You've reached retirement with multiple accounts: a 401(k), traditional IRA, Roth IRA, taxable brokerage account, and maybe a savings account. You need income to live on. But which account should you tap first?

The order you withdraw from different accounts can save or cost you tens of thousands of dollars in taxes over retirement. More importantly, the right strategy helps ensure your money lasts as long as you do.

Why Withdrawal Order Matters

Different accounts have different tax treatments:

- Traditional IRAs and 401(k)s: Taxed as ordinary income when withdrawn

- Roth IRAs: Tax-free withdrawals (contributions and earnings)

- Taxable brokerage accounts: Taxed on capital gains when you sell (often at lower rates than ordinary income), plus step-up in basis at death

- Health Savings Accounts (HSAs): Tax-free for qualified medical expenses

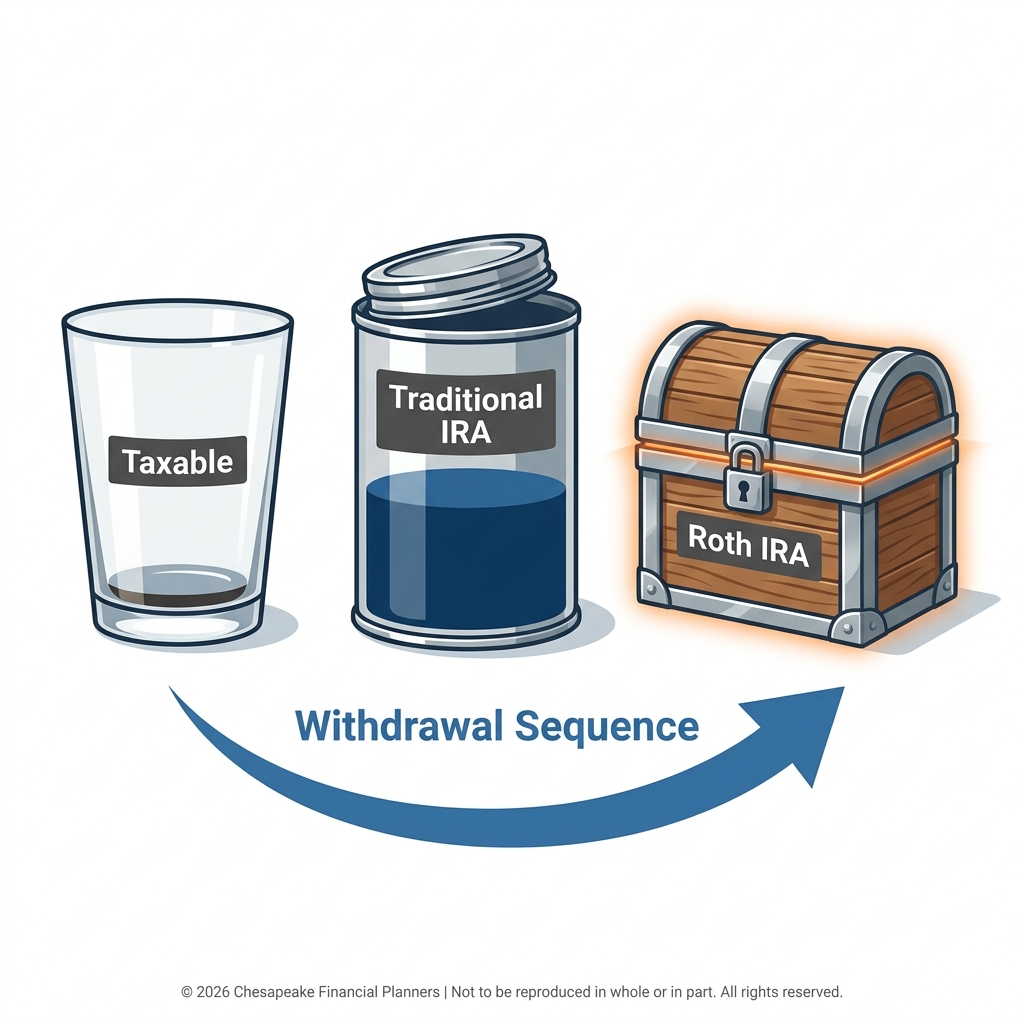

The conventional wisdom says: withdraw from taxable accounts first, tax-deferred accounts second, and tax-free accounts last. But like most conventional wisdom, it's oversimplified.

