You're considering a pension lump sum or have just received a large one-time payment from a retirement account, inheritance, or business sale. A question you might not have considered: Will this affect your Social Security benefits or Medicare premiums?

The answer is nuanced, and depends on how you receive the money and what you do with it.

Will a Lump Sum Reduce Your Social Security Benefit?

Short answer: No. A pension lump sum, inheritance, or other one-time payment will not reduce your Social Security retirement benefit amount.

Your Social Security benefit is based solely on your lifetime earnings record (specifically, your highest 35 years of indexed earnings). A lump sum payment doesn't change your work history or earnings record, so it doesn't affect your monthly benefit calculation.

Can a Lump Sum Affect Social Security Taxation?

Short answer: Yes, potentially.

While the lump sum doesn't reduce your benefit, it can affect how much of your Social Security is taxable.

Up to 85% of your Social Security benefits become taxable when your "combined income" exceeds certain thresholds:

Combined Income = Adjusted Gross Income + Tax-Exempt Interest + 50% of Social Security Benefits

Taxation thresholds:

- Single: $25,000-$34,000 = up to 50% taxable; above $34,000 = up to 85% taxable

- Married filing jointly: $32,000-$44,000 = up to 50% taxable; above $44,000 = up to 85% taxable

Here's how a lump sum matters:

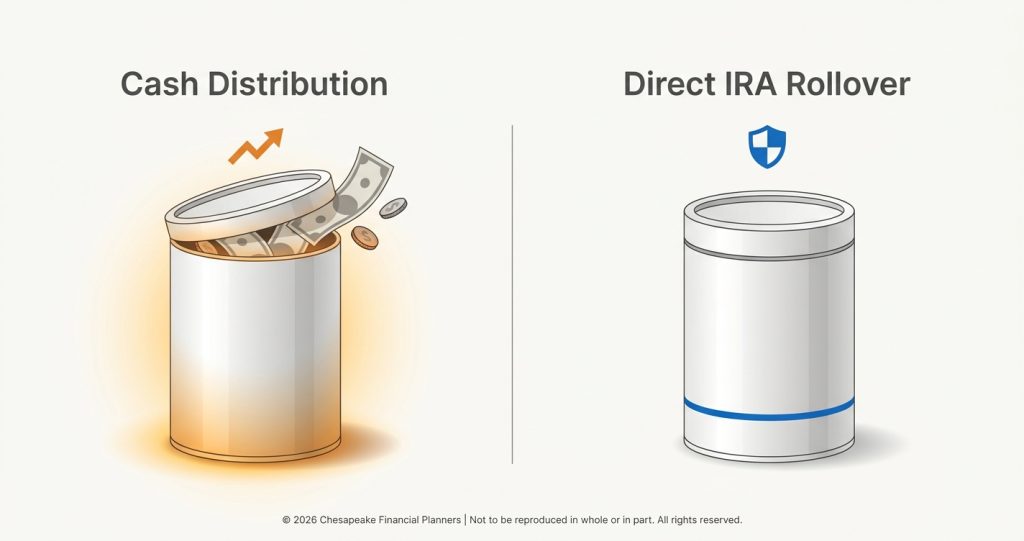

If you take a pension lump sum as cash (rather than rolling it to an IRA), it counts as income in that year. A $400,000 lump sum taken as cash makes far more than 85% of your Social Security taxable that year.

Solution: Roll the lump sum directly to an IRA. The rollover itself isn't taxable income and doesn't affect Social Security taxation. Only future withdrawals from the IRA count as income.

If you inherit a traditional IRA and must take distributions under the 10-year rule, those distributions increase your AGI and can push you above the thresholds, making more of your Social Security taxable.

The Earnings Test (If You Haven't Reached Full Retirement Age)

If you claim Social Security before your Full Retirement Age (FRA) and continue working, Social Security withholds $1 for every $2 you earn above $24,480 (2026 limit).

Important: A pension lump sum does NOT count as earnings for this test.

The earnings test only applies to wages from work or self-employment income. Lump sum payments, investment income, pensions, and IRA distributions don't trigger the earnings penalty.

Once you reach FRA, the earnings test disappears entirely. You can work and collect full Social Security simultaneously, regardless of income level.

Will a Lump Sum Affect Medicare Premiums? (IRMAA)

Short answer: Yes, if it's large enough and not rolled over.

This is where a lump sum can cause real financial impact: IRMAA (Income-Related Monthly Adjustment Amount).

Medicare Part B and Part D premiums increase when your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds.

