When you're planning retirement in Maryland, understanding the state's tax landscape can make a significant difference in your financial security. While Maryland offers a high quality of life and proximity to major metro areas, it's not known as the most tax-friendly state for retirees, but with smart planning, you can minimize your state tax burden and make the most of what Maryland does offer.

If you've spent your career in the Baltimore or Chesapeake region, the idea of relocating for tax benefits alone probably feels disruptive. The good news is that with strategic planning, you can optimize your Maryland tax situation without uprooting your life.

Maryland's Tax Structure: What Retirees Need to Know

Maryland uses a progressive income tax system with rates ranging from 2% up to 6.5% at the state level, plus local (county) income taxes ranging from 2.25% to 3.20% depending on your county. This means your combined state and local income tax rate can reach nearly 9% for some households, among the highest in the nation.

Here's what matters for retirees: Maryland taxes most forms of retirement income, including pension income, 401(k) and IRA withdrawals, and investment income. However, the state does provide specific exemptions and deductions that can reduce your taxable income if you know how to use them.

Social Security: Partially Tax-Free in Maryland

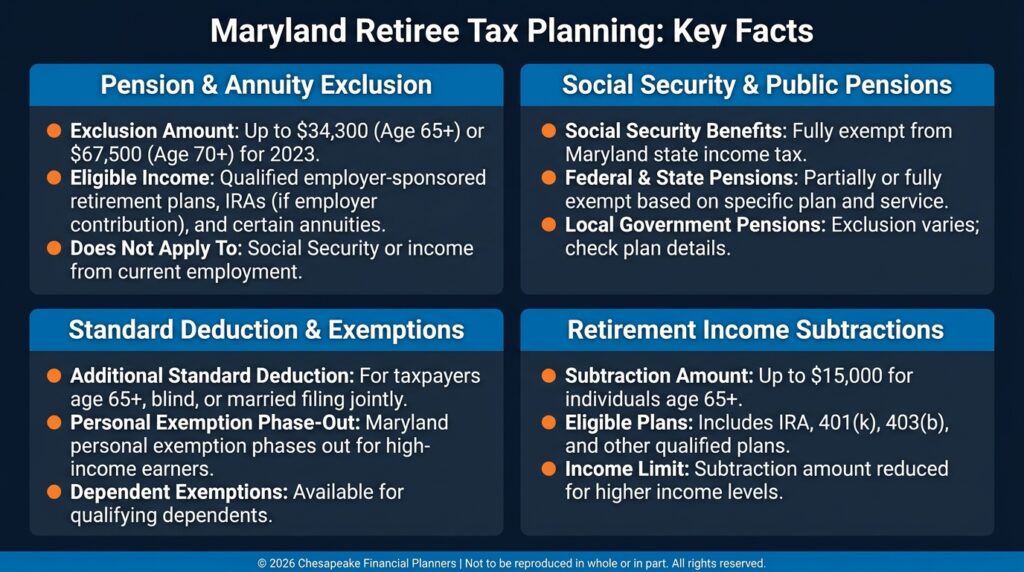

Unlike some states that tax Social Security benefits, Maryland does not tax Social Security (or Railroad Retirement) benefits at the state level.

What this means: Even if part of your Social Security is taxable on your federal return, Maryland allows you to subtract those benefits back out on the Maryland return.

Planning opportunity (still real): While Maryland doesn’t tax Social Security, your Social Security can still be taxable federally depending on your combined income and higher income can also impact Medicare premiums (IRMAA). Coordinating Roth conversions, capital gains, and withdrawal timing can help manage those federal “cliffs,” especially in the early retirement years.

Pension Income: The Retiree Tax Credit

Maryland offers a pension exclusion for taxpayers age 65 and older (or totally disabled, or with a totally disabled spouse). This exclusion can significantly reduce your state tax liability.

The maximum exclusion: For calendar year 2026, the maximum pension exclusion is $40,600 per person (it is adjusted periodically).

What qualifies: The exclusion applies to:

- Pension and annuity income from employer retirement plans

- Traditional IRA and 401(k) distributions

- Military retirement pay

- Other retirement income reported on your federal tax return

Important limitation: The exclusion is reduced dollar-for-dollar by Social Security and Railroad Retirement benefits, which can reduce (or eliminate) the benefit for many retirees.

The planning opportunity: If you're not yet receiving Social Security, you can take full advantage of the pension exclusion while delaying Social Security benefits. This strategy works particularly well for early retirees (ages 62-70) who are drawing from retirement accounts before claiming Social Security.

Property Taxes: Homestead Credits and Senior Freezes

Maryland property taxes vary widely by county, but the state offers several programs to help retirees:

Homestead Tax Credit

This credit limits the annual increase in taxable assessments for your primary residence. The maximum increase is capped at 10% per year statewide, though some counties have lower caps. This protection prevents property tax spikes when home values rise rapidly.

Senior Tax Credit (Property Tax Deferral)

For homeowners with limited income, Maryland offers programs that can reduce property tax burden.

