You're scrolling through retirement articles online, and every one gives you a different number. Some say $1 million is enough. Others insist you need $3 million. A few suggest $5 million or more. Meanwhile, your 401(k) balance feels nowhere close to any of these targets, and you're wondering if you'll ever get there.

The truth? There's no universal magic number. Retirement isn't about hitting a specific dollar amount. It's about having enough to support the lifestyle you want without running out of money.

The answer depends on your spending, your timeline, your other income sources, and your willingness to adjust along the way. But there are frameworks to help you estimate what you'll need and build a plan to get there.

Here's how to figure out your number.

The Problem with Generic Retirement Targets

Financial media loves round numbers: "$1 million to retire comfortably!" or "The average American needs $1.9 million!"

These headlines are useless.

Someone spending $40,000 per year in retirement has completely different needs than someone spending $120,000. Geography matters: $80,000 goes much further in Raleigh than in San Francisco. Health care costs, longevity, pensions, Social Security, and inheritance plans all dramatically shift the calculation.

A better approach starts with your spending and works backward.

The 4% Rule: A Starting Point

The most well-known retirement guideline is the 4% rule, which suggests you can withdraw 4% of your portfolio in the first year of retirement, then adjust that amount annually for inflation, with a high probability your money will last 30 years.

Example:

- You have $1 million saved

- 4% of $1 million = $40,000/year

- You withdraw $40,000 in year one, then adjust for inflation each year

This rule comes from the Trinity Study, which analyzed historical stock and bond returns and found that a 4% withdrawal rate had a 95% success rate over 30-year periods.

The 4% rule in reverse:

If you know how much income you need, multiply by 25 to estimate your target portfolio size.

- Need $60,000/year? $60,000 x 25 = $1.5 million

- Need $80,000/year? $80,000 x 25 = $2 million

- Need $120,000/year? $120,000 x 25 = $3 million

The Limits of the 4% Rule

The 4% rule is useful, but it's not perfect. Critics point out several limitations:

1. It Assumes 30-Year Retirements

If you retire at 55, you might need your money to last 35-40 years. A 4% withdrawal rate may be too aggressive. A 3-3.5% rate might be safer, which means you'd need a larger nest egg.

2. Sequence of Returns Risk

If you retire right before a major market crash (like 2008 or early 2020), withdrawing 4% annually while your portfolio is down can deplete your savings faster. Early losses compound negatively when you're also taking withdrawals.

3. It Ignores Other Income

Most retirees have Social Security, pensions, rental income, or part-time work. The 4% rule assumes your portfolio is your only income source, which is rarely true.

4. Spending Isn't Static

Retirees often spend more in early retirement (travel, hobbies, new experiences) and less in later years. The 4% rule assumes constant inflation-adjusted spending, which doesn't reflect reality.

Still, as a starting point for estimating your target, the 4% rule works.

