Your employer hands you a benefits enrollment packet. Forty pages of insurance options, retirement plans, stock purchase programs, and perks you've never heard of.

You skim it, check a few boxes, and move on. Most people do.

Meanwhile, you're leaving $5,000-$20,000+ per year on the table in benefits you're either not using or not optimizing.

Here's how to actually maximize your employer benefits not just enroll in them.

Start with the Free Money: 401(k) Match

The #1 mistake: not contributing enough to capture full employer match.

Typical match: 50% on first 6% of salary, or 100% on first 3%.

Example:

- Salary: $150,000

- Match: 50% on first 6% ($9,000)

- Free money if you contribute: ~$4,500

- Free money if you don't: $0

That's a guaranteed 50-100% return. No investment beats that.

Action: At minimum, contribute enough to get full match. If tight on cash, contribute to match before paying extra on low-interest debt.

Health Savings Account (HSA): The Triple Tax Advantage

If your employer offers a high-deductible health plan (HDHP) with HSA, this might be your best benefit.

Why HSAs are powerful:

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

That's triple tax advantage better than 401(k) or Roth IRA.

2026 contribution limits: – Individual: $4,400 – Family: $8,750 – Age 55+: Extra $1,000

Strategy: Max out HSA contributions, invest the balance (don't just leave it in cash), and save receipts for future tax-free withdrawals. You can reimburse yourself decades later for old medical expenses.

Think of it as: A stealth retirement account disguised as health insurance.

Employee Stock Purchase Plans (ESPP): Instant Gains

ESPPs let you buy company stock at a discount typically 10-15% below market price.

How it works:

- Contribute up to 10-15% of salary via payroll deduction

- At purchase date, buy stock at discounted price

- Immediate gain = the discount percentage

Example:

- Stock price: $100

- ESPP discount: 15%

- You pay: $85

- Immediate gain: $15 (17.6% return)

Strategy: Enroll, contribute the max, and sell immediately at purchase. Don't hold the stock (concentration risk).

Tax note: Immediate sale triggers ordinary income tax on the discount. Still profitable, just not long-term gains.

Flexible Spending Accounts (FSA): Use It or Lose It

FSAs let you set aside pre-tax dollars for medical or dependent care expenses.

2026 limits: – Healthcare FSA: $3,400 – Dependent Care FSA: $5,000

Benefit: Contributions reduce taxable income.

Risk: "Use it or lose it" unspent funds forfeit at year-end (some plans allow $680 rollover or 2.5-month grace period).

Strategy: Estimate annual expenses conservatively. Better to under-contribute than forfeit.

Good FSA expenses: Glasses, contacts, copays, dental work, orthodontics, daycare.

Life and Disability Insurance: Know What You Have

Most employers provide basic life insurance (1-2x salary) and short-term disability.

Problem: It's not enough.

Life insurance needs:

- If you have dependents, you need 8-12x salary in coverage

- Employer coverage is typically 1-2x salary

- Gap: Buy individual term life to fill the difference

Disability insurance needs:

- Employer coverage is often "any occupation" (pays only if you can't work any job)

- High earners need "own occupation" coverage (pays if you can't do your specific job)

Action: Review employer coverage, then supplement with individual policies.

Commuter and Transit Benefits: Pre-Tax Savings

Many employers offer pre-tax commuter benefits for parking, transit, or rideshare.

2026 limit: $340/month for transit; $340/month for parking (separate limits)

Savings: If you're in 32% bracket, saving $340/month pre-tax = $1,306/year in tax savings.

Note: Often overlooked because it requires active enrollment.

Tuition Reimbursement and Professional Development

Employers may reimburse up to $5,250/year for education tax-free.

Strategy: Use this if pursuing degree, certification, or skills training. Free money for career advancement.

Employee Assistance Program (EAP): Free Counseling and Services

EAPs provide free confidential counseling, legal consultations, financial planning sessions, and more.

Typical offering: 3-10 free sessions per year.

Use cases:

- Mental health counseling

- Marriage counseling

- Legal advice (wills, estate planning)

- Financial planning basics

Most people never use it; but it's included in your benefits.

Wellness Programs and Gym Reimbursements

Many employers offer:

- Gym membership reimbursements ($20-50/month)

- Wellness incentives (rewards for health screenings, fitness goals)

- On-site fitness classes

Strategy: Use these perks. They're designed to be easy wins.

Paid Time Off (PTO): Use It Strategically

Unused PTO is leaving money (and sanity) on the table.

Average: 15-20 days/year, but many people don't use it all.

Strategy: Schedule PTO in advance at year-start. Block it on calendar before meetings fill up.

Retirement Plan Beyond the Match: Roth vs. Traditional

After capturing the match, decide: traditional 401(k) or Roth 401(k)?

Traditional 401(k):

- Contributions reduce current taxes

- Withdrawals taxed in retirement

- Best if: In high bracket now (35-37%), expect lower in retirement

Roth 401(k):

- Contributions are after-tax

- Withdrawals tax-free in retirement

- Best if: In lower bracket now (24-32%), expect higher later, or want tax diversification

Strategy: If employer offers Roth 401(k), consider splitting contributions (50% traditional, 50% Roth) for tax diversification.

