The life insurance agent throws out a number: "$500,000. Maybe a million. Everyone needs at least that much." But is that true? Or are you about to overpay for coverage you don't need, or worse, underinsure and leave your family financially devastated?

Here's the reality: life insurance needs are deeply personal, based on your income, debts, dependents, and financial goals. There's no one-size-fits-all answer. But there is a methodical way to calculate exactly how much coverage you need. Let's walk through it step by step.

Why Life Insurance Exists

Life insurance isn't about you; it's about protecting the people who depend on your income. If you died tomorrow, life insurance ensures your family can:

- Replace your lost income

- Pay off debts (mortgage, car loans, credit cards)

- Cover immediate expenses (funeral, final medical bills)

- Maintain their standard of living

- Fund future goals (college, retirement)

If no one depends on your income, you might not need life insurance at all. If you're single, no kids, no debt, and no one relying on you financially, life insurance may not be a priority.

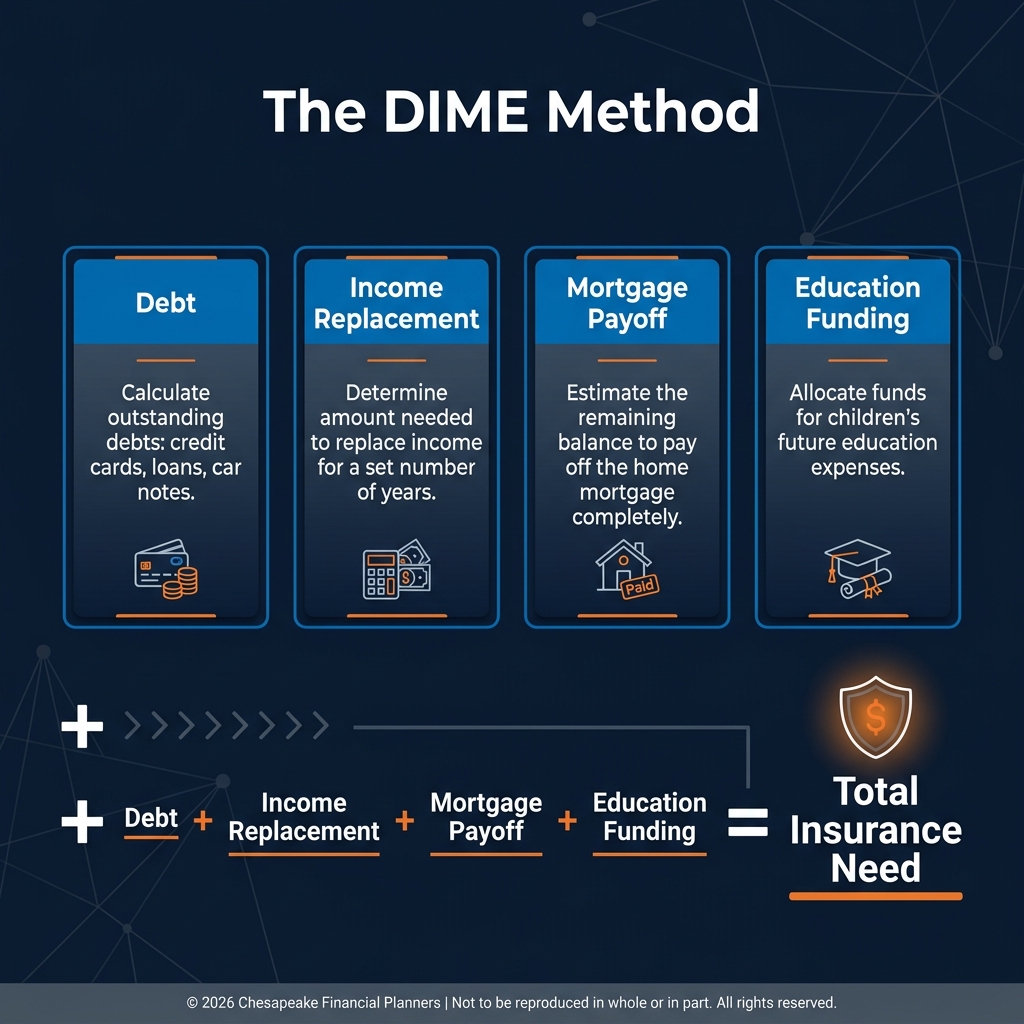

The DIME Method: A Simple Starting Point

A quick-and-dirty calculation to estimate life insurance needs:

- D = Debt (total of all debts: mortgage, car loans, credit cards, student loans, etc.)

- I = Income (annual income x number of years you want to replace—often 5-10 years)

- M = Mortgage (remaining mortgage balance, if not included in "D")

- E = Education (estimated future college costs for children)

Add them up: D + I + M + E = Estimated life insurance need

Example:

- Debt: $50,000

- Income replacement (10 years at $80,000/year): $800,000

- Mortgage: $250,000

- Education costs (2 kids, $100,000 each): $200,000

- Total: $1.3 million

Limitation: This method is a starting point, but it doesn't account for existing savings, Social Security survivor benefits, or your spouse's income.

The Human Life Value Method

This method calculates your economic value to your family over your working years.

Formula:

(Annual income – personal expenses) x remaining working years

Example:

- Annual income: $100,000

- Personal expenses (what you spend on yourself): $20,000

- Economic value to family: $80,000/year

- Remaining working years until retirement: 25 years

- Human life value: $2 million

Limitation: Doesn't account for inflation, changing expenses, or the time-value of money.

