You check your portfolio and see it's down 15% in a month. Your gut tells you to sell everything before it gets worse. Or maybe you see a hot stock that's doubled in the past three months, and you're convinced it's going to keep soaring.

These are the moments when investment biases cost you the most money.

Behavioral finance research shows that the average investor significantly underperforms the market—not because they pick bad investments, but because they make emotional, biased decisions at exactly the wrong times.

The difference between a successful long-term investor and everyone else isn't intelligence, access to information, or market timing skill. It's the ability to recognize and overcome the psychological biases that sabotage wealth-building.

Here are the most common investment biases and how to beat them.

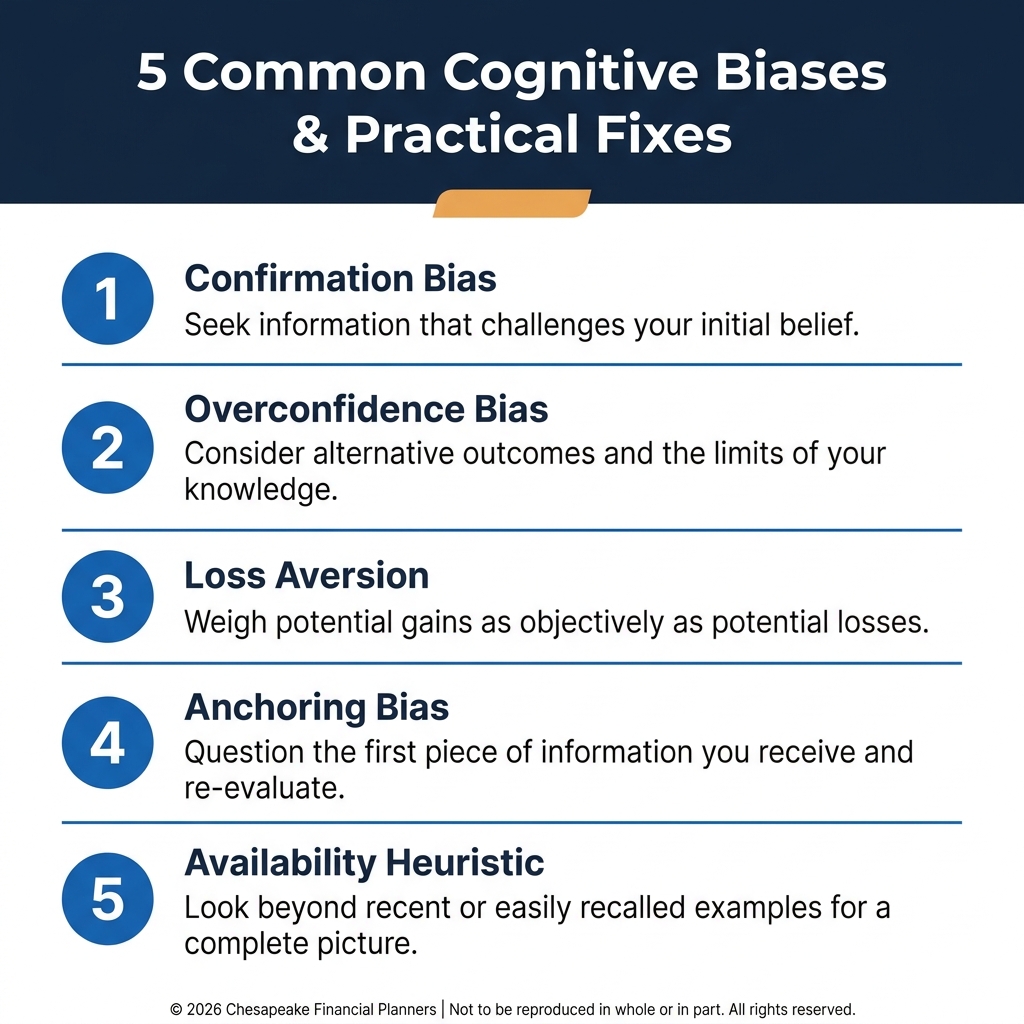

1. Loss Aversion: Feeling Losses More Than Gains

The Bias:

Research shows people feel the pain of losing $100 about twice as intensely as the pleasure of gaining $100. This asymmetry causes investors to make irrational decisions to avoid losses—even when taking those losses would be the smart move.