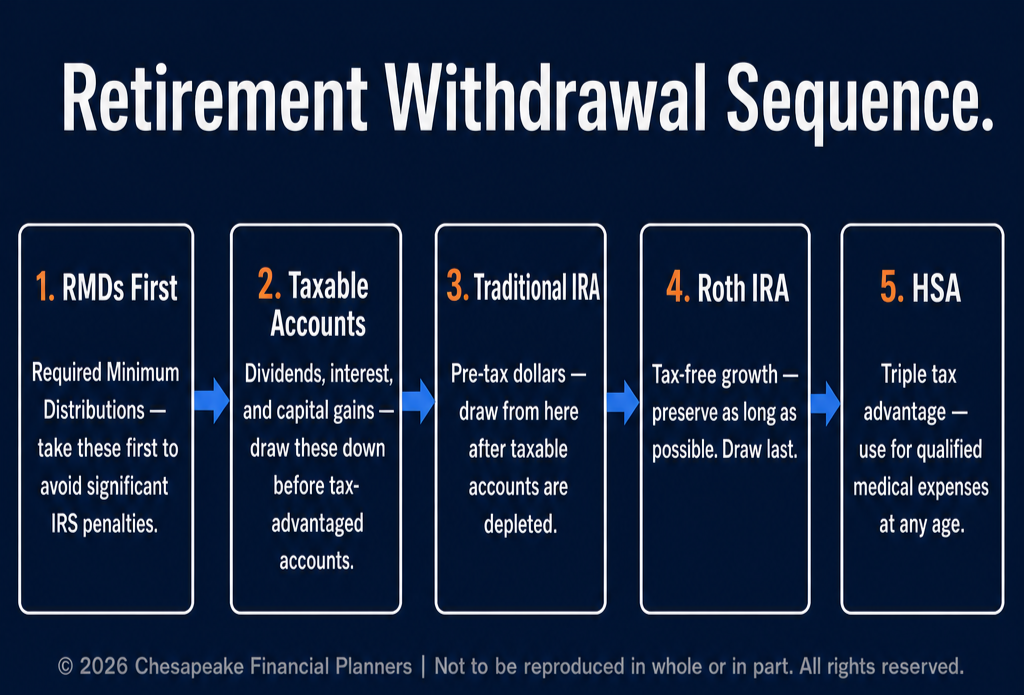

The Standard Withdrawal Sequence

For most retirees, this order makes sense:

Step 1: Required Minimum Distributions (RMDs)

Once you reach age 73 (or 75 if born in 1960 or later), you must take RMDs from traditional IRAs and 401(k)s. These aren't optional the IRS imposes a 25% penalty on amounts you fail to withdraw.

Always satisfy your RMDs first, regardless of what other accounts you have.

Step 2: Taxable Brokerage Accounts

After RMDs, tap your taxable accounts. Why?

- Tax efficiency: Long-term capital gains are taxed at 0%, 15%, or 20% usually lower than ordinary income tax rates on IRA withdrawals.

- Flexibility: You control when you realize gains, allowing for tax planning.

- Estate planning: Assets in taxable accounts receive a step-up in basis at death, meaning your heirs inherit them tax-free. Better to spend these down during life and preserve IRAs if you want to leave a legacy.

- Preserving tax-deferred growth: Leaving IRAs untouched (beyond RMDs) allows more money to grow tax-deferred longer.

Step 3: Tax-Deferred Accounts (Traditional IRAs, 401(k)s)

Once taxable accounts are depleted (or reduced to your desired legacy amount), begin drawing from traditional IRAs and 401(k)s. Withdrawals are taxed as ordinary income, so manage them carefully to avoid jumping into higher tax brackets.

Step 4: Roth IRAs

Withdraw from Roth accounts last. They're the most valuable because:

- Withdrawals are completely tax-free

- No RMDs during your lifetime

- They continue growing tax-free as long as possible

- Your heirs inherit them tax-free (though subject to the 10-year rule)

Roth accounts are your "Plan B" for unexpected expenses and your most valuable legacy asset.

Step 5: Health Savings Accounts (If Applicable)

HSAs are triple-tax-advantaged: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. Save these for healthcare costs in later retirement when expenses typically increase.

When to Deviate From the Standard Strategy

Scenario 1: You're in a Low Tax Bracket

If you retire before Social Security begins or have low income in early retirement, consider taking larger traditional IRA distributions even if you don't need the money.

Why? Fill up the 10% and 12% tax brackets now, before Social Security and RMDs push you into the 22% or 24% brackets later.

You might even convert some traditional IRA money to Roth during these low-income years.

Scenario 2: You're Just Under a Tax Bracket Threshold

If you're close to jumping into a higher bracket, blend withdrawals from taxable and traditional IRA accounts to stay below the threshold.

