Key questions to explore together:

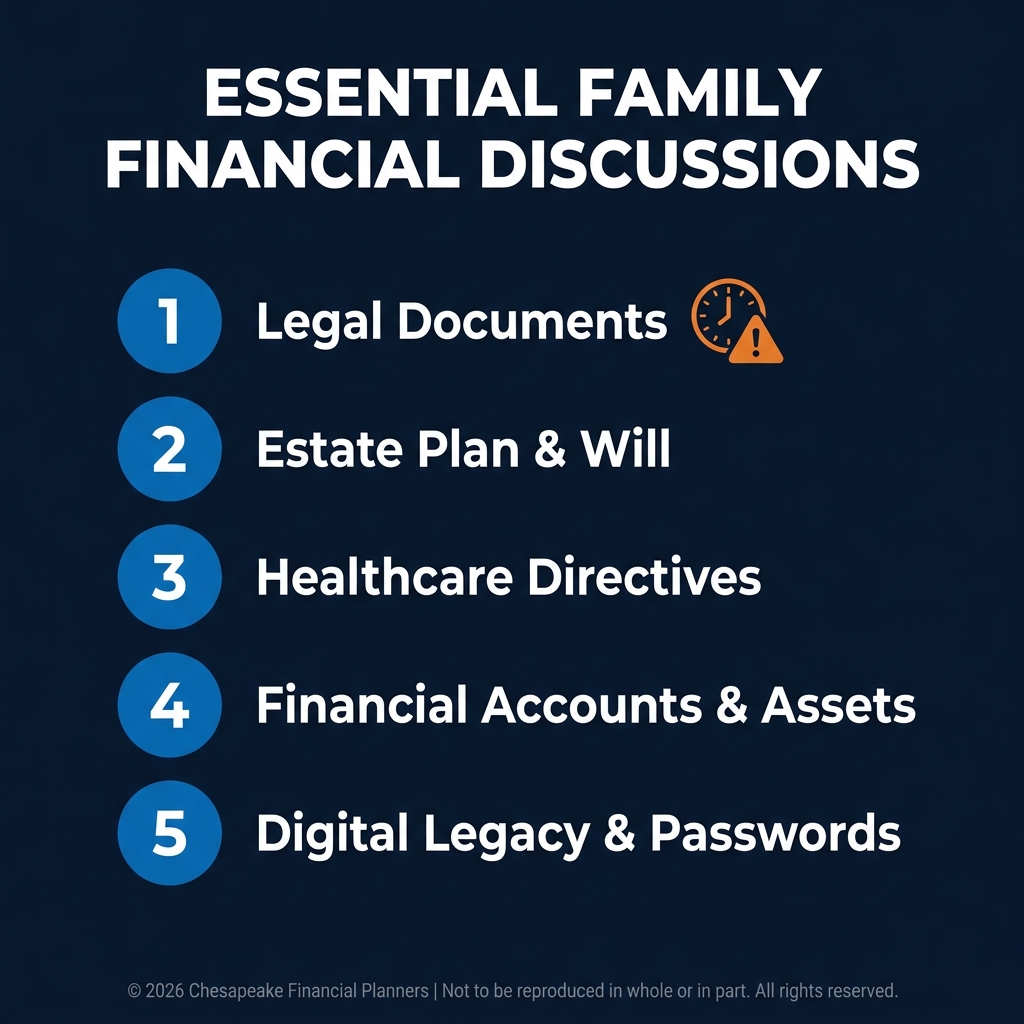

- What legal documents do they have in place? This includes powers of attorney (both financial and healthcare), living wills, and estate planning documents. If these don't exist, making them a priority protects everyone.

- Where do their finances stand? You need a realistic picture of their income sources (Social Security, pensions, investment accounts), assets, debts, and monthly expenses. This baseline helps you understand what resources exist and what gaps need filling.

- What insurance coverage do they have? Review Medicare coverage, supplemental insurance, and whether they have long-term care insurance. Many people don't realize that Medicare doesn't cover custodial long-term care—the kind most seniors eventually need.