How It Hurts You:

- Holding losing investments too long, hoping they'll "come back" instead of cutting losses

- Selling winners too early to "lock in gains" before they've fully appreciated

- Being too conservative with investments, missing out on growth because you're terrified of short-term losses

Real-World Example:

You bought a stock at $50. It drops to $30. Instead of reassessing whether it's still a good investment, you hold it because selling would mean "admitting" you lost money. Meanwhile, you sell a stock that's up 20% because you're afraid it will drop, missing out on further gains.

How to Overcome It:

- Focus on probabilities, not outcomes. A good decision can still result in a loss. Judge your process, not individual results.

- Set rules in advance. Decide beforehand when you'll sell (e.g., trailing stop-loss orders, rebalancing schedule) so emotion doesn't drive the decision.

- Think in portfolios, not positions. One losing stock doesn't matter if your overall portfolio is performing well.

2. Recency Bias: Overweighting Recent Events

The Bias:

We give far too much importance to recent experiences and assume current trends will continue indefinitely.

How It Hurts You:

- Buying stocks or sectors after they've surged, assuming the rally will continue (buying high)

- Selling stocks after a crash, assuming the decline will continue (selling low)

- Abandoning diversification because "international stocks haven't performed well recently"

Real-World Example:

Tech stocks soared from 2017-2021. Investors piled in during 2020-2021, assuming the trend would last forever. Then came 2022, and tech dropped 30-40%. Those who bought at the peak locked in massive losses.

How to Overcome It:

- Rebalance systematically. Sell winners (which have probably surged recently) and buy losers (which have probably declined recently). This forces you to do the opposite of what recency bias suggests.

- Study market history. Every asset class has cycles. What's hot now won't be hot forever.

- Stick to your allocation. If your plan says 20% international stocks, don't abandon that just because U.S. stocks outperformed for a decade.

3. Confirmation Bias: Seeking Information That Confirms Your Beliefs

The Bias:

We actively seek out information that supports what we already believe and ignore or dismiss contradictory information.

How It Hurts You:

- Reading only bullish articles about stocks you own, ignoring warning signs

- Dismissing negative news about your favorite companies as "fake news" or "market manipulation"

- Surrounding yourself with like-minded investors who reinforce your existing views

Real-World Example:

You're convinced a particular stock is undervalued. You read every article praising the company, but when a critical analyst report comes out, you dismiss it as biased. You double down on the stock, ignoring mounting evidence that your thesis is wrong.

How to Overcome It:

- Actively seek opposing views. For every bullish article you read, find a bearish one. Steel-man the opposing argument.

- Assign a "devil's advocate." If you're considering a big investment, ask someone you trust to argue against it.

- Use index funds. You can't cherry-pick information if you own the entire market.

4. Overconfidence Bias: Believing You're Better Than You Are

The Bias:

Most people believe they're above-average investors, just like most people believe they're above-average drivers. Studies show that 80% of investors think they'll beat the market—but by definition, only about 50% can.

How It Hurts You:

- Trading too frequently, thinking you can time the market or pick winners

- Taking on too much risk because you underestimate the possibility of losses

- Ignoring professional advice because "you know better"

Real-World Example:

You pick 5 stocks that happen to do well. You conclude you're a stock-picking genius and allocate more money to individual stocks, ignoring the role luck played in your success. Over time, your picks underperform, but by then you've missed out on years of index fund gains.

How to Overcome It:

- Track your actual performance. Calculate your total return (including all trades, fees, and taxes) and compare it to a simple index fund. Most people discover they underperform.

- Recognize the role of luck. Short-term outperformance is often random noise, not skill.

- Default to passive investing. If you want to stock-pick, limit it to 5-10% of your portfolio. Keep the bulk in diversified index funds.

5. Herd Mentality: Following the Crowd

The Bias:

Humans are social creatures. We feel safer doing what everyone else is doing, even when "everyone else" is making a terrible decision.

How It Hurts You:

- Buying stocks everyone's talking about at parties (usually near the peak)

- Panic-selling when the media screams about a crash

- Investing in whatever asset class is "hot" (tech stocks, crypto, real estate) without understanding it

Real-World Example:

In early 2021, GameStop and AMC surged due to a Reddit-fueled short squeeze. Millions of investors piled in at $300+ per share because "everyone was doing it." Most lost significant money when the stocks crashed back to reality.

How to Overcome It:

- Be contrarian (carefully). When everyone is euphoric, be cautious. When everyone is panicking, look for opportunities.

- Ignore FOMO (fear of missing out). Every bull market has a story about someone who got rich. You only hear about the winners, not the thousands who lost money trying to replicate their success.

- Stick to your plan. If your investment policy says "60% stocks, 40% bonds," don't abandon that because your neighbor is bragging about crypto gains.

