Losing your spouse is one of life's most devastating experiences. Grief is overwhelming, and the last thing you want to think about is paperwork, accounts, and financial decisions.

But financial matters won't wait, and making informed decisions during this painful time protects your future security. You don't need to tackle everything immediately, but you do need to know what's urgent and what can wait.

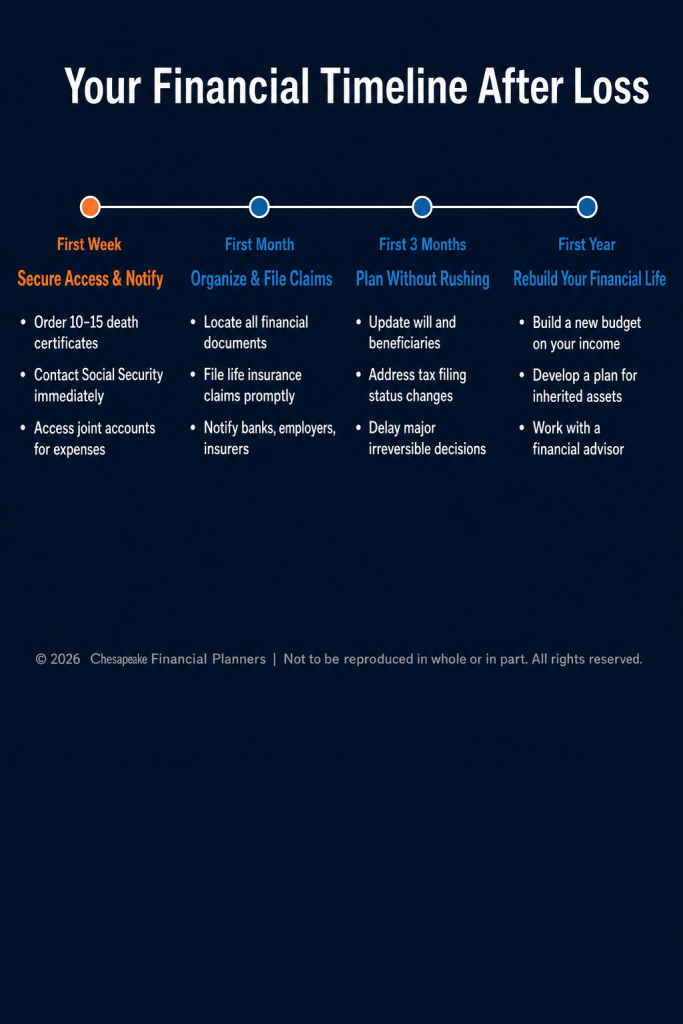

The First Week: Immediate Priorities

Take Care of Immediate Needs

Before anything else, make sure you have access to money for immediate expenses. If you have joint checking accounts, you should still have access. If not, contact your bank about accessing funds.

You'll need cash for:

- Funeral and burial expenses

- Travel for family members

- Immediate household bills

- Daily living expenses

Don't make any major financial decisions this week. Your only goal is ensuring you can cover necessary expenses.

Order Multiple Death Certificates

You'll need official death certificates for insurance claims, account transfers, Social Security, pension benefits, and other institutions. Order at least 10-15 certified copies through the funeral home or vital records office.

These take time to arrive, so request them early. You can always order more later, but delays cost time when you're settling accounts.

Notify Social Security

Contact Social Security within days of your spouse's death. If your spouse received benefits, those must stop. You may qualify for survivor benefits, which can provide important income.

The First Month: Essential Actions

Locate Important Documents

Find and organize:

- Life insurance policies

- Retirement account statements

- Bank and brokerage account information

- Property deeds and titles

- Vehicle titles

- Estate planning documents (will, trust, power of attorney)

- Tax returns from the past three years

- Mortgage and loan documents

- Credit card statements

- Passwords and online account information

Create a master list with account numbers, institutions, and approximate values. This becomes your financial roadmap.

Notify Financial Institutions

Contact:

- Life insurance companies to initiate claims

- Employers about pension benefits, 401(k)s, and any death benefits

- Banks where you held joint or individual accounts

- Credit card companies

- Investment firms

- Mortgage lender

- Insurance companies (home, auto, health)

You don't need to transfer or close everything immediately, but institutions need to know about the death.

File Life Insurance Claims

Don't delay on this. Life insurance proceeds can take weeks or months to process, and you'll likely need this money.

