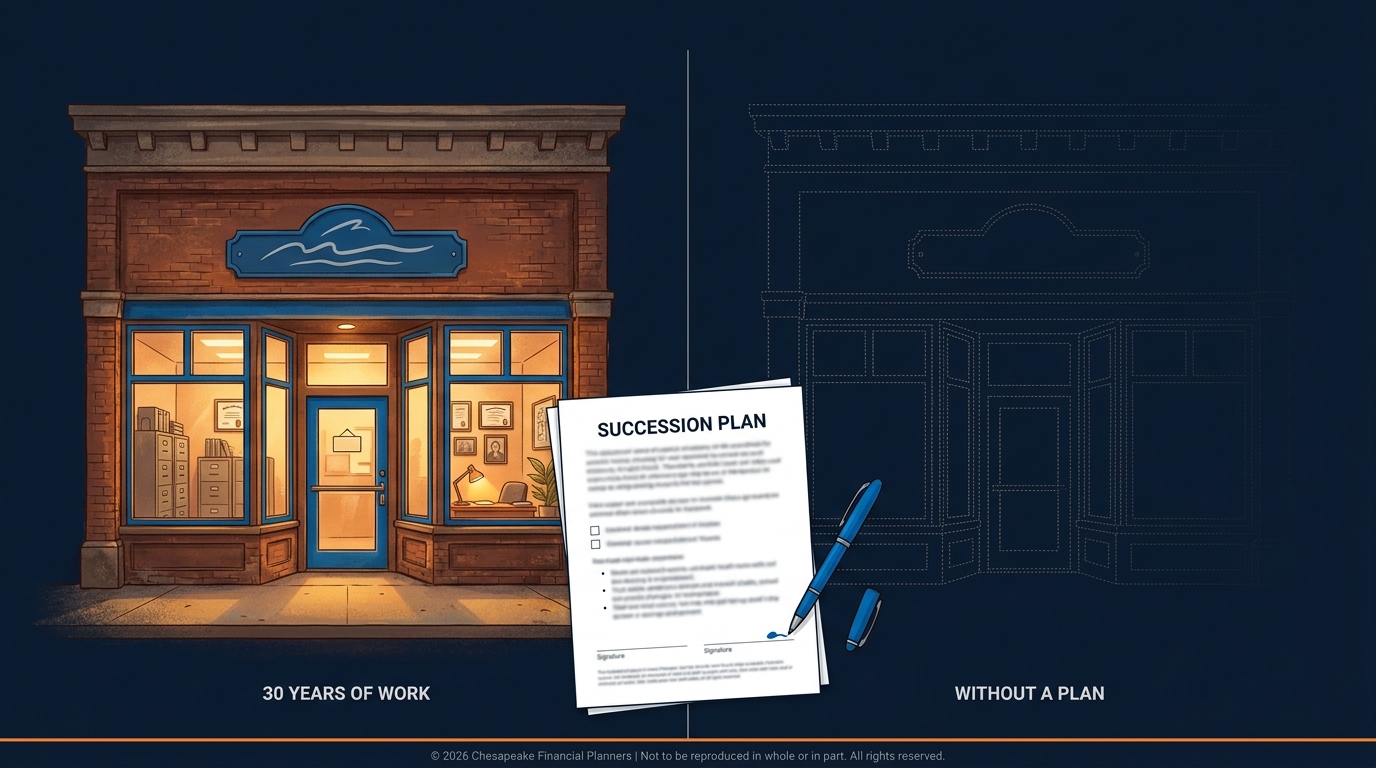

You've spent decades building your business. You've created jobs, served customers, and built something that works. Now you're facing the question that makes many business owners uncomfortable: what happens to this when you're gone?

Business succession planning is the process of deciding who will own and run your company when you exit whether through retirement, disability, or death. It's about preserving the value you've created, protecting your family's financial security, and ensuring your business continues thriving after you're no longer there.

Here's the uncomfortable truth: Without a succession plan, your life's work could evaporate or be sold for pennies on the dollar when you die unexpectedly or become disabled. Your family might face financial disaster. Your employees could lose their jobs. Your business legacy could disappear.

Yet most business owners have no plan. They're too busy running the business to plan its future without them.

Why Business Succession Planning Matters More Than You Think

The statistics are sobering. According to research from the Family Business Institute, only about 30% of family businesses survive into the second generation, and only 12% make it to the third. Most fail not because the business isn't viable, but because of poor succession planning.

What's at Risk Without a Plan?

Your family's financial security. If your business represents 60-80% of your net worth (true for most business owners), your family's financial future depends on maximizing its value when you exit.

Your employees' livelihoods. The people who helped you build your business deserve better than sudden closure or chaotic ownership transition.

Your business legacy. What you built matters. A solid succession plan preserves it.

Tax efficiency. Without planning, your estate could pay 40%+ federal estate taxes plus state taxes on business value. Smart succession planning can reduce or eliminate this.

Operational continuity. Businesses with clear succession plans maintain customer confidence, supplier relationships, and operational stability through ownership transitions.

The Core Components of a Business Succession Plan

Effective succession planning addresses several interconnected questions:

Who Will Own the Business?

Family members? If you have children or other relatives interested and capable of ownership, family succession keeps wealth in the family and preserves legacy.

Key employees? Management buyouts reward loyal employees and ensure continuity, though financing can be challenging.

Outside buyers? Selling to a third party typically maximizes financial value but ends family involvement.