6. Anchoring Bias: Fixating on Irrelevant Reference Points

The Bias:

We latch onto the first piece of information we encounter (the "anchor") and use it as a reference point for all future decisions, even when it's irrelevant.

How It Hurts You:

- Refusing to sell a stock until it "gets back to" the price you paid for it

- Buying a stock because it's "down 50% from its high" without assessing its actual value

- Setting mental price targets based on arbitrary numbers instead of fundamentals

Real-World Example:

You bought a stock at $100. It drops to $60. You refuse to sell because you're anchored to the $100 price, waiting for it to "come back." Meanwhile, the stock continues declining to $40, and you've missed the opportunity to cut your loss at $60.

How to Overcome It:

- Evaluate investments based on current value, not purchase price. Ask: "If I didn't own this stock, would I buy it today at this price?" If the answer is no, sell.

- Set price targets based on fundamentals, not history. A stock being "down 50% from its high" doesn't make it a bargain if the business is deteriorating.

- Use stop-loss orders. Decide in advance when you'll sell, removing emotion from the decision.

7. Hindsight Bias: Believing You "Knew It All Along"

The Bias:

After an event occurs, we convince ourselves we "knew it would happen," even though we didn't.

How It Hurts You:

- Overestimating your predictive ability, leading to overconfidence in future predictions

- Failing to learn from mistakes because you rewrite history to make yourself look smarter

- Taking excessive risk because you believe you can foresee outcomes

Real-World Example:

The market crashes in 2022. You tell yourself (and others), "I knew that was coming," even though you didn't sell beforehand. This reinforces the false belief that you can predict crashes, leading you to make risky bets in the future.

How to Overcome It:

- Keep an investment journal. Write down your reasoning for every investment decision before you make it. Review it later to see how accurate your predictions actually were.

- Accept uncertainty. No one consistently predicts market movements. Successful investing is about managing risk, not predicting the future.

- Focus on process over outcomes. Judge decisions based on the information available at the time, not how they turned out in hindsight.

8. Sunk Cost Fallacy: Throwing Good Money After Bad

The Bias:

We continue investing time, money, or energy into something because we've already invested so much, even when it's clearly not working.

How It Hurts You:

- Holding losing investments because "I've already lost so much"

- Adding more money to a declining stock to "average down," hoping to recoup losses

- Staying in bad investments because "I've held it for 5 years—I can't sell now"

Real-World Example:

You bought a stock at $80, and it's now $40. Instead of cutting your loss, you buy more shares to "lower your average cost" to $60. The stock continues to decline to $20, and you've now lost even more money.

How to Overcome It:

- Ignore sunk costs. Money you've already lost is gone. Focus on what the best decision is right now with the information you have.

- Ask the right question: "If I didn't already own this, would I buy it today?" If no, sell.

- Accept losses as tuition. Every investor makes bad calls. Learn from them and move on.

Building a Bias-Resistant Investment Strategy

1. Create an Investment Policy Statement (IPS)

Write down your goals, risk tolerance, asset allocation, and rebalancing plan. When emotions tempt you to deviate, refer back to your IPS.

2. Automate Everything

Set up automatic contributions, automatic rebalancing, and systematic investment plans. Remove the opportunity for biased decision-making.

3. Limit Your Exposure to Market News

Checking your portfolio daily and consuming financial media non-stop amplifies emotional reactions. Check quarterly or annually instead.

4. Work with an Advisor (If Needed)

A good advisor acts as a behavioral coach, preventing you from making emotionally driven mistakes during volatile markets.

5. Diversify Broadly

A well-diversified portfolio reduces the temptation to make tactical bets based on biases. You can't chase hot stocks if you own the entire market.

The Bottom Line

Investment biases aren't a sign of weakness—they're hardwired into human psychology. Even professional investors struggle with them.

The difference between successful investors and everyone else isn't the absence of biases—it's the awareness of them and the systems in place to counteract them.

Action steps:

- Recognize which biases affect you most (review the list and identify patterns in your past decisions)

- Create rules and systems that remove emotion from investing (asset allocation, rebalancing schedule, stop-losses)

- Automate as much as possible

- Focus on process, not outcomes

- Stay humble—the market humbles everyone eventually

The investors who build lasting wealth aren't the smartest or the ones with the best information. They're the ones who recognize their biases, build systems to overcome them, and stick to the plan when everyone else is panicking.

This information is for educational purposes only and should not be considered investment or psychological advice. All investing involves risk, including the potential loss of principal. Behavioral biases affect all investors differently. Consider consulting with a qualified financial advisor to develop an investment strategy suited to your situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.