It's the retirement question everyone asks: "How much do I need to retire comfortably?"

You've probably seen rules of thumb online "You need 10 times your salary" or "Save $1 million and you'll be fine." But here's the truth: There's no magic number that applies to everyone.

Your retirement number depends on your lifestyle, spending habits, health, when you retire, where you live, and what "comfortable" means to you.

At Chesapeake Financial Planners, we don't believe in one-size-fits-all retirement planning. We help you calculate your retirement number the amount that supports your goals, values, and vision for retirement.

Why the "magic number" myth doesn't work

"You need $1 million to retire."

Maybe. Or maybe not. One million dollars could be way more than enough: or nowhere near enough, depending on your situation.

Here's why generic advice falls short:

- Your spending is unique: Some retirees live comfortably on $40,000 per year. Others need $150,000+.

- Your income sources vary: Social Security, pensions, rental income, and part-time work all reduce how much you need saved.

- Your retirement timeline matters: Retiring at 55 requires far more savings than retiring at 67.

- Your location affects costs: Housing, taxes, and healthcare costs vary dramatically by state and region.

- Your legacy goals differ: Do you want to leave an inheritance, or are you planning to spend it all?

A comfortable retirement isn't about hitting an arbitrary dollar figure; it's about having a personalized plan that works for your life.

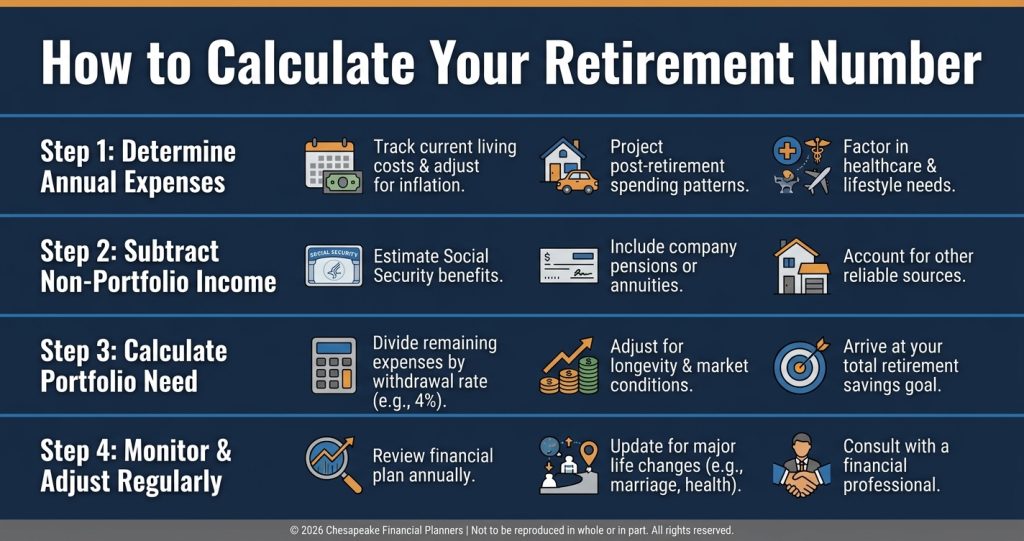

How to calculate your retirement number

Step 1: Estimate your annual spending in retirement

Start by understanding what you'll actually spend. Break it down into categories:

Essential expenses:

- Housing (mortgage, rent, property taxes, insurance, maintenance)

- Healthcare (Medicare premiums, supplemental insurance, out-of-pocket costs)

- Food and utilities

- Transportation

- Insurance

Discretionary expenses:

- Travel and entertainment

- Dining out and hobbies

- Gifts and charitable giving

- Home improvements

One-time expenses:

- Major trips

- Car replacement

- Home repairs or renovations

Many retirees find that their spending stays similar to their pre-retirement spending, or even increases in the early years as they travel and pursue deferred dreams.

A common estimate: Plan for 70–80% of your pre-retirement income as a starting point, then adjust based on your specific plans.

Step 2: Identify your guaranteed income sources

Not all your retirement income needs to come from savings. Factor in:

- Social Security: Most retirees receive $1,500–$3,500 per month, depending on earnings history and claiming age.

- Pensions: If you have a pension, this provides additional contractual income.

- Part-time work: Many retirees work part-time for income, purpose, or social connection.

