You've received a windfall or inheritance, and you're trying to understand what you'll owe in taxes. The answer is frustrating: it depends. Different types of windfalls carry vastly different tax treatment, and the specifics of your situation determine what you'll actually keep after taxes.

Here's what you need to know about taxes on windfalls and inheritances.

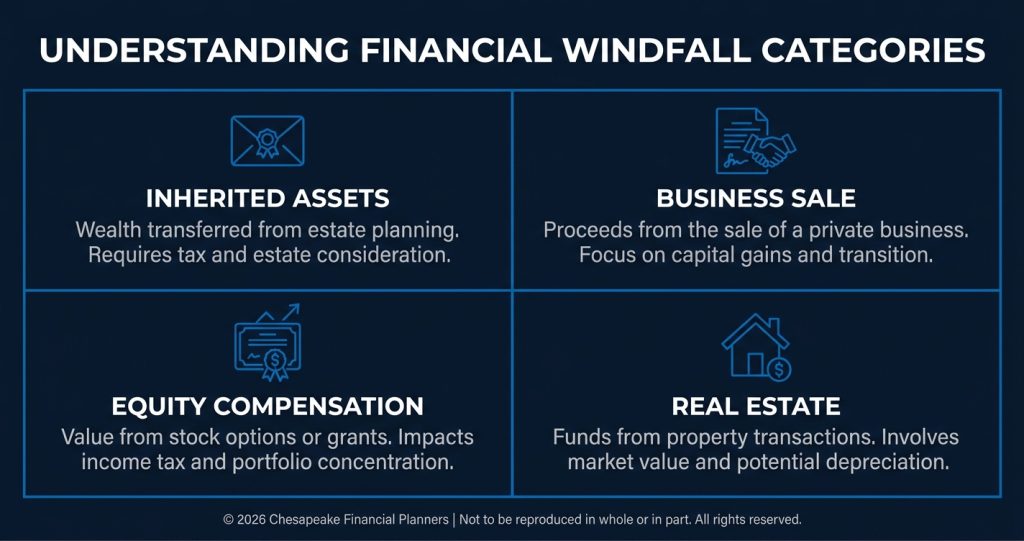

Inheritances: Generally Tax-Free (With Important Exceptions)

Most inheritances are not taxable to beneficiaries. You don't pay federal income tax simply because you inherited money or property. This surprises many people who assume inheritance is taxable income.

However, several important exceptions can create tax obligations:

Estate taxes

May apply to very large estates—those exceeding $15 million per person in 2026. But estate taxes are paid by the estate itself before assets are distributed to beneficiaries, not by you as the recipient.

State inheritance or estate taxes

Exist in some states with lower thresholds than federal limits. A handful of states impose inheritance taxes based on your relationship to the deceased. Maryland, for example, has both an estate tax and an inheritance tax with different exemptions and rates.

Inherited retirement accounts

Are pre-tax money that will be taxed as ordinary income when you take distributions. If you inherit a traditional IRA or 401(k), you'll owe taxes on every dollar you withdraw—and under current law, most non-spouse beneficiaries must empty these accounts within 10 years.

Income generated by inherited assets

Is taxable to you. If you inherit investment accounts that pay dividends, rental property that generates income, or a business that produces profits, that income is taxable even though the inheritance itself wasn't.

Business Sales: Capital Gains Taxation

When you sell a business, you'll generally owe capital gains taxes on your profit—the difference between what you sell it for and your adjusted basis in the business.

Long-term capital gains rates (for assets held more than one year) are typically 0%, 15%, or 20% at the federal level, depending on your income. These rates are significantly lower than ordinary income tax rates, which can reach 37%.

However, additional taxes may apply:

Net investment income tax

Adds 3.8% tax on net investment income (including capital gains, dividends, interest, and some rental income) if your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). It applies to the lesser of (1) your net investment income or (2) the amount your MAGI exceeds the threshold.

State capital gains taxes

Vary widely. Some states have no income tax, while others tax capital gains as ordinary income at rates up to 13.3% (California). (High earners may also face an additional 1% CA mental health surtax on income over $1M.)

Depreciation recapture

May apply if you've claimed depreciation deductions on business assets. These gains can be taxed at up to 25% instead of the more favorable long-term capital gains rates.

The structure of your business sale—asset sale vs. stock sale, earnout provisions, consulting agreements—significantly affects tax treatment. Engage a CPA before finalizing sale terms to optimize tax efficiency.

Stock Options and RSU Exercises: Ordinary Income

When you exercise stock options or restricted stock units vest, you typically owe ordinary income tax on the value you receive.

