If you're receiving stock options or Restricted Stock Units (RSUs) as part of your compensation package, particularly during a job change or as part of a buyout or merger, you're facing a complex tax situation that can dramatically affect your take-home value.

Equity compensation creates substantial wealth potential, but it also creates substantial tax liability. The difference between handling this strategically versus haphazardly can easily mean tens of thousands of dollars in additional taxes paid or saved. Understanding your options and planning proactively is essential to keeping more of what you've earned.

The Tax Problem with Equity Compensation

Unlike cash salary where taxes are straightforward, equity compensation creates tax events at multiple points: grant, vesting, exercise, and sale. Each event potentially triggers different types of taxes (ordinary income, capital gains, Alternative Minimum Tax) at different rates.

The complexity increases during wealth events. Job changes accelerate decision points. Company acquisitions trigger forced exercises or conversions. Windfalls from successful exits create massive one-year tax hits without proper planning.

Without strategy, you might pay 40-50% of your equity value to taxes. With proper planning, you can potentially reduce that to 20-30% or less, keeping substantially more wealth.

Understanding Your Equity Type

Different equity compensation types follow different tax rules. Your first step is understanding exactly what you have.

Restricted Stock Units (RSUs)

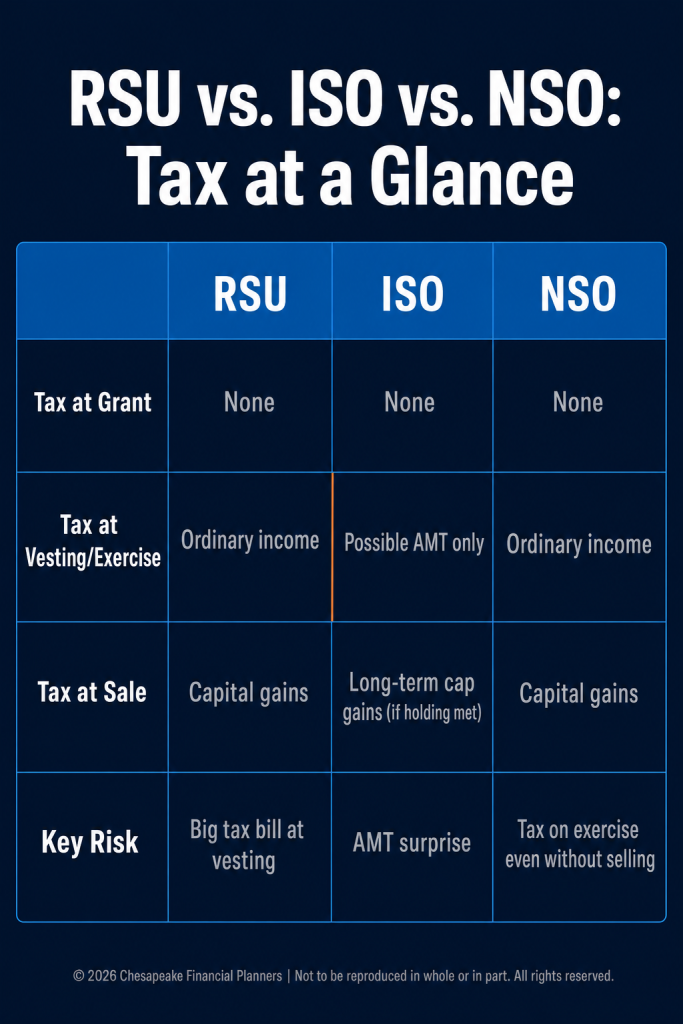

RSUs are company stock granted to you that vests over time (typically 3-4 years). When they vest, you receive actual shares and owe taxes immediately.[1]

Tax treatment:

- No taxes at grant (when you receive the RSU promise)

- At vesting: Ordinary income tax on the full fair market value (taxed like salary)

- Your employer withholds taxes (typically 22% federal, but your actual rate may be higher)

- Your cost basis equals the value at vesting

- When you sell: Capital gains tax on any increase (or loss deduction on decrease) from vesting value

Key issue: Vesting creates a large tax bill whether or not you sell shares. You could owe $30,000 in taxes on a $100,000 vesting event even if you don't sell a single share.

Incentive Stock Options (ISOs)

ISOs provide the right to purchase company stock at a set price (the "strike price"). They offer potential tax advantages but come with complex rules.[2]

Tax treatment:

- No taxes at grant

- No regular taxes at exercise (but potential AMT: Alternative Minimum Tax, implications)

- If you hold shares for 2 years from grant and 1 year from exercise: Long-term capital gains treatment on all profit

- If you sell earlier (disqualifying disposition): Ordinary income tax on the spread at exercise, plus capital gains on any additional growth

Key advantage: Potential for full long-term capital gains treatment (23.8% max federal) instead of ordinary income rates (up to 37% federal).

