Healthcare costs are the retirement wildcard that can derail even the most carefully constructed financial plan.

You've saved diligently. Your portfolio is diversified. You've calculated your safe withdrawal rate. But have you truly accounted for the fact that a healthy 65-year-old couple will spend an estimated $315,000 on healthcare throughout retirement; and that's before accounting for long-term care?

Healthcare inflation consistently outpaces general inflation. While overall prices might increase 3% annually, healthcare costs often rise 5-7% per year. This differential compounds dramatically over a 20-30 year retirement, potentially doubling or tripling your healthcare expenses beyond what you initially projected.

Here's the uncomfortable truth: most pre-retirees significantly underestimate their retirement healthcare costs. And that optimism gap can force difficult decisions later cutting back on medications, delaying necessary procedures, or depleting savings faster than planned.

Understanding the Full Scope of Healthcare Costs

Healthcare in retirement isn't just doctor visits and prescriptions. It's a complex ecosystem of expenses, many of which aren't obvious until you're facing them.

Medicare Premiums

Medicare Part B (medical insurance) and Part D (prescription drug coverage) require monthly premiums. For 2026, standard Part B premiums are $202.90 per month per person. Part D premiums vary by plan but average around $50 monthly.

That's $3,034.80 annually per person just for basic Medicare coverage—$6,069.60 for a couple—before you've used any healthcare services.

Higher-income retirees face surcharges (IRMAA) that can more than double these premiums. If your modified adjusted gross income exceeds certain thresholds, your Part B premium can reach $689.90 monthly, and Part D adds another $91.00.

Medigap or Medicare Advantage

Original Medicare has gaps—deductibles, copayments, and no out-of-pocket maximum. Most retirees purchase either Medigap (supplemental insurance) or Medicare Advantage to fill these gaps.

Medigap premiums vary widely by plan and location, typically ranging from $100-$400 monthly. Medicare Advantage plans may have lower or zero premiums but often come with higher out-of-pocket costs when you actually use services.

Out-of-Pocket Costs

Even with comprehensive coverage, you'll face deductibles, copayments, and coinsurance. The average retiree spends $4,000-$6,000 annually on these out-of-pocket medical expenses.

Prescription drugs can be particularly expensive, especially for specialty medications that Medicare doesn't fully cover. And dental, vision, and hearing care—services Medicare largely doesn't cover—add thousands more annually.

Long-Term Care

This is where healthcare costs can become catastrophic. Medicare provides minimal long-term care coverage. If you need extended care in a nursing home or assisted living facility, you're largely on your own financially.

The median annual cost for a private room in a nursing home exceeds $116,000. Even in-home care averages $30-$35 per hour. If you need care for several years, these expenses can quickly deplete even substantial retirement savings.

Why Healthcare Costs Are So Unpredictable

Unlike most retirement expenses, healthcare costs don't follow a predictable pattern. You might spend very little in your 60s and early 70s, then face enormous expenses in your 80s due to chronic conditions or acute illnesses.

This unpredictability makes planning difficult. You can't simply average costs over retirement—you need to prepare for scenarios where expenses spike dramatically in later years.

Additionally, healthcare costs correlate with longevity. If you're healthy enough to live into your 90s, you'll face decades of Medicare premiums and routine care costs. But ironically, serious health conditions that shorten lifespan can also generate enormous expenses in a concentrated period.

Strategies to Plan for Healthcare Costs

Start with Realistic Estimates

Don't rely on vague guesses. Use healthcare cost calculators from firms like Fidelity or Vanguard that factor in your age, health status, and retirement timeline. Be conservative—it's better to overestimate and have surplus than underestimate and face shortfalls.

Factor in healthcare inflation at 6% annually, not the general inflation rate. This distinction matters enormously over 20-30 years.

Maximize Health Savings Account (HSA) Contributions

If you're still working and have a high-deductible health plan, max out your HSA contributions. HSAs offer triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Think of your HSA as a dedicated healthcare fund for retirement. Let it grow untouched if you can afford to pay current medical expenses from other sources. By retirement, you'll have a substantial tax-advantaged reserve specifically for healthcare costs.

For 2026, you can contribute $4,400 individually or $8,750 for families, plus an additional $1,000 catch-up contribution if you're 55 or older.

Plan for Medicare Gaps

Research Medigap and Medicare Advantage options before you turn 65. During your initial enrollment period, Medigap insurers can't deny coverage or charge higher premiums based on health conditions. Missing this window can cost you significantly if you develop health issues.

Understand what Medicare doesn't cover: dental, vision, hearing aids, and most long-term care. Budget specifically for these expenses or purchase supplemental coverage where available.

Consider Long-Term Care Insurance

Long-term care insurance is expensive and getting more so as insurers have repriced policies. But for many retirees, it offers crucial protection against catastrophic costs.

The ideal time to purchase is your mid-to-late 50s or early 60s—young enough that premiums are manageable, but old enough that you're actually thinking about retirement and willing to pay for coverage.

Alternatively, hybrid life insurance policies with long-term care riders can provide coverage while guaranteeing a death benefit if you never need care. These products eliminate the "use it or lose it" concern many people have with traditional long-term care insurance.

