You've built $3 million through smart decisions, disciplined saving, and calculated risk taking. You understand compound interest, tax optimization, and diversification. Yet when markets drop 15%, you feel panic rising. When everyone's talking about the "next big thing," you feel FOMO pulling at you.

Intelligence doesn't make you immune to emotional money mistakes. In fact, successful people often struggle more with behavioral biases because confidence in other areas spills into financial decisions where it doesn't belong.

According to research from Charles Schwab, 65% of high net worth individuals admit that emotional biases impact their investment decisions.[1] The gap isn't knowledge. It's the space between knowing what to do and actually doing it when emotions run high.

What Is Behavioral Finance?

Behavioral finance is the study of how psychology, emotions, and cognitive biases influence financial decisions. Traditional finance assumes people make rational, logic driven choices. Behavioral finance acknowledges reality. Humans are emotional, pattern seeking, loss averse creatures who often make decisions that contradict their own best interests.

The core insight is this: Knowing the right financial strategy and executing it consistently are two different skills. The second skill, emotional discipline, often matters more than the first.

The Behavioral Biases That Cost High Net Worth Investors the Most

Loss Aversion Where Losses Hurt More Than Gains Feel Good

According to research from behavioral economists Daniel Kahneman and Amos Tversky, losses feel roughly 2 to 3 times more painful than equivalent gains feel good.[2] If you lose $50,000, the emotional pain far exceeds the pleasure you'd feel from gaining $50,000.

How this shows up: You hold losing investments too long, hoping they'll "come back" rather than selling and redeploying capital. You avoid necessary portfolio rebalancing because selling winners feels like giving up future gains. You become paralyzed during downturns, unable to make decisions because every option feels like accepting a loss.

The wealth cost: Holding losers too long while avoiding selling winners creates underperformance and emotional stress.

Recency Bias Where Recent Events Feel More Important Than They Are

Your brain will overweight recent information and underweights historical patterns. If the market was up 25% last year, you expect that to continue. If it's down 15% this year, you expect more decline.

How this shows up: You chase last year's best performing investments, buying high after performance has already happened. You panic during downturns, assuming the decline will continue forever and selling at the worst possible time. You make major allocation changes based on recent headlines rather than long-term strategy.

The wealth cost: Buying high and selling low, the exact opposite of what creates wealth.

Overconfidence Where Success in One Area Doesn't Transfer

You built a successful business, climbed to executive leadership, or excelled in your profession. That success creates confidence, which is valuable in your field. But confidence doesn't transfer to investment expertise.

How this shows up: You believe you can time the market or pick winning stocks despite evidence that professionals struggle to do this consistently. You underestimate risks because "it's worked before" or "I have a good feeling about this." You dismiss professional advice because you've made good decisions in other areas of life.

The wealth cost: Concentrated bets, poorly timed decisions, and expensive mistakes that could have been avoided with diversification and discipline.

Confirmation Bias Where You See What You Want to See

Once you've made a decision, your brain filters information to support that decision and dismisses contradictory evidence.

How this shows up: You hold a concentrated stock position and selectively notice positive news while ignoring warning signs. You've committed to an investment strategy and ignore data suggesting it's not working. You seek advice from sources that validate your existing beliefs rather than challenging them.

The wealth cost: Delayed course corrections and stubbornness that turns small mistakes into large losses.

Anchoring Where The First Number Sticks

The first price you see becomes a mental anchor. If your stock portfolio was worth $2 million at peak, and it declines to $1.7 million, you fixate on "getting back to $2 million" rather than evaluating what's best going forward.

How this shows up: You refuse to sell an investment that's declined because "it's down," ignoring whether it's still a good investment today. You make decisions based on your cost basis rather than current value and future prospects. You benchmark success against arbitrary past peaks rather than rational financial goals.

The wealth cost: Holding poor investments too long and making decisions based on irrelevant historical prices.

The High Net Worth Behavioral Finance Gap

Higher stakes amplify emotions. A 10% portfolio decline means $300,000 when you have $3 million. That's a year of spending, a child's college tuition, or a business investment. Larger numbers create larger emotional responses.

Success bias blinds you. You built wealth through smart decisions in your career or business. That success creates confidence that you can handle investments equally well, even though these are different skill sets.

Lack of accountability. You're used to being the decision maker. Taking advice feels like weakness. Yet investing is one area where objective, unemotional guidance matters most.

Complexity creates paralysis. High net worth portfolios are complex including multiple accounts, concentrated positions, tax considerations, and estate planning. Complexity makes it easier to delay decisions or default to whatever feels least uncomfortable.

Social comparison and FOMO. High net worth social circles create investment FOMO. When peers are talking about private equity deals or crypto gains, sitting in diversified index funds feels boring, even when it's the right strategy.

How Behavioral Coaching Helps

Behavioral coaching isn't therapy. It's financial guidance focused on execution and emotional discipline rather than just strategy.

What behavioral coaching provides includes these elements. Pre commitment strategies where you establish rules before emotions run high, accountability during volatility where your advisor talks you through market crashes and prevents panic driven decisions, reframing perspective by viewing same facts with different emotional response, systematic decision making based on pre established criteria rather than headlines or emotions, and permission to be human by acknowledging anxiety isn't weakness.

The Investment Behaviors That Build Wealth

1. Systematic Rebalancing

Rebalance annually or when allocations drift beyond thresholds. This forces you to "sell high" and "buy low," the opposite of emotional instincts.

2. Ignoring Short-Term Noise

Daily market moves, financial media panic, and quarterly performance swings are noise. Focus on annual performance, long term trends, and whether you're on track for financial goals.

