You're 58 years old with $2 million in traditional IRAs and 401(k)s. You plan to retire at 62. But when you start taking Required Minimum Distributions at 73, your tax bill will be massive, potentially pushing you into the 35% or 37% federal bracket.

What if you could systematically convert that pre-tax retirement money to Roth IRAs over multiple years, paying taxes at lower rates now to eliminate taxes entirely in retirement?

That's the Roth conversion ladder strategy. For high net worth pre-retirees and retirees, it's one of the most powerful tax planning tools available.

What Is a Roth Conversion Ladder?

A Roth conversion ladder is a multi-year strategy where you convert portions of traditional IRA or 401(k) balances to Roth IRAs annually, spreading the tax liability across multiple years rather than paying it all at once or waiting for high-tax RMDs.

The goal: Convert pre-tax retirement savings to Roth IRAs during low-income years when your tax bracket is lower, creating tax-free income for the rest of your life.

Why "ladder"? You're building a ladder of conversions each year adding another "rung" that will eventually provide tax-free income. —

Why Roth Conversion Ladders Matter for High Net Worth Retirees

Traditional IRAs and 401(k)s create future tax problems:

Required Minimum Distributions force taxable income. Starting at age 73, the IRS forces you to withdraw and pay taxes on a percentage of your pre-tax retirement accounts annually, whether you need the money or not.

RMDs push you into higher tax brackets. A $2 million IRA generates RMDs of $75,000+ at age 73, potentially pushing you from the 24% bracket into 32% or higher.

Taxes on Social Security benefits. RMDs can cause up to 85% of your Social Security benefits to become taxable.

Medicare premium surcharges. Higher income from RMDs can trigger Income-Related Monthly Adjustment Amounts (IRMAA), increasing Medicare Part B and D premiums by $1,000-$6,000+ per year.

Tax time bomb for heirs. When you die, heirs must withdraw inherited IRAs within 10 years, often at their highest tax rates.

Roth conversion ladders defuse all of these problems.

When to Execute Roth Conversion Ladders

The optimal window for Roth conversions is between retirement and when Social Security and RMDs begin, typically ages 60-72.

Why this window?

Lower income years: After retirement but before Social Security, your taxable income is often lower than during your working years or during RMDs.

Control over tax brackets: You choose how much to convert each year, filling up lower tax brackets without pushing into higher ones.

Time before RMDs: You have 13 years (ages 60-72) to systematically convert balances before RMDs force your hand.

Example timeline:

- Age 60-62: Retire, live off taxable savings or Roth contributions

- Age 62-72: Execute Roth conversion ladder, converting $80,000-$100,000 per year

- Age 70: Claim Social Security (optional timing based on planning)

- Age 73+: Minimal or no RMDs because most traditional IRA balance has been converted —

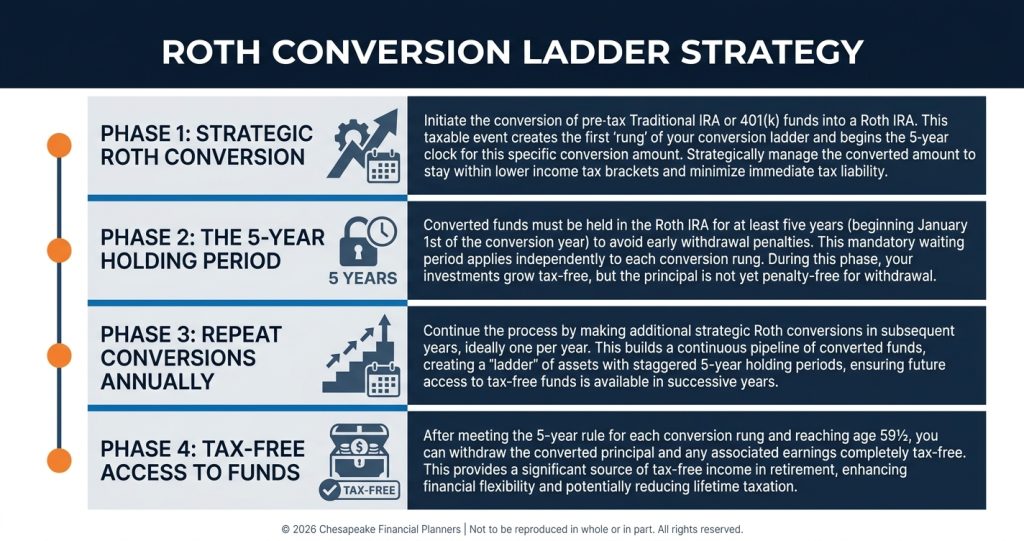

How to Build Your Roth Conversion Ladder

Step 1: Calculate your conversion capacity

Determine how much you can convert each year without pushing into undesirable tax brackets.

Example: You're married filing jointly in 2026. The 22% federal tax bracket for married filing jointly covers income from $100,800 to $211,400. You have $50,000 in other taxable income (interest, dividends, part-time work). You can convert $161,400 ($211,400 – $50,000) while staying in the 22% bracket.

Converting $161,400 keeps you in the 22% bracket rather than letting future RMDs push you into 32% or higher.

Step 2: Identify funding sources for taxes

Roth conversions create immediate tax bills. You must pay taxes without using the converted funds (which should stay invested for growth).

Funding sources:

- Taxable brokerage accounts

- Cash reserves

- Required Minimum Distributions from inherited IRAs

- Part-time work income

- Social Security (if already claiming)

Never use IRA withdrawals to pay conversion taxes that defeats the purpose.

Step 3: Execute annual conversions

Each year, convert the amount that fills your target tax bracket. Your CPA or financial advisor can calculate the precise amount based on your other income.

