You created a financial plan. You set goals, built strategies, and mapped out a path toward financial security. And then life happened.

Maybe you're getting married. Maybe you're selling your business. Maybe you've experienced a death in the family or received an unexpected windfall. These aren't minor adjustments to your financial picture; they're fundamental shifts that can invalidate assumptions your original plan was built on.

The question isn't whether you should update your financial plan after a big life event. The question is how quickly you can get it done before making decisions that could derail your long-term goals.

Why Life Events Require Plan Updates

Financial plans are built on assumptions: your income, expenses, family situation, business ownership, risk tolerance, and timeline. When a major life event changes any of these variables, your plan needs to adjust accordingly.

Consider what changes:

Marriage

Two individuals with separate financial lives merge into one. Income changes. Expenses change. Tax situations change. Beneficiary designations need updating. Estate plans require revision. Insurance needs shift.

Business Sale

Your net worth suddenly becomes liquid. Your primary asset shifts from your business to cash and investments. Your income source disappears. Tax planning becomes critical. Investment strategy needs complete restructuring.

Death of a Spouse

Income may decline dramatically. Estate proceeds might create liquidity. Beneficiary designations must be updated. Financial goals and lifestyle expectations change.

Inheritance

Your asset base increases. Tax strategies might need adjustment. Estate planning becomes more critical. Risk management needs may change.

Each of these events invalidates assumptions your current plan relies on. Continuing to follow an outdated plan is like driving with an old map you might arrive somewhere, but probably not where you intended.

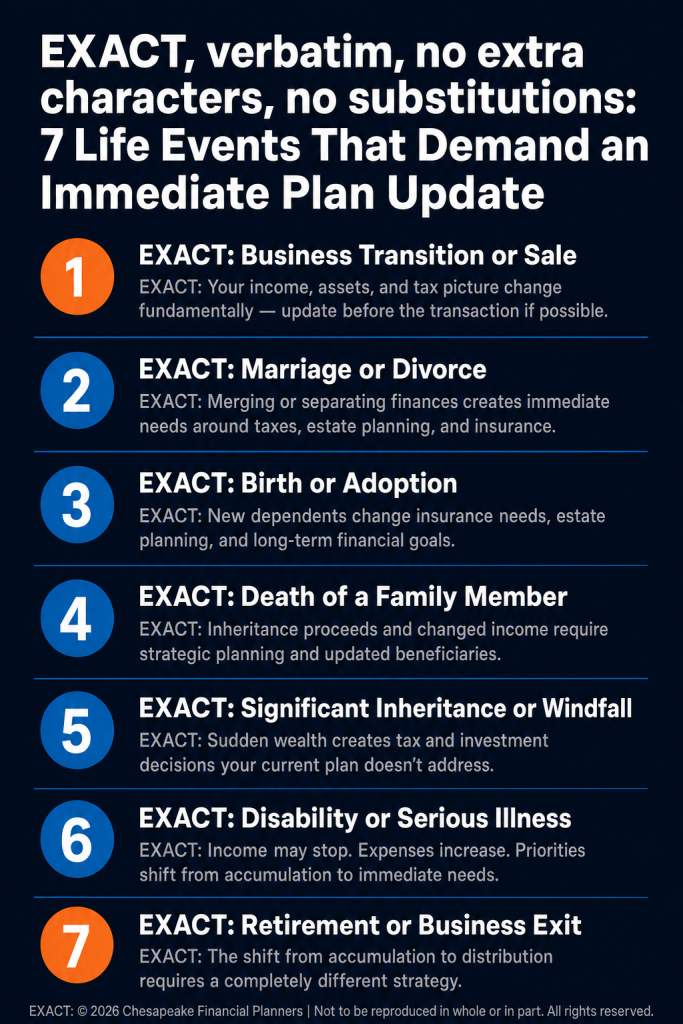

Life Events That Demand Immediate Plan Updates

Not every life change requires a complete financial plan overhaul. A salary increase or job change within the same industry might need minor adjustments. But these events require comprehensive plan updates:

- Business transition or sale: Whether you're selling, transitioning to family, or closing your business, this fundamentally reshapes your financial life. Update your plan before the transaction if possible, not after.

- Marriage or divorce: Merging or separating finances creates immediate planning needs around taxes, estate planning, insurance, and asset ownership.

- Birth or adoption of a child: New dependents change insurance needs, estate planning, education funding, and long-term financial goals.

- Death of family member: Loss of a spouse, parent, or child reshapes your financial picture and goals. Inheritance proceeds require strategic planning.

- Significant inheritance or windfall: Sudden wealth creates tax planning opportunities, investment decisions, and potential lifestyle implications that your current plan doesn't address.

- Disability or serious illness: Income may decline or stop. Expenses often increase. Financial priorities shift dramatically toward current needs rather than long-term accumulation.

- Retirement or business exit: The shift from accumulation to distribution requires completely different strategies for tax management, investment allocation, and income planning.

If you've experienced any of these events within the past 12 months and haven't updated your financial plan, you're operating with outdated guidance.

What an Updated Plan Should Address

Updating your financial plan isn't just changing a few numbers in a spreadsheet. It's reassessing your entire financial situation in light of new circumstances.