Create a Dedicated Healthcare Budget

Separate your retirement budget into essential expenses and discretionary spending. Treat healthcare as a non-negotiable essential expense that gets funded first.

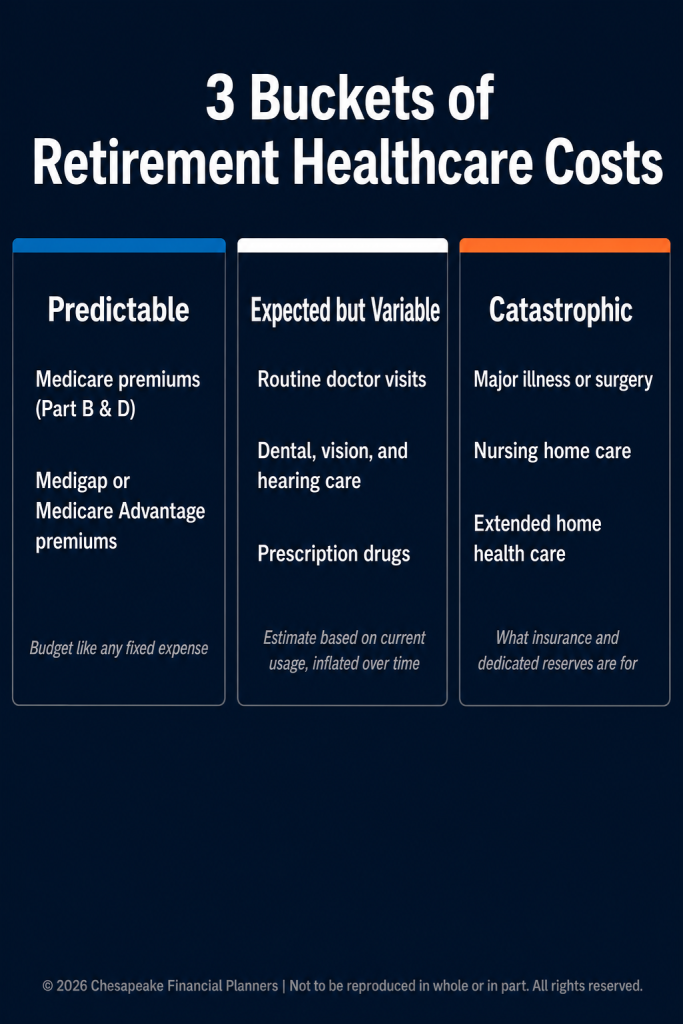

Consider dividing healthcare costs into three categories:

- Predictable (Medicare premiums, Medigap): Budget these annually like any fixed expense.

- Expected but variable (routine doctor visits, prescriptions): Estimate based on current usage, inflated over time.

- Catastrophic (major illness, long-term care): This is what insurance and reserves are for, but also what requires the largest safety margin in your planning.

The Geographic Factor

Where you retire significantly impacts healthcare costs. Medicare premiums are federally standardized, but Medigap premiums, Medicare Advantage options, and out-of-pocket costs vary dramatically by location.

Some states have significantly lower healthcare costs than others. Florida, for example, has competitive Medicare Advantage markets with robust plan options. Other states have limited choices and higher costs.

If you're considering relocating in retirement, factor healthcare costs and provider availability into your decision. Access to high-quality healthcare providers becomes increasingly important as you age.

Build Flexibility Into Your Plan

Healthcare costs are inherently uncertain. Your financial plan must accommodate this uncertainty through flexibility.

Maintain sufficient liquid reserves to cover unexpected medical expenses without disrupting your investment strategy. Having to sell stocks during a market downturn to pay for emergency surgery is exactly the scenario you want to avoid.

Consider keeping 2-3 years of healthcare expenses in easily accessible accounts, separate from your general emergency fund. This dedicated healthcare reserve provides peace of mind and reduces the pressure to tap retirement accounts at inopportune times.

The Role of Preventive Care

One of the most effective ways to control healthcare costs is to stay healthy. Preventive care—regular checkups, screenings, vaccinations, and healthy lifestyle habits—can catch problems early when they're less expensive to treat.

Medicare covers many preventive services at no cost. Take advantage of these benefits. The money you save by preventing or catching conditions early far exceeds the time investment in preventive care.

Moving Forward

Healthcare costs represent one of retirement's largest and most uncertain expenses. But uncertainty doesn't mean you're powerless. By understanding the scope of potential costs, building dedicated reserves, leveraging tax-advantaged accounts, and creating flexible plans, you can prepare for healthcare expenses without letting them dominate your retirement anxiety.

The key is starting this planning early—ideally in your 50s—when you still have time to build healthcare reserves and make strategic insurance decisions. Once you're in retirement and facing health issues, your options become much more limited.

This material is for informational purposes only and should not be construed as insurance or financial advice. Healthcare costs and insurance options vary significantly by individual circumstances. You should consult with a qualified insurance advisor and financial planner regarding your specific situation.

Medicare rules and premiums are subject to change by federal legislation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.