Non-qualified stock options (NSOs)

Create ordinary income equal to the difference between the exercise price and fair market value. If you exercise options to buy shares at $10 when they're worth $50, you have $40 per share in ordinary income taxed at your marginal rate.

Incentive stock options (ISOs)

Can receive more favorable tax treatment if you meet holding period requirements, but they trigger alternative minimum tax (AMT) concerns in the year of exercise.

Restricted stock units (RSUs)

Are taxed as ordinary income when they vest, based on the fair market value of the shares you receive.

These equity compensation events can push you into the highest tax brackets, especially if multiple years of options or RSUs vest simultaneously. The tax withholding your employer applies may be insufficient, requiring estimated tax payments to avoid penalties.

Legal Settlements: It Depends on the Claim

Settlement taxation depends entirely on what the settlement compensates:

- Personal physical injury or physical sickness settlements are generally tax-free, including compensation for medical expenses, pain and suffering, and emotional distress arising from the physical injury.

- Emotional distress or mental anguish without physical injury is taxable unless it's for medical expenses.

- Lost wages or lost profits are taxable as ordinary income.

- Punitive damages are almost always taxable, even if they're part of a physical injury case.

- Interest on any settlement is taxable.

Settlement agreements should clearly allocate amounts to different categories. This allocation affects both you and the payer, so expect negotiation about how settlement funds are characterized.

Lottery and Gambling Winnings: Fully Taxable

Lottery winnings, casino jackpots, and other gambling proceeds are taxable as ordinary income at your marginal rate. There's no special treatment or reduced rate—it's all taxed like wage income.

Federal withholding

Is typically 24% on gambling winnings over $5,000, but this may not cover your full tax obligation if the winnings push you into higher brackets.

State taxes

On gambling winnings vary. Some states exempt gambling income, others tax it fully, and a few have special rules for non-residents who win at casinos in their state.

Gambling losses

Can be deducted only up to the amount of gambling winnings, and only if you itemize deductions. You can't deduct net gambling losses to offset other income.

Real Estate Sales: Capital Gains with Possible Exclusions

When you sell real estate, capital gains taxes generally apply, but several important rules can reduce or eliminate the tax:

Primary residence exclusion

Allows you to exclude up to $250,000 of gain ($500,000 for married couples) if you've owned and lived in the home as your primary residence for at least 2 of the past 5 years.

Inherited property

Receives a stepped-up basis equal to fair market value on the date of death. This eliminates built-in capital gains. If you inherit property worth $300,000 that your parents bought for $50,000 decades ago and sell it shortly after for $300,000, you typically owe no capital gains tax.

Investment property

Doesn't qualify for the primary residence exclusion and may trigger depreciation recapture on previously claimed deductions.

Strategies to Manage Windfall Taxes

While you can't eliminate taxes on taxable windfalls, you can manage the impact:

- Understand before you act. Calculate your tax obligation before spending windfall funds. Set aside adequate money to cover all taxes due.

- Consider timing. If you have some control over when you realize the income—when you exercise options, when you close a business sale—timing it in a lower-income year reduces the tax bite.

- Use tax-deferred strategies. Rolling pre-tax windfall proceeds into retirement accounts (where allowed) defers taxes. Using appreciated assets for charitable giving avoids capital gains while providing deductions.

- Spread recognition over time if possible. Installment sales, structured settlements, or phased distributions can keep you in lower tax brackets across multiple years instead of concentrating income in one year.

- Maximize deductions in high-income years. Bunch charitable contributions, accelerate deductible business expenses, or time medical expenses to offset windfall income when possible.

- Consider state tax planning. If you have flexibility about residence, relocating to a more tax-friendly state before realizing a large windfall can save substantial amounts.

Work With Qualified Tax Professionals

Windfall taxation is complex, and mistakes are expensive. The cost of hiring a qualified CPA or tax attorney is typically far less than the cost of errors or missed opportunities.

Seek professional guidance before you receive the windfall if possible. Tax planning is most effective when done before transactions close or income is recognized. Once the windfall hits your bank account, many opportunities for tax minimization have already passed.

Your windfall is never what it appears to be gross—it's the after-tax amount that matters. Understanding what you'll owe and planning accordingly protects you from unwelcome surprises and preserves more of your windfall for its intended purposes.

This information is for educational purposes only and should not be considered personalized tax advice. Every windfall and inheritance situation involves unique tax considerations. Consult with qualified tax professionals before making decisions about significant windfall or inheritance income.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.