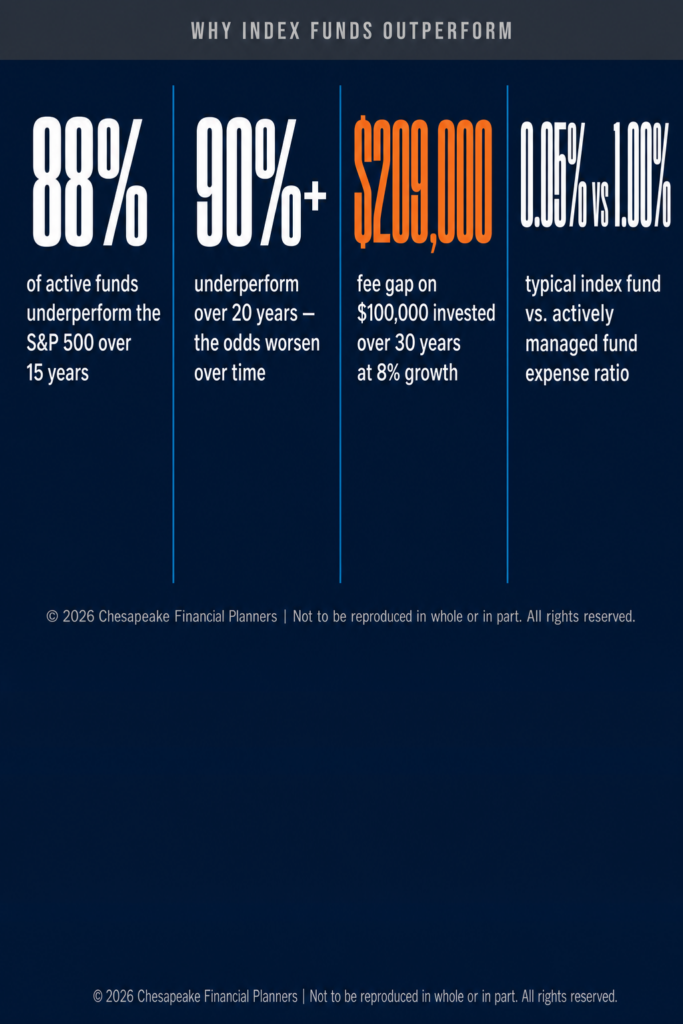

These funds typically have expense ratios between 0.01% and 0.20% per year. On a $100,000 portfolio, that's $10 to $200 annually.

What Are Actively Managed Funds?

An actively managed fund employs a portfolio manager or team who researches companies, analyzes data, and makes decisions about which stocks to buy, sell, and hold.

How it works:

- The fund manager actively selects investments based on research, forecasts, and market timing

- The goal is to beat the benchmark index

- The fund buys and sells frequently to capitalize on perceived opportunities

- You're paying for the manager's expertise, research team, and trading activity

Examples:

- American Funds Growth Fund of America (AGTHX)

- Fidelity Contrafund (FCNTX)

- T. Rowe Price Blue Chip Growth Fund (TRBCX)

These funds typically have expense ratios between 0.50% and 1.50% per year. On a $100,000 portfolio, that's $500 to $1,500 annually.

The Performance Question About Who Actually Wins

The promise of active management is compelling. Skilled professionals using sophisticated analysis to beat the market. The reality is far less exciting.

The Data:

- According to S&P Indices Versus Active (SPIVA) research, over 15 years, 88% of actively managed U.S. stock funds underperformed the S&P 500.[1]

- Over 20 years, that number climbs to over 90%

- The small percentage of actively managed funds that do outperform rarely do so consistently

- Past outperformance is not predictive of future outperformance

Why do active managers underperform so consistently?

1. Fees Erode Returns

A 1% annual fee might not sound like much, but compounded over decades, it destroys wealth. On a $100,000 investment growing at 8% annually for 30 years:

- Index fund (0.05% fee): $970,000

- Active fund (1.00% fee): $761,000

That's a $209,000 difference, just from fees.

2. Trading Costs and Taxes

Active funds trade frequently, generating transaction costs and capital gains taxes (in taxable accounts). Index funds trade minimally, keeping costs and tax drag low.