Example: Your taxable income is $44,000, and the 12% bracket tops out at $50,400 (2026, single). You could take $6,400 from your traditional IRA while staying in the 12% bracket — those dollars taxed at 12% instead of 22% later.

Scenario 3: You're Subject to IRMAA

Medicare premiums increase when your modified adjusted gross income (MAGI) exceeds certain thresholds—called IRMAA (Income-Related Monthly Adjustment Amount).

In 2026, IRMAA kicks in at $109,000 (single) or $218,000 (married). If you're close to these thresholds, manage withdrawals to stay below them and avoid premium surcharges that can add $3,000-$6,000+ per year.

Scenario 4: You Need to Minimize Taxes on Social Security

Up to 85% of Social Security benefits become taxable once your "combined income" exceeds $34,000 (single) or $44,000 (married).

Combined income = AGI + Tax-Exempt Interest + 50% of Social Security

If you're near these thresholds, consider drawing more from Roth accounts (which don't increase combined income) or taxable accounts with minimal gains.

Scenario 5: Market Downturn

During bear markets, avoid selling stocks at depressed prices. Instead:

- Tap your cash reserves (you should have 1-2 years of expenses in cash)

- Draw from bond allocations

- Consider harvesting tax losses in taxable accounts

- Temporarily reduce discretionary spending

This prevents "selling low" and gives your equity positions time to recover.

Advanced Strategies

Roth Conversions in Early Retirement

Before Social Security and RMDs begin, you may have low-income years (ages 62-72). Use this window to convert traditional IRA money to Roth, paying taxes at lower rates.

Benefits:

- Reduces future RMDs

- Creates more tax-free income later

- Lowers taxation of Social Security benefits

- Provides tax-free legacy for heirs

Tax Loss Harvesting

In taxable accounts, sell losing positions to offset gains from winning positions. This allows you to take distributions while minimizing taxes.

Losses can offset up to $3,000 of ordinary income per year, with excess losses carried forward indefinitely.

Qualified Charitable Distributions (QCDs)

If you're age 70½ or older and charitably inclined, direct IRA distributions (up to $108,000 in 2026) straight to charity. This satisfies your RMD without increasing taxable income.

QCDs are especially valuable if you don't itemize deductions.

Laddering Withdrawals

Don't withdraw everything from one account type in a single year. Ladder withdrawals across multiple accounts to smooth your tax bill and maintain flexibility.

Example: Take 40% from taxable, 40% from traditional IRA, and 20% from Roth. Adjust percentages annually based on tax bracket management.

Common Mistakes to Avoid

- Withdrawing only from Roth accounts: This wastes your most tax-efficient money and leaves you with a large traditional IRA that triggers massive RMDs later.

- Ignoring tax brackets: Taking one large distribution instead of spreading it across years can push you into higher brackets unnecessarily.

- Not planning for RMDs: RMDs can create tax surprises in your 70s and 80s if you haven't been drawing down traditional accounts earlier.

- Forgetting about state taxes: Some states tax retirement income, others don't. If you're considering relocating, time large withdrawals for after the move to a tax-friendly state.

- Panic withdrawing during downturns: Selling stocks when they're down 30% locks in losses. Have cash reserves to avoid this.

Creating Your Personal Strategy

Your optimal withdrawal strategy depends on:

- Your current and projected tax brackets

- When you plan to claim Social Security

- Your state of residence

- Healthcare costs and IRMAA exposure

- Legacy goals

- Account balances across different account types

Consider working with a financial advisor or CPA to model your specific situation. Tax planning software can project the lifetime tax impact of different withdrawal strategies.

Annual Review Process

Revisit your withdrawal strategy each year:

- Project your income from all sources

- Calculate your current tax bracket

- Identify IRMAA and Social Security thresholds

- Determine optimal withdrawal amounts from each account type

- Rebalance your portfolio as you withdraw

- Consider Roth conversions if you have room in lower brackets

- Adjust spending if needed based on portfolio performance

The Bottom Line

The "safest" withdrawal strategy isn't just about preserving capital—it's about tax efficiency, flexibility, and ensuring your money lasts throughout retirement.

For most retirees:

- Start with RMDs (when required)

- Draw from taxable accounts

- Tap traditional IRAs strategically

- Preserve Roth accounts for later

- Adjust based on tax brackets and life circumstances

But your situation is unique. The right strategy balances immediate income needs with long-term tax efficiency and legacy goals.

Don't leave tens of thousands of dollars on the table through poor withdrawal sequencing. A little planning goes a long way toward making your retirement savings last—and work harder for you.

This information is for educational purposes only and should not be considered tax or investment advice. Tax rules are complex and subject to change. Consult with qualified tax and financial professionals before making withdrawal decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.