- What are their wishes if they need care? Would they prefer to age in place with home health support, move in with family, or transition to assisted living or a nursing home? Understanding preferences now helps you plan for realistic costs.

Understanding the Real Costs of Caring

The financial burden of aging parent care extends beyond direct expenses. You need to account for both the visible costs and the hidden ones.

Direct costs

- Housing modifications for aging in place

- Home health aides or adult day programs

- Assisted living or memory care facilities

- Medical expenses not covered by insurance

- Transportation to appointments

- Medications or medical equipment

Hidden costs

- Your own lost wages if you reduce work hours or leave your job

- The impact on your Social Security benefits from reduced earnings years

- Retirement savings you can't contribute during caregiving years

- The potential need to delay your own retirement

- The physical and mental health toll of caregiving stress

The average family caregiver spends about $7,200 per year out of pocket on caregiving expenses, on top of the time commitment. For many women already facing a retirement savings gap, absorbing these costs while maintaining their own financial health requires deliberate planning.

Create a Coordinated Family Plan

Caring for aging parents works best as a team effort. If your parents have multiple adult children, have an honest family meeting about roles, responsibilities, and financial contributions.

Discuss who can provide what type of support. One sibling might be better positioned to contribute financially while another can provide hands-on care. Another might handle the administrative work—coordinating appointments, managing insurance claims, and overseeing legal documents. Clear roles reduce resentment and ensure all the work doesn't fall on one person (which too often happens to daughters).

Consider how parent care costs will be shared. Will everyone contribute proportionally to their income? Will those who can't contribute financially provide more hands-on care? Will you use your parents' assets first before children contribute? Document these agreements to avoid future conflicts.

Protect Your Own Financial Security

Supporting aging parents shouldn't come at the cost of your own retirement security. You can't borrow for retirement the way your kids can borrow for college.

Set boundaries that protect your future:

Establish a realistic budget for what you can contribute financially without compromising your own retirement savings. Keep contributing to your retirement accounts even while helping parents—your future self depends on these years of compound growth.

If you need to reduce work hours for caregiving, understand the long-term impact on your Social Security benefits and retirement accounts. Can you afford to make up those lost years, or are there alternatives like paid caregiving help or shared family responsibilities that preserve your earnings?

Avoid depleting your emergency fund or taking on debt to fund parent care. These strategies might solve an immediate problem but create bigger financial vulnerabilities for your own future.

Explore Available Resources and Support

Many families don't realize the resources available to help with aging parent care costs.

Government programs like Medicaid cover long-term care for those who qualify based on income and assets. Veterans Aid and Attendance benefits may be available if your parent served in the military. Some states offer Medicaid waiver programs that help seniors afford to age at home instead of entering nursing facilities.

Tax benefits can offset some costs. If you're providing more than half your parent's support, you may be able to claim them as a dependent. Medical expense deductions may apply if costs exceed 7.5% of your adjusted gross income. A Dependent Care FSA might help if your parent lives with you and you're paying for care while you work.

Community resources often provide support services at lower costs than private options—adult day programs, meal delivery services, respite care to give family caregivers breaks, and transportation assistance for medical appointments.

When to Bring in Professional Help

Navigating the financial complexities of aging parent care while protecting your own retirement requires specialized expertise. A financial advisor who understands eldercare planning can help you create a coordinated strategy that honors your parents while safeguarding your future.

- We can help you model different care scenarios and their costs

- Coordinate with eldercare attorneys on legal documents

- Evaluate whether long-term care insurance makes sense at this stage

- Create a sustainable plan that protects your retirement timeline

- Identify tax strategies and government programs that reduce your family's burden

You don't have to choose between supporting your parents and securing your own future. With the right planning, you can honor both.

For educational purposes only. This is not personalized financial, tax, or legal advice. Consult with your financial advisor, tax professional, and eldercare attorney for guidance specific to your family's situation.

Past performance does not guarantee future results. All investing involves risk, including potential loss of principal.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.