3. Avoiding Timing Decisions

Market timing feels smart but rarely works. Time in the market beats timing the market. Stay invested according to your allocation regardless of predictions about what markets will do next.

4. Diversification as Emotional Insurance

Diversified portfolios reduce the emotional rollercoaster. When one asset class declines, others may hold steady or rise. This dampens volatility and makes staying disciplined easier.

5. Pre-Commitment to Rules

Establish investment rules before emotions are high like "I will rebalance annually on January 15," "I will not make allocation changes based on headlines," and "I will not check my portfolio daily."

When emotions flare, follow the rules.

How to Know If Behavioral Biases Are Costing You

Ask yourself honestly these questions. Have you sold investments during market downturns, then regretted it? Do you constantly check portfolio performance and feel anxious? Have you chased investments after strong performance, only to see them decline? Do you hold concentrated positions because "you know the company well"? Have you avoided making necessary changes because they "feel wrong"? Do you make major financial decisions based on what peers are doing?

If you answered yes to two or more, behavioral biases are likely costing you.

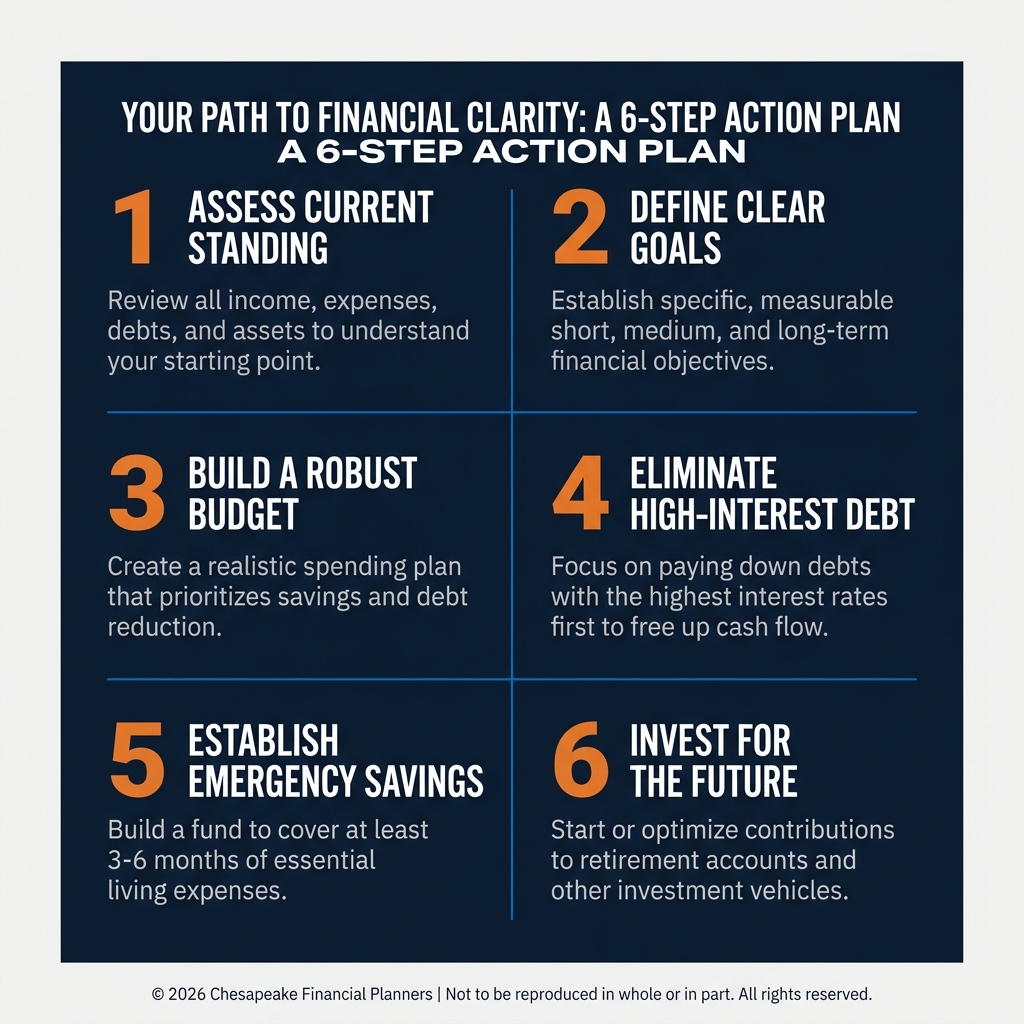

Your Behavioral Finance Action Plan

Acknowledge emotions are normal. Create a written investment policy statement. Establish accountability with a financial advisor whose role includes behavioral coaching. Limit portfolio checking (quarterly reviews are sufficient). Automate where possible (systematic contributions, rebalancing, tax-loss harvesting). Keep a decision journal to build self-awareness.

Intelligence Isn't Enough

You didn't build wealth by being impulsive or irrational. But investing tests emotional discipline in ways other areas of life don't.

The market doesn't care how smart you are or how successful you've been. It rewards discipline, consistency, and emotional management.

Acknowledging that you're human, subject to fear, greed, overconfidence, and anxiety, isn't weakness. It's the foundation of better financial decision making.

This information is not intended to be a substitute for specific individualized investment or financial advice. We suggest that you discuss your specific situation with a qualified financial advisor.

Please consult your financial professional regarding your specific situation.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

Diversification does not guarantee profit or protect against loss in declining markets.

Rebalancing may be a taxable event and does not ensure a profit or protect against a loss.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

References:

[1] "Understanding Behavioral Finance," Charles Schwab, 2024

[2] Kahneman, D., & Tversky, A., "Prospect Theory: An Analysis of Decision under Risk," Econometrica, 1979

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.