Submit claims with certified death certificates to every policy. If you're unsure whether your spouse had coverage, check with:

- Current and former employers

- Professional associations

- Credit card companies (some provide automatic coverage)

- Mortgage lenders (some loans include life insurance)

Assess Your Income Situation

Calculate what income you'll have going forward:

- Your employment income

- Social Security survivor benefits

- Pension payments (survivor benefits, if any)

- Investment income

- Rental income

- Other sources

Compare this to your household expenses. Understanding the gap helps you make informed decisions about life insurance proceeds and other assets.

The First Three Months: Making a Plan

Don't Rush Major Decisions

Financial advisors often recommend waiting 6-12 months before making irreversible decisions like:

- Selling your home

- Moving to a new area

- Making large purchases

- Giving away significant assets

- Remarrying

Your judgment is impaired by grief. Decisions made in crisis mode often turn out poorly. What feels right now might not feel right in six months.

Update Your Estate Planning

You need new documents reflecting your changed circumstances:

- Update your will

- Revise beneficiaries on retirement accounts and life insurance

- Update powers of attorney and healthcare directives

- Review trust arrangements if applicable

- Update your own life insurance beneficiaries

If you have minor children, these updates become even more urgent to ensure their care and financial security.

Address Tax Implications

Your tax situation has changed significantly:

File a final joint return for the year of your spouse's death. You get married filing jointly status one last time.

Understand your new filing status: You might qualify for qualifying widow(er) with dependent child status for two years after your spouse's death, which provides better tax rates than filing single.

Consider inherited retirement accounts: Rules for inherited IRAs and 401(k)s are complex. Don't make withdrawal decisions without understanding tax consequences.

Review tax withholding: If you're working, your tax situation is now different. Adjust your W-4 accordingly.

Consider hiring a CPA or tax professional this year. The complexity of your situation warrants expert help.

Evaluate Your Housing Situation

For now, stay where you are unless circumstances force a move. But start thinking about whether your current home makes sense long-term:

- Can you afford the mortgage and maintenance on one income?

- Is the house too large for your current needs?

- Does staying connected to this place help or hurt your healing?

- What would it cost to downsize or relocate?

You don't need to decide yet. Just gather information so you can make an informed choice when you're ready.

The First Year: Rebuilding Your Financial Life

Close or Transfer Joint Accounts

Eventually you'll need to:

- Remove your spouse from joint bank accounts or close them and open new ones

- Transfer joint investment accounts to your name

- Retitle property and vehicle ownership

- Update home and auto insurance policies

This process takes time and energy. Tackle one institution at a time rather than trying to do everything at once.

Create Your Own Budget

Your expenses have changed. Some costs decrease (possibly food, healthcare, life insurance), while others might increase (home maintenance you previously shared).

Build a new budget based on your current income and actual expenses. This shows you whether you're living within your means or need to make adjustments.

Develop an Investment Strategy

If you received life insurance proceeds or inherited retirement accounts, you need a plan for this money:

Emergency reserves: Keep 6-12 months of expenses in accessible savings.

Pay off high-interest debt: Credit cards and personal loans should generally be eliminated.

Invest the rest appropriately: Based on your timeline, risk tolerance, and income needs.

Don't let guilt drive decisions: Some widows feel obligated to "preserve" life insurance money without touching it. That money is meant to support you. Use it wisely, but don't feel wrong about using it for its intended purpose.

Build Your Knowledge and Confidence

If your spouse handled finances, you might feel overwhelmed by suddenly managing everything alone. That's normal.

Consider:

- Taking a personal finance class

- Working with a financial advisor

- Joining a widow support group where others share experiences and advice

- Reading books about financial recovery after loss

Knowledge builds confidence, and confidence helps you make better decisions.

Finding Help When You Need It

You don't have to do this alone. Consider professional help from:

Financial advisors who can help with investment strategy, budgeting, and long-term planning.

CPAs who can navigate the tax complexity of your situation.

Estate attorneys who can help settle your spouse's estate and update your own planning.

Grief counselors who help you process loss emotionally so you can make better financial decisions.

Moving Forward

Financial recovery after loss takes time, just like emotional recovery. Be patient with yourself as you learn new skills and take on responsibilities you might not have expected.

You're stronger than you know. The fact that you're reading this and taking steps to understand your financial situation shows you're moving forward, even when forward feels impossibly difficult.

Take it one day, one decision, one step at a time. You will get through this.

This material is for educational purposes only. For personalized financial guidance during life transitions, please consult with a qualified financial professional.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.