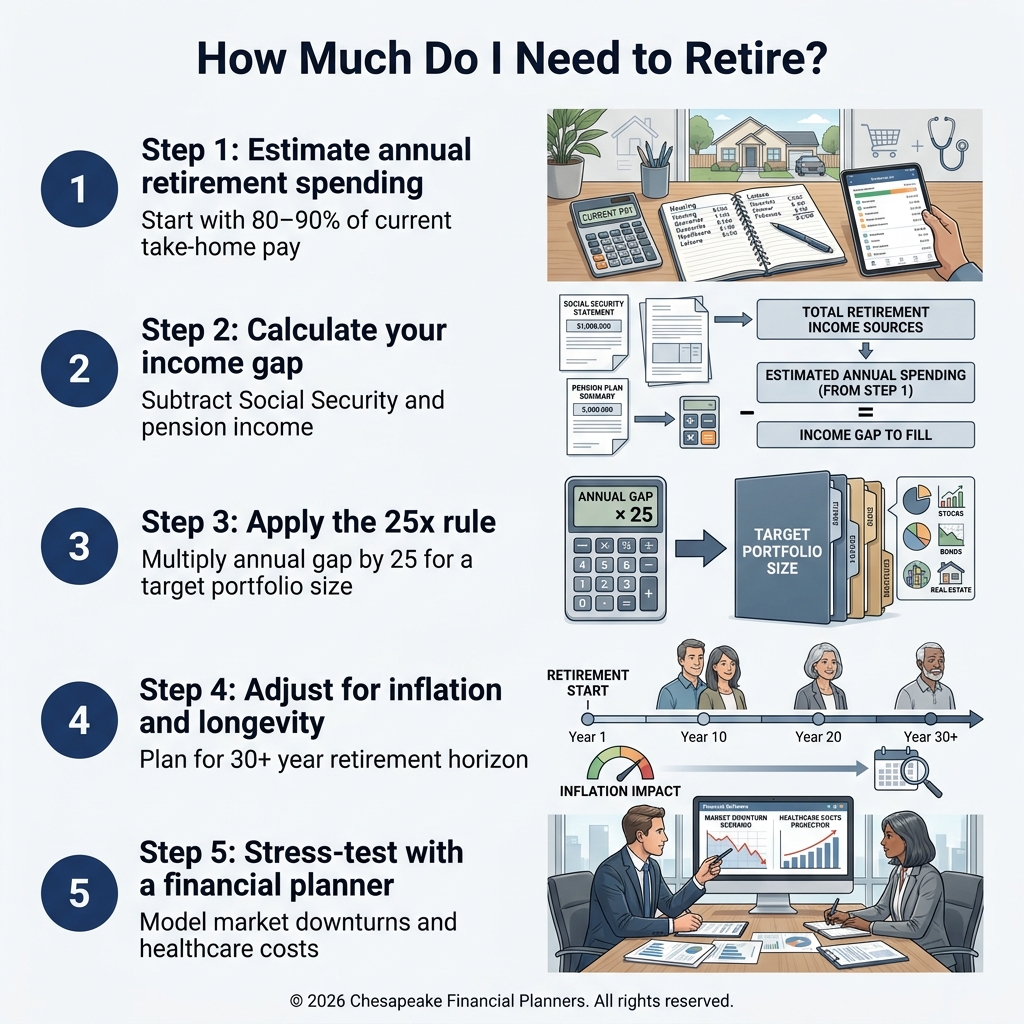

Step 1: Calculate Your Retirement Spending

Most retirement calculators start with your current income and assume you'll need 70-80% of it in retirement. This is often wrong.

Instead, project your actual retirement expenses:

Fixed Costs

- Housing (mortgage, rent, property taxes, insurance, maintenance)

- Utilities

- Insurance (health, life, auto, home, long-term care)

- Property taxes

- HOA fees

Variable Costs

- Groceries and dining

- Travel and entertainment

- Hobbies

- Gifts and charitable giving

- Clothing

One-Time and Irregular Costs

- Home repairs or renovations

- New vehicles

- Healthcare expenses not covered by insurance

Be realistic. If you're planning to travel extensively, buy a vacation home, or support adult children, factor that in. If your mortgage will be paid off, exclude it.

Common estimate: Many retirees find they spend 80-90% of their pre-retirement income in the early years, dropping to 70-80% in later years as spending naturally declines.

Step 2: Subtract Guaranteed Income

Most people have income sources beyond their investment portfolio:

Social Security

Check your estimated benefit at SSA.gov. The average benefit is about $1,900/month ($22,800/year), but high earners can receive up to $4,873/month ($58,476/year) if they delay until age 70.

Pensions

If you have a defined benefit pension, factor in the monthly or annual payout.

Rental Income

If you own rental properties, include net income after expenses.

Part-Time Work

Many retirees work part-time in early retirement, either for income or engagement. If that's your plan, include it.

Example Calculation:

- Annual retirement spending: $90,000

- Social Security (two people): $50,000

- Pension: $15,000

- Total guaranteed income: $65,000

- Portfolio needs to cover: $90,000 – $65,000 = $25,000/year

Using the 4% rule: $25,000 x 25 = $625,000 needed

Without Social Security or a pension, you'd need $90,000 x 25 = $2.25 million – a massive difference.