Key challenge: AMT can create tax liability even when you haven't sold shares, potentially requiring cash payment on paper gains.

Non-Qualified Stock Options (NSOs)

NSOs also provide the right to purchase shares at a strike price, but without ISO tax advantages.

Tax treatment:

- No taxes at grant

- At exercise: Ordinary income tax on the spread (current price minus strike price)

- Your employer withholds taxes

- When you sell: Capital gains on growth from exercise value

Key issue: Like RSUs, exercising creates taxable income and tax liability whether or not you sell shares.

Tax Optimization Strategies for RSUs

Strategy 1: Sell-to-Cover at Vesting

The default approach: When RSUs vest, immediately sell enough shares to cover tax liability, keeping the rest.

Example: 1,000 RSUs vest at $100/share = $100,000 income. You owe approximately $35,000 in taxes (35% combined rate). Sell 350 shares, keep 650 shares.

Advantage: Meets tax obligation while maintaining some stock exposure.

Disadvantage: No additional tax optimization; you pay full ordinary income rates.

Strategy 2: Immediate Full Sale

Sell all shares immediately upon vesting to eliminate concentration risk.

Advantage: Diversifies your wealth; no additional tax if sold at vesting value.

Disadvantage: Gives up potential appreciation; all gains taxed as ordinary income.

Strategy 3: Hold for Long-Term Capital Gains

Keep vested shares at least one year to convert future appreciation to long-term capital gains.

Example: RSUs vest at $100/share. You pay ordinary income tax on $100/share. One year later, stock is $150. If you sell then, the $50 gain is taxed at long-term capital gains rates (~20%) rather than ordinary income rates (~35%).

Advantage: Reduced tax rate on appreciation.

Disadvantage: Concentration risk if too much wealth stays in one stock; no tax benefit on the initial vesting amount.

Strategy 4: Tax Loss Harvesting

If shares decline after vesting, sell them to realize capital losses that offset other gains.

Example: RSUs vest at $100 (you paid tax on this). Stock drops to $75. Sell for a $25/share capital loss that can offset other capital gains or up to $3,000 of ordinary income annually.

Advantage: Converts unfortunate declines into tax benefit.

Tax Optimization Strategies for ISOs

Strategy 1: Exercise and Hold for Qualifying Disposition

Exercise ISOs and hold shares for required periods (2 years from grant, 1 year from exercise) to get full long-term capital gains treatment on all profit.[3]

Example: ISO granted at $10 strike when stock is worth $10. Later, stock is $100. Exercise at $100 (paying $10/share). Hold another year. Sell at $120. All $110/share gain is long-term capital gains.

Advantage: Maximum tax efficiency all gains at favorable long-term rates.

Disadvantage: AMT may be owed in exercise year; concentration risk from holding single stock; risk that stock declines while holding.

Strategy 2: Exercise Early in Low-Value Period

If you have ISOs granted when the company was early-stage and stock value was low, exercising early (even before vesting) can minimize AMT and maximize capital gains treatment.

Example: ISO granted at $1 strike when worth $1. Exercise immediately. No AMT (no spread). All future appreciation is capital gains if held appropriately.

Advantage: Starts capital gains holding period early; minimizes AMT risk.

Disadvantage: Requires cash outlay for shares that may become worthless; risk if company fails.

Strategy 3: Disqualifying Disposition When Advantageous

Sometimes intentionally triggering a disqualifying disposition makes sense.

Example: You exercised ISOs when stock was $50 (strike $10). Stock is now $200. Waiting another 6 months for qualifying disposition means risking $150/share in paper gains. Sell now: $40 ordinary income ($50-$10), $150 capital gains. Max federal tax ~$67/share. If stock drops 50% while waiting, you've lost $100/share trying to save $10/share in taxes.

Advantage: Locks in gains; reduces concentration risk.

Disadvantage: Gives up some tax optimization.

Strategy 4: Manage AMT with Careful Exercise Timing

Alternative Minimum Tax (AMT) is triggered when your ISO spread at exercise (fair market value minus strike price) is large.

Strategies:

- Exercise ISOs in years when your regular income is lower (career breaks, sabbaticals)

- Spread exercises across multiple years to stay below AMT thresholds

- Calculate exactly how many ISOs you can exercise without triggering AMT

- Consider disqualifying dispositions in the same year to reduce AMT impact

Special Situations During Wealth Events

Job Changes

Leaving a company accelerates equity decisions:

RSUs: Often forfeit unvested RSUs when leaving (check your agreement). Negotiate accelerated vesting in severance negotiations.