Timing: Execute conversions late in the year (November-December) when you have clarity on annual income. This prevents accidentally pushing into higher brackets due to unexpected income.

Step 4: Pay quarterly estimated taxes

Roth conversions increase your tax liability. Pay quarterly estimated taxes to avoid underpayment penalties.

Work with your CPA to calculate appropriate quarterly payments based on your conversion amounts.

Step 5: Let converted funds grow tax-free

Once converted to Roth IRAs, funds grow tax-free forever. Reinvest distributions and let compound growth work its magic.

Step 6: Repeat annually until optimal balance achieved

Continue conversions year after year until you've converted enough to minimize future RMDs or eliminate them entirely.

Advanced Roth Conversion Ladder Strategies

Fill multiple tax brackets strategically

Don't obsess over staying in the lowest bracket. Sometimes converting into the 24% or even 32% bracket makes sense if it prevents 35% or 37% taxes on future RMDs.

Run projections comparing current conversion taxes versus future RMD taxes. Often, paying 24-32% now beats 35-37% later.

Coordinate conversions with Social Security timing

Delaying Social Security from 62 to 70 creates an eight-year window with lower income, ideal for aggressive Roth conversions.

Convert aggressively before claiming Social Security, then reduce or stop conversions once benefits begin.

Use market downturns opportunistically

When your IRA declines 20% during a bear market, the same dollar amount converts more shares. Those shares recover and grow tax-free in the Roth IRA.

Example: Your IRA was worth $1 million, declines to $800,000. Converting $100,000 now transfers more shares than converting $100,000 when the account was worth $1 million.

Convert just enough to manage IRMAA surcharges

Medicare IRMAA surcharges kick in at specific income thresholds. Convert enough to stay below the next IRMAA tier while maximizing conversions.

2026 IRMAA thresholds (married filing jointly):

- Under $218,000: No surcharge

- $218,000-$274,000: +$81.20/month per person

- $274,000-$342,000: +$202.90/month per person

Stay below thresholds when possible, or convert aggressively if you're already over.

Layer conversions with charitable giving

Charitable contributions reduce taxable income, creating room for larger Roth conversions within your target bracket.

Example: Convert $150,000 and donate $30,000 to a donor-advised fund. The $30,000 deduction offsets part of the conversion income, effectively reducing the conversion's tax cost. —

Common Roth Conversion Ladder Mistakes

Mistake 1: Converting too much in one year

Pushing into the 35% or 37% bracket rarely makes sense. Spread conversions across multiple years.

Mistake 2: Not accounting for state taxes

Federal brackets aren't the only consideration. High-tax states like California add 9-13% to your conversion cost.

Mistake 3: Forgetting about the five-year rule

Roth conversions must season for five years before earnings can be withdrawn tax-free. Plan accordingly if you need access to funds before age 59½.

Mistake 4: Ignoring future tax law changes

Tax rates could increase or decrease. Don't delay conversions indefinitely hoping for lower rates; that's speculation.

Mistake 5: Not coordinating with your CPA

Roth conversions affect your entire tax situation. Your CPA must be involved in planning and execution. —

Should You Build a Roth Conversion Ladder?

Roth conversion ladders make sense if:

- You have significant pre-tax retirement savings ($500,000+) that will create large RMDs.

- You're between retirement and RMDs (roughly ages 60-72) with low current income.

- You have cash or taxable assets to pay conversion taxes without touching the converted funds.

- You expect higher tax rates in retirement due to RMDs, pensions, Social Security, or rental income.

- You want to eliminate RMDs to control your tax situation in retirement.

- You want to reduce taxes for heirs by passing Roth IRAs instead of traditional IRAs.

Roth conversion ladders may not make sense if:

- You expect to be in a lower tax bracket in retirement than during conversion years (rare for high earners but possible).

- You lack cash to pay conversion taxes without using retirement account withdrawals.

- You need maximum current cash flow and can't afford to pay taxes on conversions. —

Your Roth Conversion Ladder Action Plan

- Run a retirement tax projection. Work with your financial advisor and CPA to project future RMDs and tax brackets.

- Calculate optimal annual conversion amounts. Identify the "sweet spot" that fills lower tax brackets without pushing into higher ones.

- Identify tax payment sources. Earmark taxable account funds or other cash to pay conversion taxes.

- Execute your first conversion. Start with a conservative amount to understand the process and tax impact.

- Pay quarterly estimated taxes. Avoid penalties by paying taxes as you convert.

- Monitor and adjust annually. Tax laws change, your income changes, and your strategy should adapt accordingly.

- Document your strategy. Ensure your spouse or financial power of attorney understands the plan if you become incapacitated. —

Roth Conversion Ladders Are Long-Term Tax Arbitrage

Roth conversion ladders aren't about eliminating taxes they're about paying taxes at lower rates now rather than higher rates later.

For high net worth individuals with substantial pre-tax retirement savings, the math is compelling. Pay 24-32% taxes today through strategic conversions rather than 35-37%+ taxes on future RMDs.

The result? Tax-free retirement income, no RMDs controlling your tax situation, lower Medicare premiums, and a better inheritance for your heirs.

Work with experienced financial and tax professionals to build your ladder. The savings compound over decades.

This information is not intended to be a substitute for specific individualized tax or investment advice. We suggest that you discuss your specific situation with a qualified tax or investment advisor.

Please consult your tax professional regarding your specific tax situation.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

Roth IRA distributions of earnings are tax-free as long as the distribution is made more than five years after your first Roth IRA contribution and you are at least 59½, or as a result of your disability or death.

A Roth IRA conversion may not be suitable for your situation. The conversion will result in taxation of the converted amount. You should consult with a tax advisor before implementing any Roth IRA conversion strategy.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.