Step 3: Factor in Healthcare Costs

Healthcare is one of the largest and least predictable retirement expenses.

Before Medicare (Age 65)

If you retire before 65, you'll need to cover health insurance yourself. Options include:

- COBRA (expensive but comprehensive)

- ACA marketplace plans (potentially subsidized)

- Spouse's employer plan

Budget $700-1,500/month per person, depending on your location and health.

After Medicare

Medicare covers much (but not all) of your healthcare costs. Expect to pay:

- Medicare Part B premium: ~$185/month (higher for high earners due to IRMAA surcharges)

- Medigap or Medicare Advantage premiums

- Part D prescription drug coverage

- Out-of-pocket costs

Fidelity estimates a 65-year-old couple will need about $315,000 over retirement to cover healthcare costs not paid by Medicare. That's roughly $12,000-15,000/year.

Long-Term Care

Medicare does not cover long-term care (nursing homes, assisted living, in-home care). The average cost of a nursing home is $100,000+/year.

Consider:

- Self-funding (having extra savings)

- Long-term care insurance

- Hybrid life insurance policies with LTC riders

Step 4: Adjust for Longevity

How long will you need your money to last?

Life Expectancy

- A 65-year-old man has a 50% chance of living to age 84 and a 25% chance of reaching 92

- A 65-year-old woman has a 50% chance of living to age 87 and a 25% chance of reaching 94

- For a 65-year-old couple, there's a 50% chance one spouse lives to 90+

Planning Horizon

Most advisors suggest planning for at least 30 years, often 35-40, especially if you or your spouse have longevity in your family history or retire early.

If you're retiring at 60, plan for your money to last until at least 95. If you're retiring at 67, plan until at least 97.

Step 5: Build in Flexibility

Retirement isn't a set-it-and-forget-it calculation. Markets fluctuate. Spending changes. Life happens.

Dynamic Withdrawal Strategies

Instead of rigidly withdrawing 4% annually, consider:

- Variable withdrawals: Spend more in strong market years, less in weak ones

- Guardrails approach: Set upper and lower spending limits based on portfolio performance

- Bucket strategy: Keep 2-3 years of expenses in cash, so you're not forced to sell stocks in a downturn

Part-Time Work

Working even part-time for a few years in early retirement significantly reduces the burden on your portfolio.

Downsizing

Selling a large home and moving to a smaller, lower-cost property can free up hundreds of thousands in equity and reduce ongoing expenses.

Common Retirement Number Benchmarks

While your situation is unique, here are some general benchmarks:

- By Age 30: 1x your annual salary saved

- By Age 40: 3x your annual salary

- By Age 50: 6x your annual salary

- By Age 60: 8x your annual salary

- By Age 67: 10x your annual salary

These are guidelines, not mandates. Someone with a pension or rental income needs less. Someone planning to retire early needs more.

What If You're Behind?

If you're looking at your target number and feeling discouraged, you have options:

1. Increase Savings Rate

Even small increases compound significantly. Going from 10% to 15% savings can add hundreds of thousands over 20 years.

2. Delay Retirement

Working even 2-3 extra years dramatically improves your situation: more savings time, less portfolio draw, higher Social Security benefits.

3. Optimize Social Security

Delaying Social Security from age 62 to 70 increases your benefit by about 77%. For many, this is the best "investment" available.

4. Reduce Retirement Spending

If you need $100,000/year, you need $2.5 million. If you can live comfortably on $70,000/year, you need $1.75 million. Lifestyle adjustments matter.

The Bottom Line

There's no single retirement number. Your target depends on your spending, other income sources, health, longevity, and risk tolerance.

Start with the 4% rule to get a rough estimate, then refine based on your situation. Work with a financial planner to model different scenarios, stress-test your plan, and build in flexibility.

Retirement planning isn't about hitting a perfect number. It's about building a plan that adapts as life unfolds.

This information is for educational purposes only and should not be considered financial or investment advice. Retirement planning involves numerous variables and assumptions that may not reflect actual future outcomes. Consult with a qualified financial advisor to create a personalized retirement plan based on your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.