- Rental income: If you own rental properties, this can provide ongoing cash flow.

- Other income: Royalties, business income, or dividends from investments.

Example: If you need $80,000 per year to live comfortably, and you'll receive $30,000 from Social Security and $10,000 from part-time work, you need your portfolio to generate $40,000 per year.

Step 3: Apply the 4% rule (as a starting point)

The 4% rule suggests you can withdraw 4% of your portfolio annually in retirement with a high probability your money will last 30 years.

Using this rule:

- To generate $40,000 per year, you'd need $1 million saved ($40,000 ÷ 0.04 = $1,000,000)

- To generate $60,000 per year, you'd need $1.5 million

- To generate $80,000 per year, you'd need $2 million

The 4% rule is a helpful benchmark, but it's not perfect. Your actual safe withdrawal rate depends on:

- Your retirement timeline (early retirees may need 3–3.5%)

- Market conditions when you retire

- Your flexibility to adjust spending

- Your asset allocation

Step 4: Account for inflation

Don't forget that costs rise over time. At 3% annual inflation, your expenses will double roughly every 24 years.

If you retire at 65 and live to 90, your $60,000 annual budget will feel more like $30,000 in purchasing power by the end of your retirement.

Strategy: Maintain growth-oriented investments (stocks) throughout retirement to combat inflation.

Step 5: Add a buffer for the unexpected

Healthcare costs, market downturns, home repairs, family emergencies life happens. Build in a cushion:

- Add 10–20% to your estimated retirement number

- Maintain an emergency fund of 1–2 years of expenses in liquid accounts

- Consider long-term care costs (which can be substantial)

How your retirement number changes based on circumstances

Retiring at 55 vs. 67:

If you retire early, you need more savings because:

- Your money needs to last longer (potentially 40+ years)

- You don't have Social Security or Medicare yet

- You have less time to save and benefit from compounding

High cost of living vs. low cost of living:

Where you live dramatically affects how much you need. Retiring in San Francisco or New York City requires far more savings than retiring in a low-cost state like Tennessee or Florida.

Health and longevity:

If you have a family history of longevity, plan for your money to last into your 90s or beyond. If you have health concerns, you may need less but you'll also face higher healthcare costs.

Legacy goals:

If leaving an inheritance is important, you'll need more savings. If your goal is to "die with zero," you can spend more freely.

Beyond the number: What "comfortable" really means

A comfortable retirement isn't just about having enough money; it's about having a plan that gives you:

- Financial security: Confidence that you won't run out of money, even if markets decline or expenses rise.

- Flexibility: The ability to adapt your spending if circumstances change.

- Purpose and fulfillment: Knowing how you'll spend your time and what will give your days meaning.

- Peace of mind: Not worrying about every market dip or unexpected expense.

At Chesapeake, we help clients define what "comfortable" means for them, and then build a plan to make it happen.

Common retirement savings benchmarks

While your number is personal, here are some general guidelines:

By age:

- Age 30: 1x your annual salary saved

- Age 40: 3x your annual salary

- Age 50: 6x your annual salary

- Age 60: 8x your annual salary

- Age 67: 10x your annual salary

By income replacement:

- Replace 70–80% of your pre-retirement income

- Adjust based on your specific spending and lifestyle goals

These are benchmarks, not requirements. If you're behind, don't panic focus on what you can control going forward.

How we help you find your number

At Chesapeake Financial Planners, we go beyond generic rules of thumb. We help you:

- Analyze your current spending and project retirement expenses

- Model different retirement scenarios (retire at 60, 65, 67)

- Optimize Social Security and pension strategies

- Stress-test your plan against market downturns and inflation

- Adjust the plan as your goals and circumstances evolve

We don't just tell you a number; we build a personalized roadmap to get you there.

Your next step

The question isn't just "How much do I need?" it's "How much do I need to live the retirement I want?"

That answer is personal, and it requires a thoughtful, customized plan.

Ready to discover your retirement number? Schedule a complimentary consultation with Chesapeake Financial Planners today.

This material is for educational purposes only and is not intended as investment advice. All investing involves risk, including the potential loss of principal. No investment strategy can guarantee success or protect against loss.

Withdrawal rate strategies do not guarantee that your money will last throughout retirement. Actual results will vary based on market conditions, inflation, and individual circumstances.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.