For Business Owners Who Sold

- Immediate tax planning: What's the tax bill from the business sale? Are there strategies to minimize taxes on the proceeds? Should you make large charitable contributions this year while income is high?

- Investment strategy redesign: You went from concentrated business ownership to liquid assets. How should those assets be invested? What's your risk tolerance now that your income is no longer dependent on the business?

- Income replacement planning: How will you replace the income your business provided? Do you need an immediate income stream, or can you delay distributions to manage taxes?

- Estate planning updates: Your estate just grew significantly. Are current estate structures appropriate, or do you need trusts, gifting strategies, or other advanced planning?

For Individuals Who Married

- Beneficiary designation updates: Update all retirement accounts, life insurance policies, and bank accounts to reflect your new marital status.

- Combined tax planning: File jointly or separately? How do combined incomes affect tax brackets? Should you adjust withholdings?

- Coordinated insurance: Do you need life insurance to protect your spouse? Disability insurance to replace income? Long-term care planning?

- Aligned financial goals: What are you working toward together? Retirement at the same time or different ages? Geographic preferences? Risk tolerance alignment?

For Individuals Who Received Inheritance

- Tax optimization: Depending on what you inherited (cash, stocks, real estate, retirement accounts), there may be significant tax planning opportunities.

- Asset integration: How does the inheritance fit into your existing portfolio? Should you keep inherited investments or sell and reallocate?

- Goal acceleration or adjustment: Does the inheritance allow you to retire earlier, help children more, or pursue goals that previously weren't financially feasible?

The Updating Process

Updating your financial plan should follow a structured process, not ad hoc adjustments.

- Document what changed. List all the financial implications of your life event. New income? Lost income? New assets? Changed expenses? Different family situation?

- Reassess your goals. Do your goals remain the same, or has the life event changed what you're working toward? A business owner who just sold might shift from "grow wealth" to "preserve wealth and generate income."

- Update all assumptions. Income projections, expense expectations, tax rates, investment allocations, insurance needs—everything built into your original plan needs fresh review.

- Identify new strategies. What planning opportunities does this life event create? Are there tax strategies, estate planning techniques, or investment approaches that now make sense but didn't before?

- Update all legal documents and accounts. Wills, trusts, powers of attorney, beneficiary designations, and account titling all need to reflect your new situation.

- Implement changes. Don't just update the plan on paper—execute the necessary trades, policy changes, and account adjustments to bring your actual financial life in line with the new plan.

The Cost of Not Updating

What happens if you don't update your plan after a major life event?

- You make decisions based on outdated assumptions. A business owner who sold their business but continues following a plan built for someone actively running a business might take inappropriate risks or miss critical tax planning opportunities.

- You leave legal documents misaligned. Beneficiary designations from before a marriage or divorce can result in assets passing to the wrong people. An estate plan that doesn't reflect a recent inheritance might miss opportunities to minimize estate taxes.

- You miss time-sensitive opportunities. Many planning strategies have deadlines. Tax elections must be made within specific windows. Certain account rollovers have time limits. Delaying your plan update can mean permanently losing valuable strategies.

- You create confusion and stress. Operating without a clear, updated plan means making financial decisions without a framework. Should you invest the business sale proceeds conservatively or aggressively? Should you retire now or keep working? Without an updated plan, every decision becomes a source of uncertainty.

When to Work with a Professional

Some life events are complex enough that professional guidance isn't optional—it's essential.

- Business sale proceeds over $1 million: The tax planning, investment strategy design, and wealth preservation strategies required are too consequential to handle without expert guidance.

- Sudden wealth from inheritance: Especially if you've inherited complex assets such as businesses, real estate, or large retirement accounts, professional planning prevents costly mistakes.

- Marriage or divorce: The legal, tax, and estate planning implications require coordinated advice from financial planners, CPAs, and attorneys.

- Approaching retirement within 5 years: The transition from accumulation to distribution is when mistakes are most costly. Professional guidance during this window is worth the investment.

Your Action Plan

If you've experienced a major life event in the past 12 months:

- Schedule a comprehensive plan review within 30 days. Don't wait until your next annual review. Life events demand immediate attention.

- Bring documentation. If you sold a business, bring the purchase agreement and tax documents. If you inherited assets, bring estate documents and account statements. Your planner needs complete information.

- Update beneficiaries immediately. Even before completing a full plan update, update beneficiary designations on all accounts. This is low-hanging fruit that prevents catastrophic errors.

- Don't make major financial decisions until your plan is updated. If you just sold your business and receive calls from advisors suggesting investment strategies, wait. Get your plan updated first, then make decisions aligned with that plan.

Big life events create both opportunities and risks. An updated financial plan helps you capitalize on the opportunities while avoiding the risks. The cost of updating is measured in hours and planning fees. The cost of not updating can be measured in hundreds of thousands of dollars in missed opportunities, unnecessary taxes, and suboptimal decisions.

Your financial plan is a living document, not a one-time project. When life changes dramatically, your plan must change with it.

This article is for educational purposes only and should not be construed as specific financial, tax, or legal advice. Consult with qualified professionals regarding your individual circumstances.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.