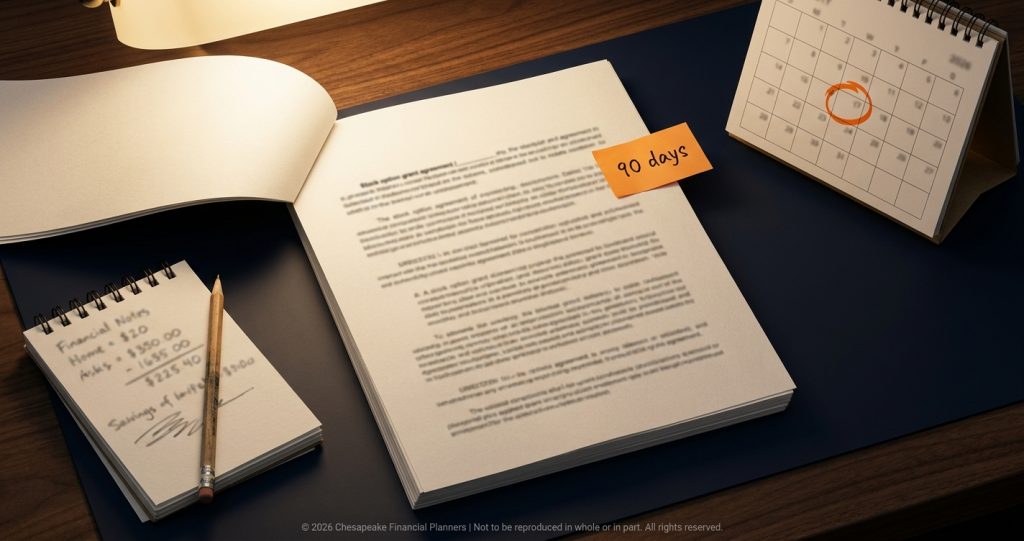

Stock options: Typically have 90 days post-employment to exercise or lose them. This is often insufficient time, especially for ISOs trying to reach qualifying disposition holding periods. Negotiate extended exercise windows (12-24 months) in your departure agreement.

Company Acquisitions

Acquisitions trigger immediate tax consequences:

RSUs: Usually accelerate vesting ("acceleration upon change of control"). All RSUs may vest at once, creating a massive one-year tax hit. Consider estimated tax payments to avoid underpayment penalties.

Stock options: Often exercised automatically or converted to acquiring company's options. Understand the tax implications before the acquisition closes. ISOs may convert to NSOs, losing tax advantages.

Cash-Out Events

If your company is acquired for cash or goes public, consider:

- Max out pre-tax retirement contributions in the windfall year to reduce taxable income

- Make charitable contributions of appreciated stock before sale to avoid capital gains entirely while getting fair market value deduction

- Spread income across years if possible (installment sales, deferred compensation elections)

Tax Planning Essentials

Work with Professionals

Equity compensation taxation is complex enough that DIY approaches often cost more in missed opportunities than professional fees. Consult:

CPA or tax advisor: Model different scenarios; optimize timing; ensure estimated tax payments prevent penalties.

Financial advisor: Integrate equity decisions into overall financial plan; manage concentration risk; optimize asset allocation.

Estate planning attorney: For large equity positions, consider trust structures and gifting strategies.

Track Your Basis Carefully

Keep meticulous records of:

- Grant dates and amounts

- Vesting dates and values

- Exercise dates, prices, and values

- Sale dates and prices

- All tax forms (W-2, 1099-B, 3921, 3922)

Errors in basis reporting can cause you to pay taxes twice on the same income. Your employer's cost basis reporting may be incomplete or incorrect.

Avoid Common Mistakes

Letting the tax tail wag the investment dog: Don't hold concentrated positions just to save taxes if that creates excessive risk.

Ignoring AMT: ISO holders often get surprised by AMT liability. Calculate this before exercising.

Missing estimated tax payments: Large equity vesting creates underpayment penalty risk. Make quarterly estimated payments.

Failing to diversify: Equity compensation creates concentration risk. Sell systematically to diversify regardless of short-term tax consequences.

Equity compensation represents substantial wealth potential, but only if you navigate the tax complexity successfully. Plan proactively, understand your options, and work with professionals to keep more of what you've earned.

This article is for educational purposes only and does not constitute tax, financial, or legal advice. Consult with qualified professionals regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.