2026 IRMAA brackets (married filing jointly):

- $218,000 or less: $202.90/month Part B premium per person

- Above $218,000 up to $274,000: $284.10/month Part B premium per person

- Above $274,000 up to $342,000: $405.80/month Part B premium per person

- Above $342,000 up to $410,000: $527.50/month Part B premium per person

- Above $410,000 and less than $750,000: $649.20/month Part B premium per person

- $750,000 and above: $689.90/month Part B premium per person

For singles, thresholds are roughly half these amounts.

If you take a $300,000 pension lump sum as cash, it pushes you into higher IRMAA brackets for that year. This can cost an extra $2,000-$6,000+ in Medicare premiums for that year.

IRMAA Has a Two-Year Lookback

The SSA determines who pays IRMAA based on the income reported two years prior.

Example: Your 2026 Medicare premiums are based on your 2024 tax return.

This creates planning opportunities and traps:

The trap: If you take a lump sum at age 63 (not yet on Medicare), you might forget that two years later at age 65, your Medicare premiums will spike because of that lump sum income.

The opportunity: If you know a large income event is coming, you can plan around it, potentially taking the lump sum in a year when you're not yet subject to IRMAA (before age 63) or by rolling it to an IRA to avoid the income hit.

Strategies to Minimize Impact

Strategy 1: Roll the Lump Sum to an IRA

If you're receiving a pension lump sum or 401(k) distribution, roll it directly to an IRA. This is a tax-free transfer that doesn't count as income.

Benefits:

- No income spike

- No Social Security taxation impact

- No IRMAA impact

- Money continues growing tax-deferred

Only future withdrawals from the IRA count as income for tax and IRMAA purposes; and you control the timing and amount.

Strategy 2: Time Large Distributions Carefully

If you need to take large distributions from retirement accounts, spread them across multiple years to stay below IRMAA thresholds.

Example: Instead of withdrawing $300,000 in one year (triggering high IRMAA), take $100,000 per year for three years. Each year stays below or closer to IRMAA thresholds.

Strategy 3: Use Roth Accounts When Possible

Roth IRA withdrawals don't count as income for IRMAA or Social Security taxation purposes (assuming the account is at least 5 years old and you're over 59½).

If you have money in both traditional and Roth IRAs, draw from the Roth when you need large distributions, especially in years when you're trying to avoid IRMAA.

Strategy 4: File for IRMAA Reconsideration

If a one-time event (like a pension lump sum) causes a temporary income spike, you can file Form SSA-44 to request IRMAA reconsideration if you experienced a "life-changing event":

- Retirement

- Death of spouse

- Divorce

- Work reduction

- Loss of income-producing property

If approved, Medicare will recalculate your premiums based on your current year income (or a reasonable estimate) rather than the two-year lookback.

This can save thousands in the year following a lump sum.

Strategy 5: Delay Medicare Enrollment

If you're still working with employer health coverage and take a lump sum at age 65-66, consider delaying Medicare enrollment by a year.

As long as you have creditable employer coverage, you can delay Part B enrollment without penalties. By the time you enroll, the lump sum income will be outside the two-year lookback window.

What About Medicaid?

If you're concerned about qualifying for Medicaid for long-term care in the future, a lump sum can affect eligibility.

Medicaid has strict asset limits (typically $2,000-$3,000 for individuals). A large lump sum in a bank or investment account counts toward this limit.

If Medicaid planning is relevant to your situation, consult with an elder law attorney about strategies like:

- Medicaid-compliant annuities

- Irrevocable trusts

- Strategic spend-down

- Spousal protections

Documentation and Reporting

Keep detailed records:

- IRA rollover confirmations (showing no taxable distribution)

- 1099-R forms from pension/retirement distributions

- Documentation of direct rollovers vs. taxable distributions

- Tax returns showing income levels for IRMAA appeals

If Social Security or Medicare incorrectly assesses your income, you'll need documentation to correct it.

The Bottom Line

A pension lump sum or other large one-time payment:

Will NOT:

- Reduce your Social Security benefit amount

- Count as "earnings" for the Social Security earnings test

- Affect eligibility for Social Security or Medicare

Might:

- Increase taxation of your Social Security benefits (if taken as taxable income)

- Trigger higher Medicare premiums (IRMAA) for one or more years

- Affect Medicaid eligibility if long-term care is a concern

Best practice: Roll lump sums to IRAs when possible, spread large distributions across years, use Roth accounts strategically, and be aware of the two-year IRMAA lookback when planning large withdrawals.

A little planning can save thousands in taxes and Medicare premiums while preserving your Social Security benefits exactly as calculated.

This information is for educational purposes only and should not be considered tax, legal, or financial advice. Social Security and Medicare rules are complex and subject to change. Consult with qualified professionals before making decisions.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.