You've built a valuable business; but do you actually know what it's worth? Most business owners operate on gut instinct or outdated assumptions about their company's value. Then, when it's time to sell, transition to family, or plan for retirement, they discover their expectations were dramatically off target.

The gap between what you think your business is worth and what a buyer will actually pay can be painful. It can derail retirement plans, create family conflict, or force you to work years longer than intended.

Why Business Owners Overestimate (or Underestimate) Value

Business valuation isn't about what you've invested, how hard you've worked, or what you need to retire comfortably. It's about what a rational buyer would pay for future cash flows.

Common valuation mistakes include:

- Counting owner salary as profit when it should be an expense

- Ignoring customer concentration risk (one client represents 40% of revenue)

- Assuming your industry expertise transfers to a buyer

- Including personal assets or expenses in the business valuation

- Using outdated valuation multiples from different market conditions

Here's the philosophical truth: Your business ought to be valued fairly for what it actually produces, not what it once produced or what it could theoretically produce. Fair valuation requires removing emotion and focusing on transferable value.

We understand how frustrating it feels to hear your life's work reduced to spreadsheets and multiples. But accurate valuation is the foundation of strategic exit planning.

The Three Primary Valuation Methods

Professional valuators typically use three approaches, then weight them based on your business type and situation.

Asset-Based Valuation

This approach tallies up what your business owns and owes: equipment, inventory, real estate, intellectual property, accounts receivable, minus liabilities.

When it's used: Asset-based valuation works best for businesses being liquidated, holding companies, or businesses with minimal operating income but significant assets (like real estate holdings).

The limitation: Most operating businesses are worth more than their asset value because of goodwill, customer relationships, and ongoing operations. Asset-based valuation typically represents the floor value.

Market-Based Valuation (Comparable Sales)

This approach looks at what similar businesses have sold for recently, then adjusts for differences in size, profitability, growth, and risk.

When it's used: Market-based valuation works well when there are truly comparable transactions in your industry. It's common for professional services firms, retail businesses, and franchises with active acquisition markets.

The limitation: Finding truly comparable sales is harder than it seems. Industry, geography, size, growth rate, and dozens of other factors impact comparability.

Income-Based Valuation (Discounted Cash Flow)

This approach calculates the present value of future cash flows your business is expected to generate. It's the most theoretically sound method and most commonly used for established operating businesses.

When it's used: Income-based valuation is preferred for businesses with predictable cash flows, especially when buyers are acquiring the business for its ongoing operations rather than its assets.

The limitation: It requires assumptions about future growth, margins, and risk all of which can be debated.

The Multiple Everyone Asks About

When business owners ask "what's my business worth," they're usually thinking about EBITDA multiples a shorthand version of income-based valuation.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) represents your core operating profit. Buyers apply a multiple to your EBITDA based on industry, size, growth, and risk factors.

Typical EBITDA multiples range from:

- 2-3x for small businesses (under $1M EBITDA)

- 4-6x for mid-sized businesses ($1M-$5M EBITDA)

- 6-10x for larger businesses (over $5M EBITDA) or high-growth tech companies

- 10x+ for businesses with recurring revenue, minimal owner dependence, and strong growth