Employer Stock: Don't Over-Concentrate

If you receive employer stock (RSUs, ESPP, options), you're at risk of over-concentration.

Rule of thumb: Keep employer stock to <10-15% of net worth.

Strategy: Sell vested equity regularly and reinvest in diversified portfolio.

Annual Benefits Review Checklist

Every year at open enrollment:

Every quarter:

The Hidden Cost of Not Optimizing

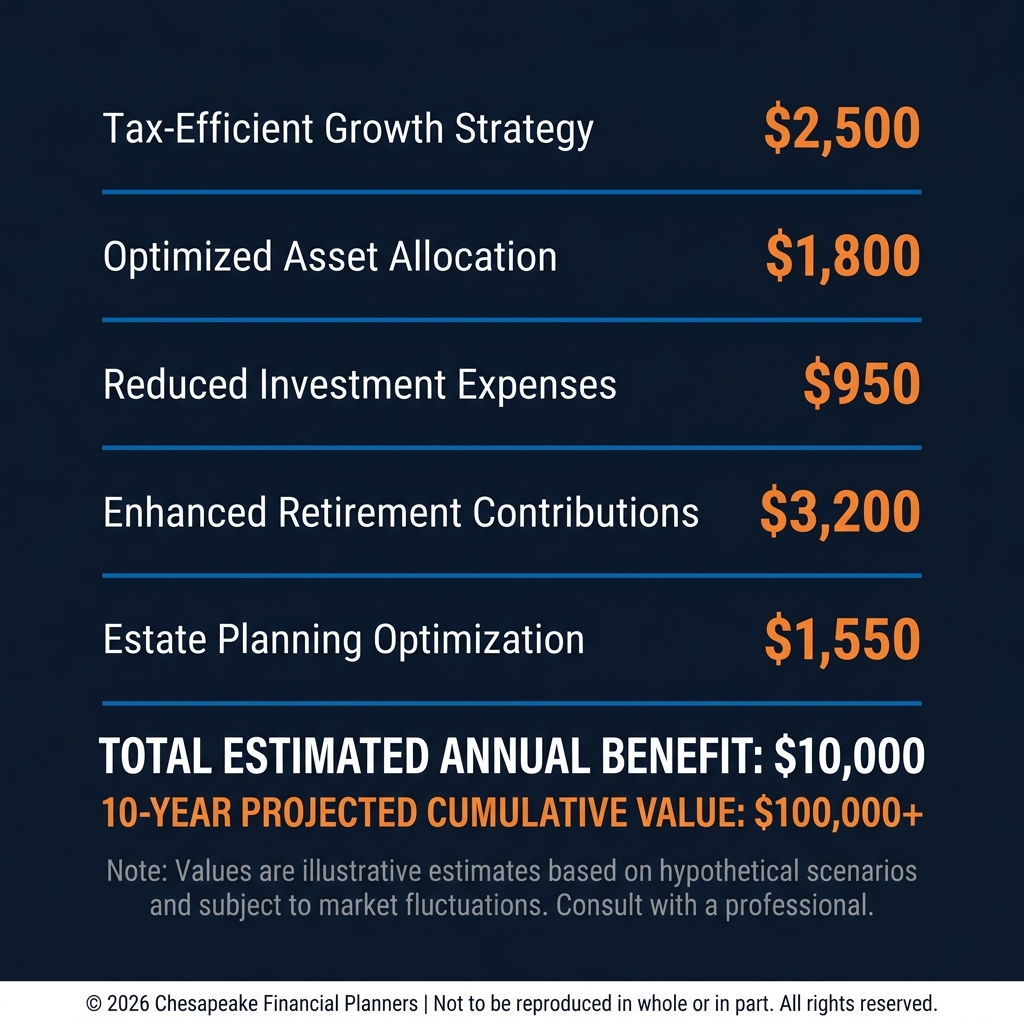

Let's add up what you're leaving on the table:

- 401(k) match: $4,500/year

- HSA max: $8,750/year (potential tax savings ~$2,625 at a 30% marginal rate)

- ESPP: $3,000/year (15% discount on $20K contribution)

- Commuter benefit: $1,306/year tax savings

- Unused PTO: 5 days/year = ~$2,900 (for $150K salary)

Total value: $14,331/year

Over 10 years at 7% returns: $198,000.

That's a down payment on a house, kids' college fund, or years of early retirement just from optimizing benefits you already have.

The Bottom Line

Your benefits package isn't just insurance and retirement. It's part of your compensation—often 20-40% beyond base salary.

Treat it like real money. Because it is.

This content is for educational purposes only and should not be considered as financial, tax, or insurance advice. Employer benefits vary widely by company. Review your specific plan documents and consult with qualified advisors before making decisions.

Tax laws are complex and subject to change. The strategies discussed may not be appropriate for all individuals.

ESPP and equity compensation involve investment risk, including potential loss of principal. Diversification does not guarantee profit or protect against loss.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.