- State Homeowners’ Property Tax Credit: Eligibility includes combined gross household income up to $60,000 (along with other requirements, including a net worth test).

- Harford County specifics: Harford County offers additional local credits (including a senior credit) with eligibility rules that can differ from the state program. Check Harford County’s current requirements for the specific credit you’re applying for.

Estate and Inheritance Taxes: Planning for Heirs

Maryland is one of the few states that imposes both an estate tax and an inheritance tax, though recent reforms have provided some relief.

Maryland Estate Tax

Maryland's estate tax exemption is $5 million per person (set by Maryland law). Estates valued above this threshold face a progressive tax rate up to 16%.

While this exemption is generous, it is significantly lower than the federal estate tax exemption of $15 million per person in 2026 (under OBBBA, with inflation indexing beginning later).

Planning strategy: If your estate approaches or exceeds $5 million, strategic gifting, irrevocable trusts, and portability planning between spouses can help minimize state estate tax exposure.

Maryland Inheritance Tax

Maryland imposes a 10% inheritance tax on property passing to beneficiaries who are not close family members (children, spouses, parents, grandparents, siblings, and certain other relations are exempt).

Key takeaway: If you plan to leave assets to friends, nieces, nephews, or non-family members, proper estate planning can help reduce or eliminate this tax through strategic use of exemptions and gifting strategies.

Tax-Smart Withdrawal Strategies for Maryland Retirees

Given Maryland's tax structure, your withdrawal strategy matters significantly. Here are key approaches:

Manage Your Income to Preserve the Social Security Exemption

Maryland doesn’t tax Social Security benefits, but income management still matters because:

- Social Security can be taxable federally based on combined income, and

- higher income can trigger Medicare premium surcharges (IRMAA) in future years.

Be strategic about:

- Timing Roth conversions: Convert in years when your income is naturally lower

- Capital gains management: Harvest losses to offset gains, or spread large gains across multiple years

- Municipal bond income: Municipal bond interest is generally exempt from federal and Maryland state income tax

Maximize the Pension Exclusion Before Social Security

If you retire before age 70 and delay Social Security, you can often take better advantage of Maryland’s pension exclusion during those early retirement years. Once Social Security begins, the exclusion is reduced by Social Security/Railroad Retirement benefits, so front-loading some retirement account withdrawals earlier can be helpful in the right situation.

Use Roth Accounts Strategically

Roth IRA distributions are tax-free and don't count toward Maryland AGI, making them valuable tools for managing taxable income. Converting traditional retirement accounts to Roth IRAs in low-income years creates a pool of tax-free funds for the future.

Consider Qualified Charitable Distributions (QCDs)

Once you reach age 70½, you can donate up to $100,000 per year from your IRA directly to charity. These distributions count toward required minimum distributions (RMDs) but are excluded from your AGI, which helps with both Social Security exemption thresholds and pension exclusion calculations.

Investment Income and Capital Gains

Maryland taxes capital gains as ordinary income. This means long-term capital gains face the same state and local income tax rates as wages or retirement distributions (up to 8.95% combined). Unlike the federal system, there's no preferential rate for long-term gains.

Planning approach:

- Harvest tax losses to offset gains

- Hold growth investments in Roth accounts where gains are tax-free

- Consider tax-advantaged investments like municipal bonds

- Spread large capital gains across multiple years if possible

Sales Tax and Everyday Expenses

Maryland's statewide sales tax rate is 6%, which is moderate compared to other states. Certain items like groceries and prescription drugs are exempt, which helps retirees on fixed incomes.

Should You Consider Relocating?

Maryland's tax structure prompts some retirees to consider more tax-friendly states like Florida (no income tax), Pennsylvania (no tax on retirement income), or Delaware (no sales tax, moderate income tax). However, taxes are just one factor.

Consider the full picture:

- Proximity to family and social networks

- Quality of healthcare facilities

- Cost of living beyond taxes

- Estate planning implications if you own property in Maryland

For many retirees in the Chesapeake region, the benefits of staying (access to excellent healthcare, proximity to family, established community ties) outweigh the tax savings from relocating. The key is optimizing your Maryland tax situation rather than feeling forced to leave.

Next Steps

Maryland's retirement tax landscape requires active planning, not passive acceptance. The difference between paying full state taxes and strategically minimizing them can be $5,000 to $10,000 per year for a typical retiree couple. That's money that compounds over a 25-30 year retirement.

If you're within five years of retirement in Maryland, a comprehensive tax projection that models different withdrawal strategies, Social Security claiming ages, and Roth conversion opportunities can identify significant savings. This planning is especially valuable for couples with income near the Social Security exemption thresholds or those who can maximize the pension exclusion before claiming benefits.

This content is for educational purposes only and should not be construed as specific tax or legal advice. Maryland tax laws are complex and subject to change. Tax planning decisions should be made in consultation with qualified tax professionals who understand your complete financial situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.