Combination approach? Some businesses transition ownership gradually, with family retaining partial ownership while management runs operations.

Who Will Run the Business?

Ownership and management don't have to be the same. Your son might inherit ownership while a capable non-family executive runs operations. Or you might sell to key employees while your family retains real estate the business leases.

Critical question: Do your intended successors have the skills, experience, and desire to successfully run the business? Wishful thinking destroys more succession plans than any other factor.

When Will the Transition Happen?

Gradual transition: Stepping back over 5-10 years allows mentoring, testing successors, and maintaining continuity.

Immediate (death or disability): Requires robust contingency plans, key person insurance, and clear decision-making authority.

Planned retirement: Gives you maximum control over timing, terms, and transition management.

How Will You (or Your Estate) Get Paid?

Sale to third party: Cash at closing (minus taxes)

Family transfer: Typically below-market price, financed over time, with estate and gift tax planning

Management buyout: Usually requires seller financing since employees lack capital

ESOP: Employee Stock Ownership Plan provides tax benefits and employee ownership

Hybrid approaches: Partial sales, earnouts, ongoing consulting arrangements

The Biggest Succession Planning Mistakes

Avoid these errors that destroy business value and create family conflict:

Starting Too Late

Succession planning should begin 5-10 years before your target exit. Last-minute plans rarely work well. Successors need time to develop skills, prove themselves, and build credibility with customers and employees.

Assuming Your Kids Want the Business

Just because you love the business doesn't mean your children do. Some have no interest. Others lack the skills or temperament. Forcing unwilling or incapable children into succession creates misery for everyone.

Have honest conversations early. If kids aren't interested or capable, explore other options while you have time.

Ignoring Tax Implications

Business transfers trigger estate taxes, gift taxes, capital gains taxes, and income taxes. Without planning, taxes can consume 40-50%+ of business value.

Strategic use of gifting strategies, valuation discounts, trusts, and other techniques can dramatically reduce this burden.

Failing to Address Fairness Among Children

What if one child works in the business and three don't? What if you give the business to one child—does that child owe something to siblings? What if one child is more financially successful and needs less?

Families fracture over perceived unfairness. Address this explicitly in your planning, communicate clearly with all children, and consider equalizing through life insurance or other assets.

Not Preparing Successors Adequately

Handing someone the keys without proper training and mentoring is a recipe for failure. Successful successors typically spend years learning the business, building relationships, and gradually taking on responsibility.

Neglecting Legal Documentation

Good intentions aren't enough. You need:

- Buy-sell agreements that specify terms when owners exit

- Operating agreements or shareholder agreements that define governance

- Estate planning documents that coordinate with succession plans

- Employment agreements for successors

- Non-compete and confidentiality agreements

Tax-Efficient Succession Strategies

Strategic planning can preserve hundreds of thousands or millions in taxes:

Gradual Gifting

Gifting business interests to heirs over time using annual gift tax exclusions ($19,000 per recipient in 2026, $38,000 for married couples) and lifetime exemptions ($15 million in 2026) can remove significant value from your taxable estate.

Valuation discounts for minority interests and lack of marketability can further reduce gift values.

Intentionally Defective Grantor Trusts (IDGTs)

Selling business interests to IDGTs freezes estate values while allowing future appreciation to pass tax-free to heirs.

Family Limited Partnerships (FLPs)

FLPs provide asset protection, estate planning benefits, and centralized management while allowing gradual transfer to next generation with valuation discounts.

ESOPs

Employee Stock Ownership Plans offer unique tax benefits including tax-deferred sale proceeds and potential estate tax elimination, while creating employee ownership.

Charitable Strategies

Charitable remainder trusts (CRTs) or charitable lead trusts (CLTs) can reduce estate taxes while supporting causes you care about and providing family income.

Your Succession Planning Timeline

10+ Years Before Exit:

- Have family discussions about interest and capability

- Begin mentoring and testing potential successors

- Implement gradual gifting strategies

- Build management depth and reduce owner dependence

5-10 Years Before Exit:

- Formalize succession structure

- Execute buy-sell agreements and legal documentation

- Begin formal leadership transition

- Address tax planning opportunities requiring long timelines

2-5 Years Before Exit:

- Transfer day-to-day operations to successors

- Complete major tax planning strategies

- Secure financing if needed for buyouts

- Communicate plan to key stakeholders

0-2 Years Before Exit:

- Finalize all legal and financial arrangements

- Complete ownership transfer

- Transition customer and vendor relationships

- Execute contingency plans for unexpected events

Your Next Steps

Business succession planning is complex, emotional, and critically important. It requires coordination among family members, legal professionals, tax advisors, and financial planners.

Start here:

- Clarify your goals – What matters most? Maximizing value? Preserving legacy? Taking care of family?

- Assess your successors – Who's interested, capable, and willing? Be honest.

- Understand your business value – Get a professional valuation to understand what's at stake

- Model tax implications – Understand the cost of different succession approaches

- Assemble your advisory team – Attorney, CPA, financial advisor who specialize in business succession

- Create your plan – Document decisions and implement legal structures

- Communicate clearly – Share your plan with family and key employees to avoid surprises

The business you've built deserves a succession plan that preserves its value, protects your family, and honors your legacy.

Ready to start your business succession planning? Schedule a consultation to discuss comprehensive strategies.

The information provided is for educational purposes only and should not be construed as legal, tax, or investment advice. Business succession planning is highly complex and depends on individual circumstances. Consult with qualified attorneys, tax professionals, and financial advisors regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.