The Income Replacement Method (Most Comprehensive)

This method calculates how much capital your family needs to replace your income indefinitely (or until they're self-sufficient).

Formula:

(Annual income x percentage to replace) ÷ expected investment return

Example:

- Annual income: $90,000

- Percentage to replace: 70% (family can adjust lifestyle slightly)

- Income needed: $63,000/year

- Expected safe withdrawal rate: 4%

- Capital needed: $63,000 ÷ 0.04 = $1.575 million

Then add:

- One-time expenses (funeral, final medical bills): $15,000

- Outstanding debts (mortgage, loans): $300,000

- Future goals (college funding): $200,000

Total need: ~$2.1 million

Subtract existing resources:

- Savings and investments: $100,000

- Existing life insurance (through employer): $100,000

- Net life insurance need: ~$1.9 million

Factors That Increase Your Life Insurance Needs

You're the Primary Earner

If your income supports the household, your death would create an immediate and severe financial crisis. You need enough coverage to replace your income for at least 5-10 years, ideally longer.

You Have Young Children

Children are financially dependent for 18+ years. Factor in:

- Daily living expenses

- Childcare costs if the surviving parent needs to work

- College education funding

You Have a Mortgage or Significant Debt

Your family shouldn't lose their home or be burdened by debt. Coverage should be sufficient to pay off the mortgage and any other major debts.

Your Spouse Stays Home or Earns Significantly Less

If one spouse doesn't work or earns much less, the family is heavily reliant on the primary earner's income. Coverage must be robust enough to maintain the family's lifestyle.

You Have Special Needs Dependents

A child or family member with special needs may require lifelong financial support. Life insurance can fund a special needs trust to provide long-term care.

You're Self-Employed or Own a Business

Your death could impact business operations or create tax liabilities. Life insurance can provide liquidity for business succession, buy-sell agreements, or to cover business debts.

Factors That Decrease Your Life Insurance Needs

You Have Substantial Savings and Investments

If you have $1 million in retirement accounts and investments, your family has a financial cushion. You may need less life insurance because existing assets can replace some income.

Your Spouse Has a High Income

If your spouse earns enough to support the family independently, your life insurance needs are lower because the income gap is smaller.

Your Children Are Grown and Financially Independent

Once children are self-sufficient and your mortgage is paid off, your life insurance needs decrease significantly.

You're Close to Retirement with Sufficient Retirement Savings

If you're 60 with $2 million saved for retirement, your family is less dependent on your future income. You may need only enough coverage for final expenses.

Life Insurance for Stay-at-Home Parents

Don't skip life insurance for a non-working spouse. Their contributions—childcare, household management, meal preparation, transportation—have significant economic value.

Cost to replace:

- Childcare: $15,000-$30,000/year

- Housekeeping: $10,000-$15,000/year

- Meal preparation: $5,000-$10,000/year

- Errands and transportation: $3,000-$5,000/year

Total value: $30,000-$60,000/year. If the stay-at-home parent dies, the surviving parent will need to pay for these services while working full-time.

Recommendation: $250,000-$500,000 of term life insurance for a stay-at-home parent.

Types of Life Insurance and Coverage Amounts

Term Life Insurance

Best for: Most people who need high coverage for a limited time (while kids are young, mortgage is unpaid, income is being earned)

Coverage amounts: $250,000 to $2 million+ are common

Cost: Very affordable (often $30-$60/month for $500,000 coverage for healthy 35-year-olds)

Whole Life / Permanent Insurance

Best for: Permanent needs (estate planning, special needs dependents, business succession), wealth building strategies

Coverage amounts: Varies widely; often lower than term for the same premium due to cash value component

Cost: 10-15x more expensive than term for the same death benefit

Common Mistakes to Avoid

- Relying only on employer-provided life insurance: Often 1-2x salary, which is rarely sufficient. Plus, you lose it if you change jobs.

- Buying more than you need: Life insurance agents are often commission-driven. Don't overpay for coverage that doesn't align with your actual needs.

- Ignoring inflation: A $500,000 policy today won't have the same purchasing power in 20 years. Factor in inflation when projecting future needs.

- Not reassessing regularly: Your life insurance needs change as your income, debts, and family situation evolve. Review annually.

Your Life Insurance Checklist

- Calculate your coverage need using one or more methods above

- Get quotes from multiple carriers (term life insurance is highly competitive)

- Choose a term length that aligns with when dependents become self-sufficient (often 20-30 years)

- Apply while you're healthy (rates increase significantly with age and health issues)

- Review annually and adjust as needed (births, home purchases, income changes, debt payoff)

Protect the People Who Count on You

Life insurance isn't about death—it's about love. It's saying, "Even if I'm gone, you'll be okay." It's ensuring your spouse doesn't lose the house, your children can still go to college, and the life you've built together doesn't crumble.

The right amount of life insurance is enough to replace what you provide—financially and practically—without overpaying for coverage you don't need.

Not sure how much life insurance you need? Schedule a complimentary consultation with our team. We'll analyze your income, debts, dependents, and goals to calculate your exact coverage need—and help you find affordable, appropriate protection. Because the people you love deserve financial security, no matter what.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. Life insurance policies contain guarantees and benefits subject to the claims-paying ability of the issuing insurance company.

For educational purposes only. Please consult with a qualified insurance professional regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.