3. Market Efficiency

In highly efficient markets like U.S. large cap stocks, it's extraordinarily difficult to consistently identify mispriced securities. By the time an active manager spots an opportunity, the market has usually already priced it in.

4. Survivorship Bias

Poorly performing actively managed funds often close or merge with other funds. When researchers look at active fund performance, they're often only seeing the survivors. The data excludes the funds that failed entirely.

The Cost of "Expertise"

Let's be clear. Some actively managed funds do outperform their benchmarks. The problem is identifying them in advance and paying for the attempt.

The average actively managed fund charges about 1% per year. If you have a $500,000 portfolio, that's $5,000 annually. Over 20 years, assuming 7% returns, you'd pay roughly $204,000 in fees.

With an index fund charging 0.05%, you'd pay about $10,000 over the same period. That's a $194,000 difference.

To justify that cost, the active fund would need to consistently outperform the index by more than 1% annually, something 90% of funds fail to do over the long term.

When Might Active Management Make Sense?

There are a few scenarios where actively managed funds could be reasonable:

1. Inefficient Markets

In less efficient markets like small cap international stocks or emerging markets, active managers may have more opportunities to add value through research and selection.

2. Specialized Strategies

If you're pursuing a specific strategy like socially responsible investing with detailed screening criteria, an actively managed fund might be the only way to implement it.

3. Access to Top Talent

If you have access to a truly exceptional manager with a long, consistent track record, and you're investing a large enough sum that fees are negotiable, active management might be worth considering.

But even in these cases, the burden of proof is on the active manager to justify the higher fees.

The Index Fund Advantage of Simplicity and Certainty

Index funds offer something active funds cannot. Certainty of outcome relative to the market.

With an index fund, you know:

- You'll capture the market's return minus a tiny fee

- You won't underperform due to bad manager decisions

- Your costs are predictable and minimal

- You don't need to research funds, track manager changes, or worry about style drift

This doesn't mean you'll get rich quickly. It means you'll get the market's return, which has historically been about 10% annually for U.S. stocks, without giving up 1 to 2% to fund managers who probably won't beat it anyway.

Behavioral Benefits

Index funds also protect you from yourself.

Chasing Performance:

Investors in active funds often chase recent winners, buying after a fund has had a strong run and is likely to revert to the mean. Index funds eliminate this temptation. You're just buying the market.

Manager Risk:

What happens when your star fund manager retires or leaves for a competitor? With an index fund, there's no manager risk. The strategy is the index itself.

Simplicity:

Fewer decisions mean fewer opportunities to make costly mistakes. You pick a low-cost index fund, invest consistently, and let compounding do the work.

How to Choose an Index Fund

Not all index funds are created equal. Here's what to look for:

1. Expense Ratio

Lower is better. For U.S. stock index funds, you should pay no more than 0.10%, and ideally closer to 0.03 to 0.05%.

2. Index Tracked

Do you want total U.S. stock market exposure? S&P 500? International stocks? Bonds? Match the fund to the index that fits your allocation strategy.

3. Tracking Error

The fund should closely match the index it tracks. Check the fund's annual return against the index's return. They should be nearly identical within a few basis points.

4. Fund Size

Larger funds tend to have lower costs and tighter tracking. Avoid brand new or tiny index funds.

5. Provider

Vanguard, Fidelity, and Schwab all offer excellent low-cost index funds. Choose based on where you have your account and which funds have the lowest expense ratios.

The Bottom Line

Index funds win because they're cheaper, simpler, and (on average) outperform the vast majority of actively managed funds over time.

Active management isn't inherently bad. It's just expensive, unpredictable, and statistically unlikely to justify its cost. If you're going to pay for active management, the manager should be able to clearly articulate why they'll outperform and have a long, verifiable track record to back it up.

For most investors, the smarter move is simple. Buy low cost index funds, invest consistently, and let the market do what it's always done, which is to grow over time.

This information is for educational purposes only and should not be considered investment advice. All investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Indexes are unmanaged and cannot be invested in directly. Index fund performance may not match the performance of the underlying index due to fees and expenses. Consult with a qualified financial advisor before making investment decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

References:

[1] "SPIVA U.S. Scorecard Year-End 2023," S&P Dow Jones Indices, 2024

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.