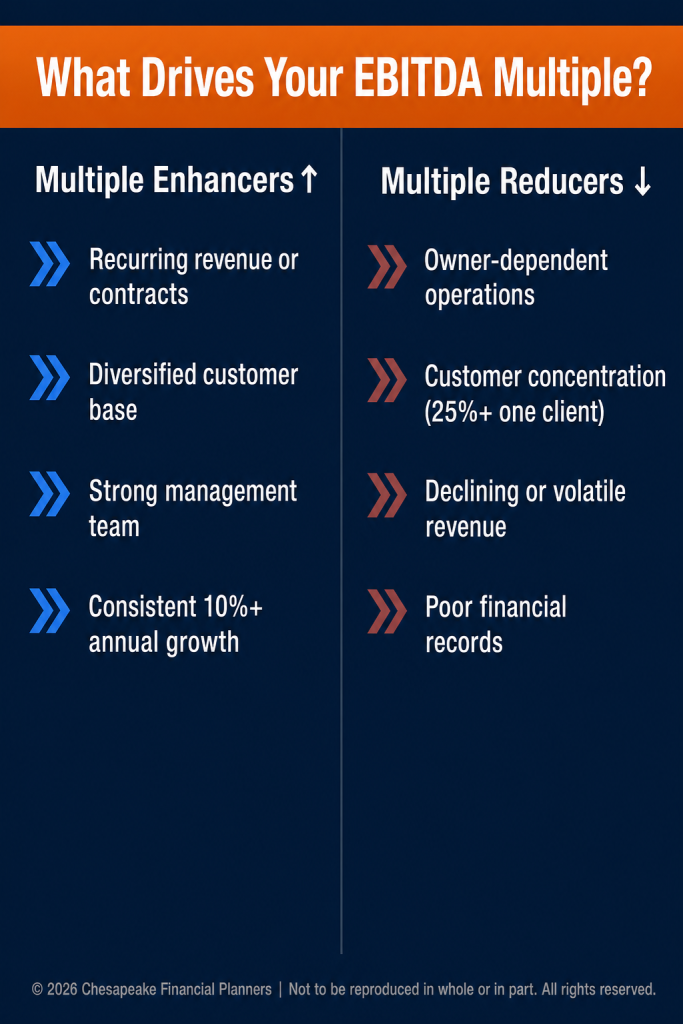

But here's what drives multiples up or down:

Multiple Enhancers:

- Recurring revenue or contracts

- Diversified customer base (no single customer over 10% of revenue)

- Strong management team that stays post-sale

- Proprietary products, processes, or intellectual property

- Consistent revenue and profit growth (10%+ annually)

- Clean financials and strong systems

Multiple Reducers:

- Owner-dependent operations

- Customer concentration (one customer = 25%+ of revenue)

- Declining or volatile revenue

- Low margins or intense competition

- Regulatory or legal risks

- Poor financial records or mixing personal/business expenses

Normalizing Your EBITDA: What Actually Counts

Before applying any multiple, valuators "normalize" your earnings by adding back certain expenses and removing one-time items.

Common add-backs:

- Owner compensation above market rate

- Personal expenses run through the business

- One-time legal fees or non-recurring expenses

- Family members on payroll above market compensation

- Excess rent if you own the building

Common reductions:

- Owner compensation below market rate (replacement cost of hiring someone to do your job)

- Deferred maintenance or needed capital expenditures

- Unpaid family member contributions

The normalized EBITDA is what buyers care about the sustainable cash flow the business generates under normal operating conditions.

Beyond the Numbers: Qualitative Value Drivers

Two businesses with identical EBITDA can have dramatically different values based on qualitative factors:

Strategic value: Does the business fill a gap for strategic buyers? (Geographic expansion, new product line, vertical integration)

Growth potential: Are there obvious growth opportunities an acquirer could unlock?

Competitive position: How defensible is your market position?

Brand strength: Do customers specifically seek out your brand?

These factors can add 20-50% to your valuation, or reduce it if they're weaknesses.

Getting a Professional Valuation

If you're within 5-10 years of a potential exit, get a professional valuation. Costs typically range from $5,000 to $25,000+ depending on business complexity.

Three levels of valuation:

- Calculation of value: Least expensive, provides estimate based on limited information

- Summary valuation: Mid-tier, provides defendable number with moderate documentation

- Comprehensive valuation report: Most expensive, full documentation, meets IRS and court standards

For exit planning, a summary valuation usually provides sufficient detail to guide strategy without excessive cost.

Your Three Next Steps

1. Calculate your own preliminary estimate. Take your normalized EBITDA and apply a conservative multiple for your industry (your acco untant can help).

2. Identify value gaps. What's the difference between your estimate and what you need to achieve your retirement goals?

3. Build a value enhancement plan. Work with advisors to identify specific actions that increase your multiple or EBITDA over the next 3-5 years.

Knowing your business value isn't about satisfying curiosity. It's about building a strategic roadmap to maximize what you've built.

If you're ready to get clarity on your business value and build a plan to enhance it before exit, schedule a complimentary consultation. We'll help you understand what drives value in your industry and create a specific action plan.

This material is for educational purposes only and should not be construed as investment, legal, or tax advice. Business valuations can vary significantly based on methodology, market conditions, and business-specific factors. Actual sale prices may differ from valuation estimates. Please consult with qualified advisors regarding your specific situation.

Advisors associated with Chesapeake Financial Planners may be either (1) LPL Financial Registered Representatives offering securities through LPL Financial, Member FINRA and SIPC, and investment advisor representatives offering investment advice through Great Valley Advisor Group; or (2) solely investment advisor representatives offering investment advice through Great Valley Advisor Group and not affiliated with LPL Financial. Great Valley Advisor Group, and Chesapeake Financial Planners are separate entities from LPL Financial.

Chesapeake Financial Planners | 2402 Scotlon Ct, Forest Hill, MD 21050 | (410) 652-7868 | www.chesapeakefp.com

© 2026 Chesapeake Financial Planners | Not to be reproduced in whole or in part. All rights reserved.